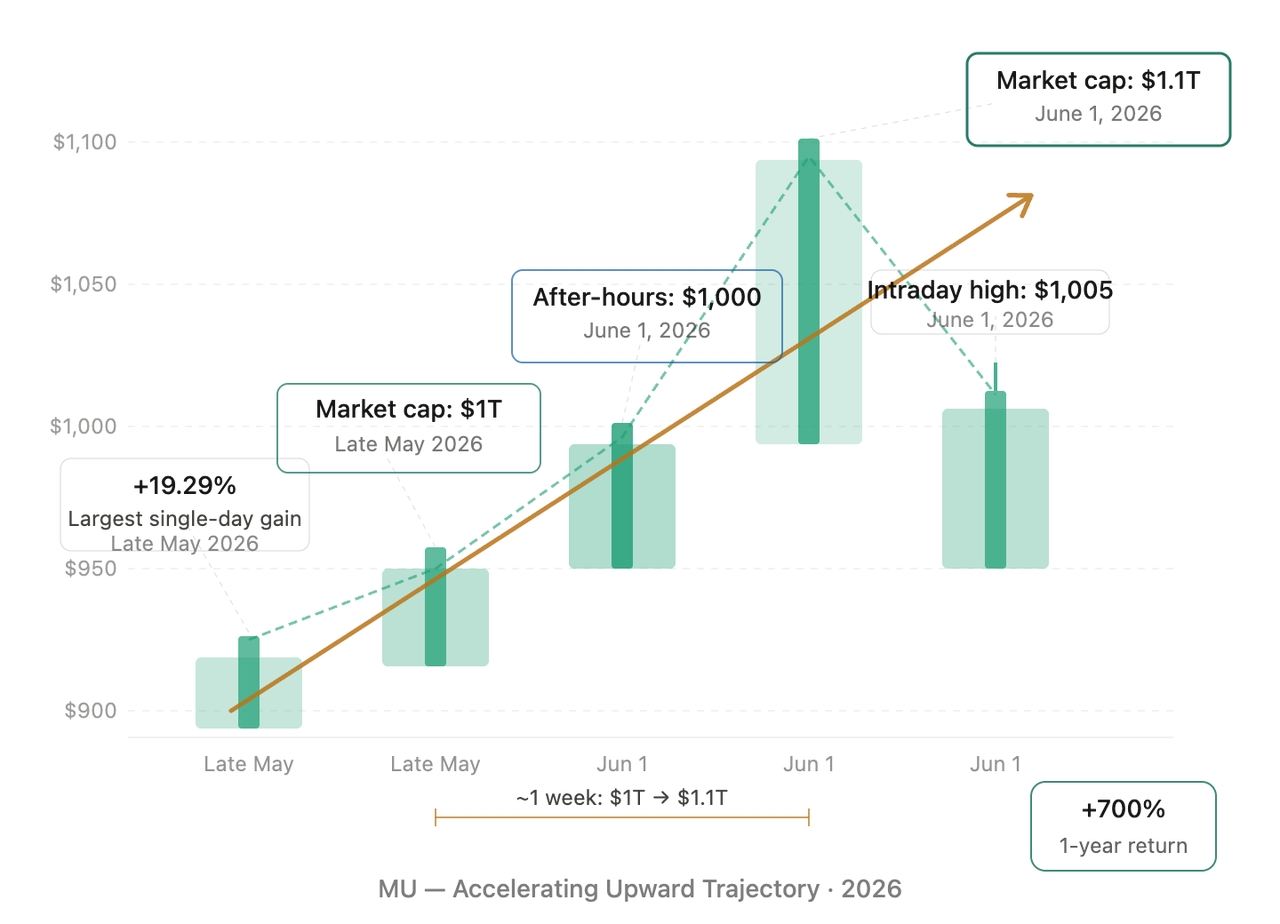

Micron Technology (MU) officially broke through the $1,000 mark during after-hours trading on June 1, 2026, temporarily trading at $1,005 and pushing its total market capitalization past $1.1 trillion. This milestone carries both technical and psychological significance—it marks Micron’s entry into the $1,000 stock price club. The last company to achieve a similar leap was NVIDIA during the previous AI cycle’s acceleration phase.

