CASHCAT tokenomics analysis should be considered in the context of the overall project landscape. Begin by understanding the narrative positioning and on-chain participation framework of Cash Cat (CASHCAT), then revisit the parameters themselves. This approach makes it easier to distinguish between “narrative language” and “verifiable facts.” Common public disclosures include a 1B total supply, 0/0 tax rate, and LP burned; these indicators help outline the project at a glance, but cannot alone provide a comprehensive risk assessment.

What Does a 1B Total Supply Mean in Meme Projects?

A fixed total supply is typically used to set expectations for a “clear supply cap.” For meme projects, the total supply itself is not a measure of quality; what matters more are the allocation structure, circulation pace, and concentration of holdings. Without this supporting information, the total supply figure alone cannot provide a full assessment.

A 1B (one billion) supply is a standard denomination in the meme coin space, allowing the community to easily discuss circulation and holding ratios in whole numbers. Researchers should distinguish between the “maximum supply cap” and the “actual tradable circulating supply”: the former is the cap stated in the contract or disclosures, while the latter depends on factors like locked tokens, team reserves, uncirculated addresses, and the actual depth in the liquidity pool.

| Indicator |

Surface Meaning |

Further Considerations |

| 1B Total Supply |

Clear supply cap |

Distribution and circulation pathways |

| Issuance Structure |

Perceived fairness in narrative |

Presence of abnormally concentrated addresses |

| Circulation Pace |

Basis for trading activity |

Consistency with public narrative |

The core of parameter analysis is not “whether the numbers look good,” but “whether the numbers can be continuously validated by on-chain data.” If the disclosed total supply is inconsistent with the on-chain total supply, decimals, or contract read-only functions, always defer to the verifiable on-chain data and recheck information sources.

Why Is a 0/0 Tax Rate Frequently Highlighted?

A 0/0 tax rate typically means neither buying nor selling incurs additional tax, which intuitively reduces trading friction. For participants, this improves quote predictability, but does not reduce volatility risk. Meme asset prices remain driven by sentiment and liquidity.

Tax rate information is often misinterpreted as a “low-risk label.” In reality, it only describes the transaction fee structure and does not address market depth, price stability, or information quality. Equating tax rate with risk is a classic analytical mistake. Even if the contract shows a zero buy/sell tax, DEXs may still have slippage, routing losses, and network gas fees—these are market and infrastructure costs, not “project taxes.”

In cross-project comparisons, many meme coins also use low or zero tax as a marketing narrative. The real differences are rarely in the tax rate itself, but in the narrative anchor, chain context, and community rhythm. See CASHCAT vs Typical Meme Coin for a breakdown of these dimensions.

How Is LP Burned Commonly Explained and Verified?

LP burned is often described as “liquidity pool control being locked or relinquished,” intended to reduce certain liquidity operation risks. This claim must be validated on-chain, not just accepted from project statements. Verification includes: checking where LP tokens are sent, reviewing contract permissions, and observing pool status changes.

“Burned” can mean different technical implementations across projects: sending LP tokens to an irrecoverable address, using a time-lock contract, or restricting withdrawals via multisig/custody. The same label does not always mean the same security outcome. Always treat “LP burned” as a hypothesis to be verified, not a final safety conclusion.

| Verification Dimension |

Focus Point |

Possible Conclusion |

| LP Token Destination |

Sent to uncontrollable/locked address? |

Reduces risks of direct pool withdrawal |

| Contract Permissions |

Can tax, mint, or blocklist parameters still be changed? |

Determines if permission boundaries remain open |

| Pool Status Change |

Any sudden, abnormal changes? |

Flags operational or market risk signals |

It’s also critical to distinguish between “liquidity is locked” and “liquidity is sufficient.” Restricting LP control does not guarantee the pool is deep enough to absorb large trades; if depth is lacking, slippage and price impact may still be significant. Always cross-check parameter claims with on-chain realities.