From a news perspective, this after-hours breakout wasn’t triggered by a single earnings report or event, but rather by the steady accumulation of multiple positive signals. Micron previously confirmed that its entire high-bandwidth memory (HBM) production capacity for 2026 has already sold out, creating an extremely tight supply-demand environment that significantly strengthens its pricing power. At the same time, several Wall Street investment banks have raised their earnings forecasts for memory chip giants including Micron, citing continued demand for AI training, inference, and agent systems that far outpaces current industry supply.

Notably, the pace of this breakout differs sharply from previous weeks. In late May, Micron’s market cap first crossed $1 trillion, with the stock surging 19.29% in a single day—the largest daily gain since 2011. MU climbed from $1 trillion to $1.1 trillion in just about a week. This kind of acceleration usually occurs when market sentiment is highly aligned, signaling growing tension between momentum and fundamentals in the near term.

MU’s Accelerated Upward Trajectory—Timeline from $1 Trillion Market Cap to $1,000 Stock Price

Stock Price Breaks $1,000—Will MU’s Stock Split Move from Rumor to Reality?

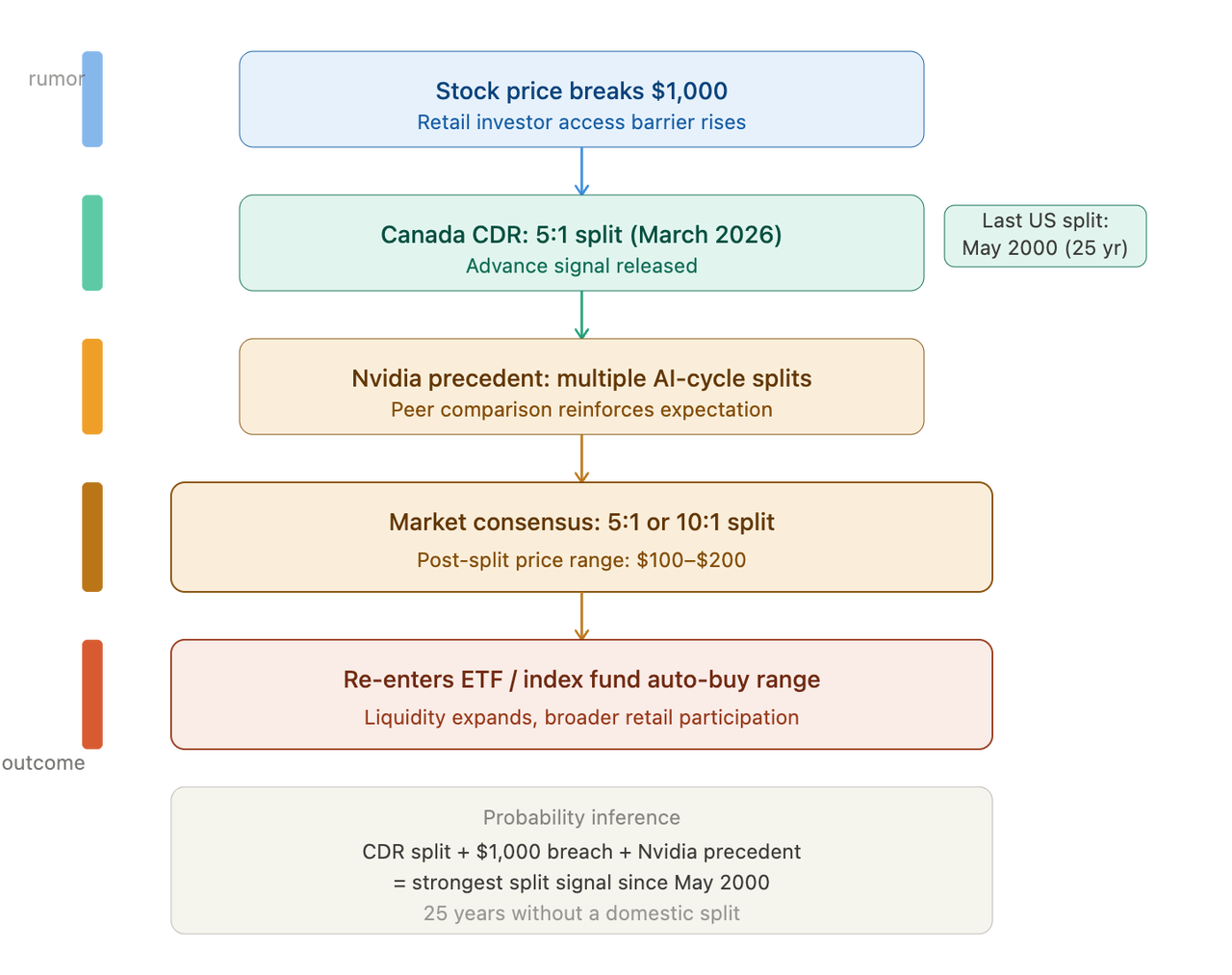

When a company’s stock price reaches the $1,000 level, the question of a stock split shifts from "if" to "when." Micron last executed a stock split in May 2000 (2-for-1), and before that in 1995 (also 2-for-1), meaning it’s been over 25 years since the last split.

A signal not to be overlooked: Micron’s Canadian Depositary Receipts (CDR) underwent a 5-for-1 split in March 2026, further fueling speculation that MU, listed on Nasdaq, will eventually follow suit. From a corporate governance perspective, splitting depositary receipts in other markets is often seen as a preliminary test ahead of a formal split.

Peer comparisons reinforce this logic. NVIDIA executed multiple stock splits during its previous AI-driven rally to maintain retail investor participation and trading liquidity. Micron’s current situation is strikingly similar—its stock has gained over 700% in the past year, and retail investor holdings still have room to grow. If management decides to move forward with a split, the market generally expects a 5-for-1 or 10-for-1 ratio, which would bring the share price back to the $100–$200 range and restore automatic allocation by more ETFs and index funds.

A Historic Signal Not Seen in 25 Years—Micron Stock Split Probability Logic Chain

After $1.1 Trillion Market Cap, Why Is the Market Debating an AI Chip Bubble?

Micron’s break through $1,000 and its $1.1 trillion market cap coincide with intense debate over whether an AI chip bubble is forming. Bulls argue that the highly cyclical semiconductor industry is undergoing structural change, with AI-driven demand permanently elevating profitability. Bears counter that the market is overheated, investors are chasing the latest hype, and the semiconductor sector has several months of lag from orders to product delivery—if demand slows, inventory buildup and pricing weakness could sharply reduce profits.

Valuation concerns are not unfounded. The market expects Micron’s net profit in 2026 to jump from $8.5 billion in 2025 to $66.8 billion, and reach about $120 billion in 2027. Meanwhile, the memory chip sector’s price-to-earnings ratio has approached 71x, near historic highs since the financial crisis. High valuations don’t necessarily mean a bubble, but they do indicate that current prices reflect extremely optimistic growth expectations. Any slowdown in shipments or pricing in future quarters could trigger a dramatic market repricing.

Another risk signal comes from momentum trading strategies. According to momentum stock data tracked by 22V Research, turnover has risen from 2% at the start of the year to nearly 5%. Experts warn that the risk of a "momentum crash" is accumulating. Some of Micron’s recent gains may also be linked to a "gamma squeeze" caused by investors piling into call options—where options dealers hedge their books, unintentionally driving nonlinear price increases.

What Does the $1,000 Breakthrough Mean for the Crypto Market?

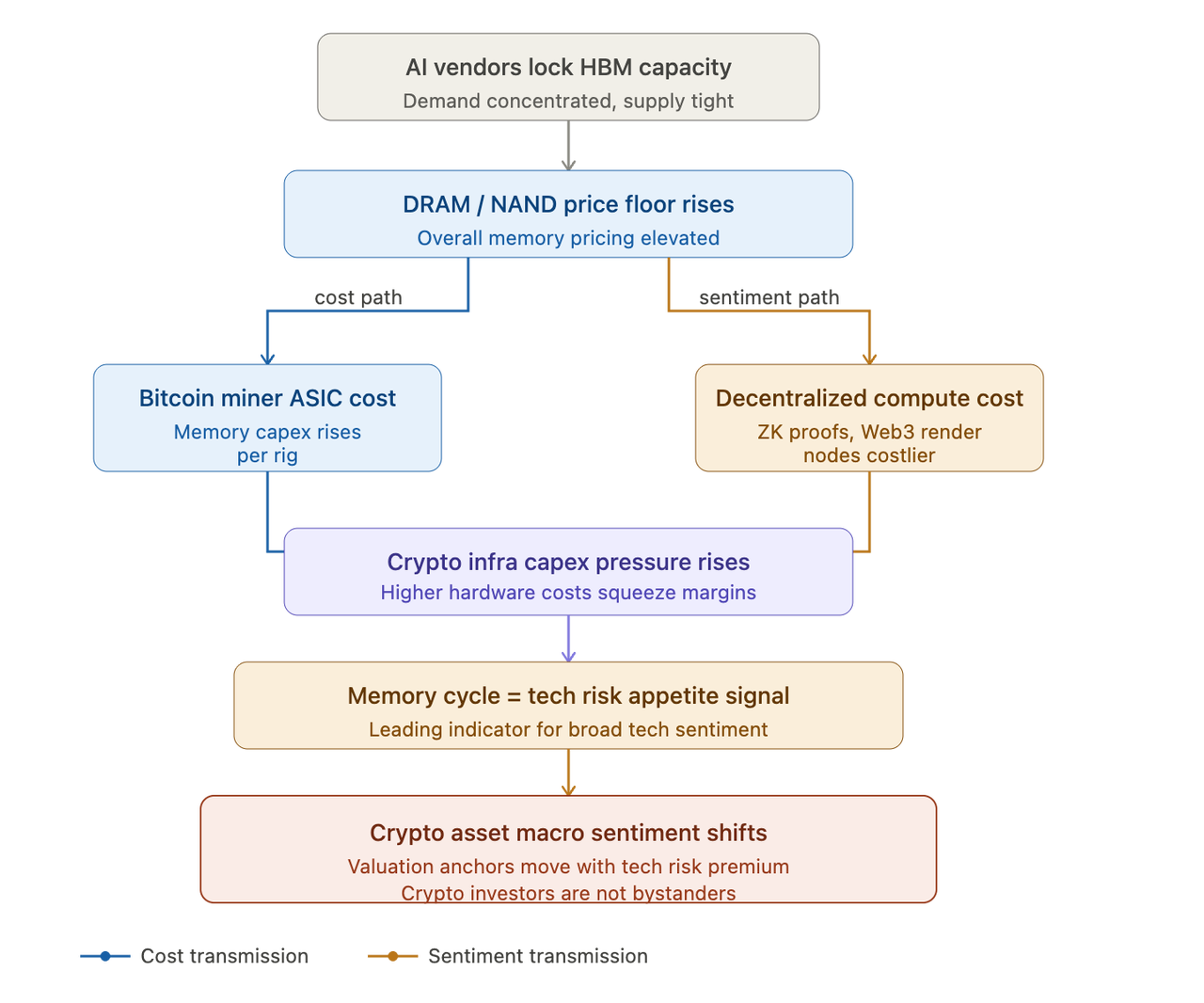

Crypto investors aren’t just spectators to Micron’s stock rally—they’re indirect beneficiaries. Bitcoin mining relies on ASIC chips, Ethereum Layer 2 nodes require high-performance computing hardware, and the intersection of AI and crypto—decentralized compute markets, ZK proof acceleration, Web3 game cloud rendering—all depend on advanced process chips.

When Micron’s HBM capacity is locked up by AI chip manufacturers, overall DRAM and NAND supply tightens, pushing up the price baseline for memory chips. For crypto infrastructure operators who need large amounts of memory devices, this means rising capital expenditure pressures.

How Memory Chips Impact the Crypto World—Price Linkage Mechanism

Additionally, the supply-demand cycle of memory chips is often seen as a leading indicator of global tech risk appetite. When investors are willing to pay higher valuations for semiconductor companies, it reflects confidence in the long-term growth of the digital economy. As a key part of the digital economy, crypto asset valuations are indirectly influenced by these macro sentiment shifts. The combined market cap of the three major memory chip companies now exceeds $1 trillion each, together surpassing the total market cap of Meta and Tesla. This concentration of capital sends a clear signal across the tech investment landscape.

How HBM Capacity Lock-In and DRAM Price Surge Are Reshaping the Industry

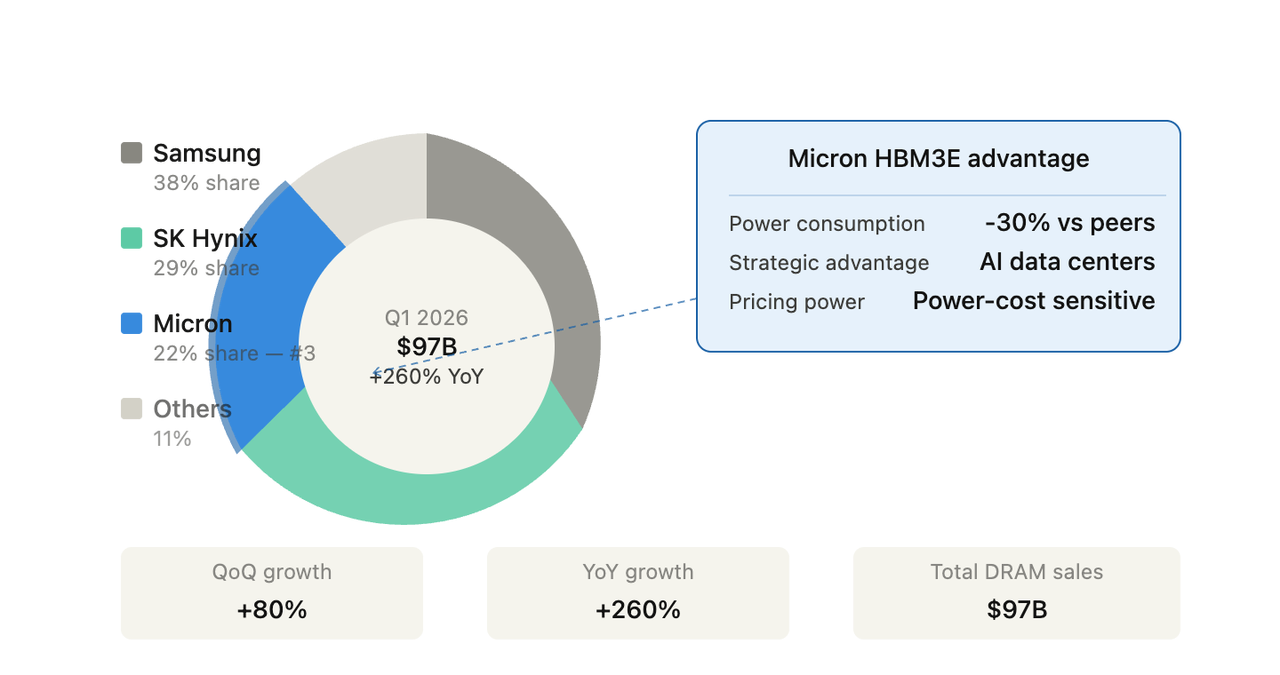

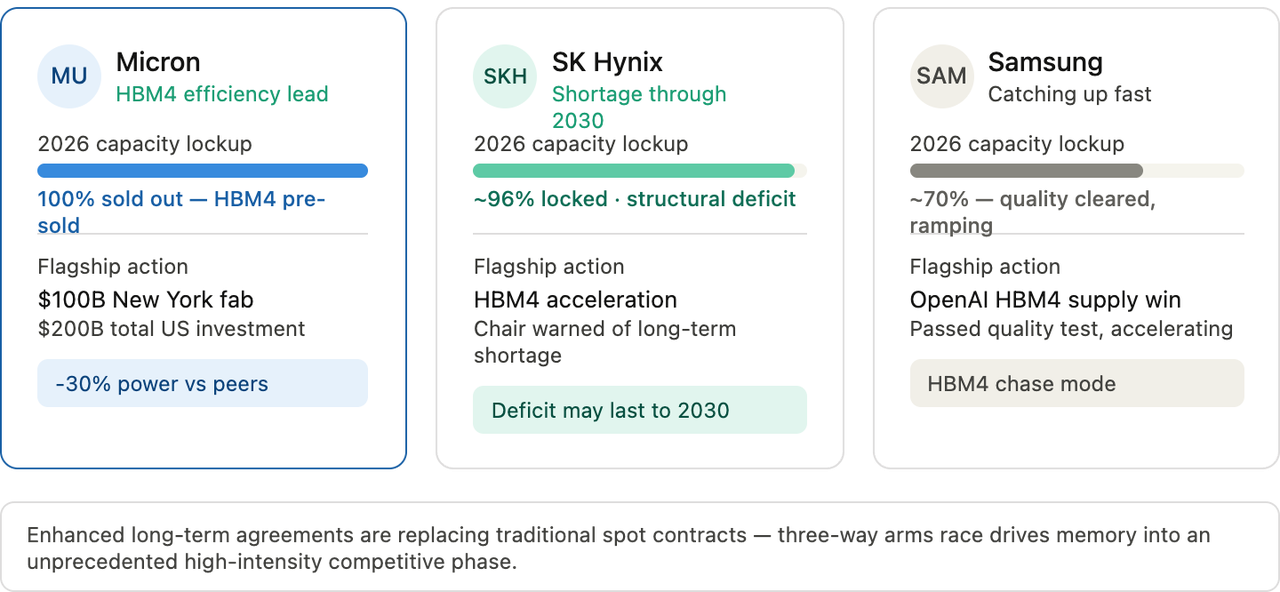

The main driver of this memory chip cycle is the structural supply-demand imbalance in HBM. Global DRAM sales in Q1 2026 surged 80% quarter-over-quarter to $97 billion, up 260% year-over-year. In terms of market share, Samsung leads with 38%, SK Hynix follows at 29%, and Micron ranks third with 22%. While Micron trails the Korean giants in share, its HBM3E products offer differentiated energy efficiency—the latest chips consume 30% less power than competitors. This efficiency is crucial for AI data center operators, as power costs are increasingly central to their operating expenses.

HBM Structural Supply-Demand Imbalance—Q1 2026 Global DRAM Market Landscape

Micron is also accelerating its expansion. The company has announced a $100 billion investment to build the largest semiconductor plant in the US in New York State, with a total $200 billion plan to expand domestic memory manufacturing and R&D. The project is underway and expected to begin production in 2030. UBS analysts raised Micron’s target price from $535 to $1,625, citing a fundamental shift in the memory industry—new "enhanced" long-term agreements are replacing traditional purchase contracts, featuring longer terms, fixed shipment commitments, and key fixed pricing frameworks.

Meanwhile, competition for HBM4 has already begun. SK Hynix’s chairman stated the world is in a "structural shortage" that may last until 2030. Micron’s CEO confirmed the company has "pre-sold every HBM4 chip it can produce this year." Samsung is catching up, having passed quality tests and secured large orders from OpenAI for HBM4. The arms race among the three giants is pushing the memory chip industry into an unprecedented phase of intense competition.

The Memory Chip Giants’ Arms Race—HBM Expansion and Future Plans Compared

How Will the Tension Between Earnings Growth and Valuation Expansion Play Out?

From an earnings forecast perspective, Micron is currently in one of its best historical positions. Multiple analysts have issued aggressive targets—Susquehanna raised its price target to $1,750, citing stronger-than-expected DRAM pricing, stable NAND prices, and tight HBM supply. In the past three months, no analyst has issued a sell rating on the stock, with 27 buy ratings and only 3 holds.

Earnings Leap and Valuation Ceiling—MU Earnings Forecast and Target Price Divergence

However, the average Wall Street target price is just $804.26, implying about 17% downside from the current $1,005 level. This phenomenon—high consensus ratings but an average target price below the current market price—is rare historically. It highlights a core issue: institutional investors remain optimistic about Micron’s fundamentals but generally believe the recent price surge has exceeded reasonable limits.

On a broader scale, earnings expectations for memory chip companies are ballooning at an astonishing rate. Micron’s earnings in 2026 are projected to leap from $8.5 billion in 2025 to $66.8 billion—nearly an eightfold increase. Yet the jump from $1 trillion to $1.1 trillion in market cap took only about a week, signaling a certain degree of concentrated market sentiment.

Conclusion

Micron’s after-hours breakthrough of $1,000 and its $1.1 trillion market cap are the result of AI-driven structural HBM demand, sold-out production capacity, and heightened expectations for a stock split. The logic behind the split rumors is clear: 25 years without a split, the signal from the Canadian Depositary Receipt split, and historical precedent from peers all shift the question from "if" to "when."

For crypto industry investors, memory chip price trends and supply-demand dynamics indirectly affect mining infrastructure costs and the pace of decentralized compute network expansion. When HBM capacity is locked up by AI chip manufacturers, tightening DRAM supply pushes up prices across all memory products, and crypto infrastructure operators must contend with these rising costs.

It’s worth noting that Micron’s current valuation already reflects extremely optimistic growth expectations. The average analyst target price below the current market price highlights growing tension between short-term gains and fundamentals. The evolution of HBM4 competition, production ramp-up, and changes in macro interest rates are all key variables to monitor going forward.

FAQ

When exactly did Micron Technology break through $1,000?

According to market data from June 1, 2026, Micron Technology (MU) broke through the $1,000 mark during after-hours trading, temporarily trading at $1,005 and pushing its market cap past $1.1 trillion. This breakout happened about a week after the market cap first crossed $1 trillion in late May, marking an accelerated upward move.

What’s the latest on MU stock split rumors?

As of June 2026, Micron has not issued a formal stock split announcement. However, market attention has surged, driven by several factors: the stock price has surpassed $1,000, meeting the typical threshold for a split; Micron’s Canadian Depositary Receipts underwent a 5-for-1 split in March 2026, fueling speculation about MU following suit; and multiple investment banks have listed Micron as a likely candidate for a split announcement within the next 3–6 months. A split would not change shareholder equity or company market cap, but would increase liquidity and lower trading barriers.

Does the $1,000 breakthrough have direct or indirect impacts on the crypto market?

There’s no direct causal relationship, but a clear indirect transmission mechanism exists: memory chip prices affect the cost of crypto mining and decentralized compute network infrastructure; semiconductor industry strength reflects global tech risk appetite, and crypto assets benefit from the same macro sentiment; the intersection of AI and crypto—such as ZK proof acceleration and Web3 game rendering—directly depends on advanced process chip supply and pricing.

How much longer can the memory chip cycle’s upswing last?

The duration of this cycle depends on the slope of AI demand growth versus the pace of supply expansion. SK Hynix’s chairman believes the "structural shortage" may persist until 2030, and Micron’s CEO has confirmed all HBM4 chips for this year are pre-sold. Some analysts warn that, after data center buildouts are completed, large tech firms may slow investment faster than expected, reducing overall hardware demand. The evolution of HBM4 competition will be a key variable in identifying the cycle’s turning point.

Should investors be concerned about Micron’s high valuation risk?

Looking at the data, Wall Street’s average target price of $804.26 is below the current $1,005 price, implying about 17% downside. The memory chip sector’s price-to-earnings ratio is near 71x, the highest since the financial crisis. Some analysts note that recent gains may be driven by "gamma squeezes" in the options market rather than pure fundamentals, and such derivative-driven rallies often come with higher short-term volatility risk.