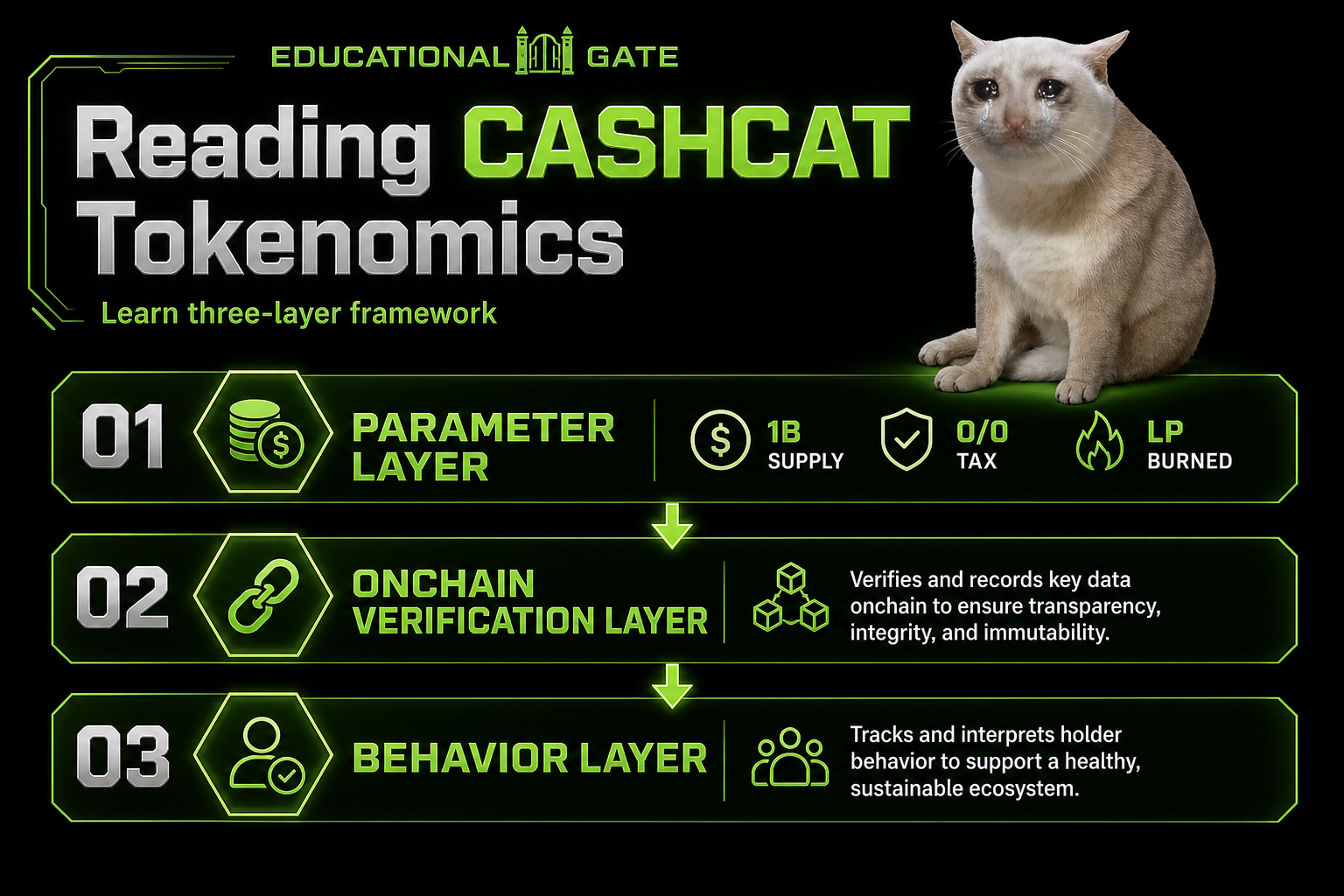

How Do These Three Parameters Fit Into a Unified Analytical Framework?

A “three-layer framework” is recommended: parameter layer, on-chain layer, and behavioral layer. The parameter layer reviews public disclosures; the on-chain layer checks data consistency; the behavioral layer examines whether community and market actions align. The more consistent these layers, the more robust the analysis.

| Analytical Layer |

Key Question |

Typical Input |

| Parameter Layer |

What is publicly disclosed? |

Total supply, tax rate, LP status statements |

| On-Chain Layer |

Is on-chain data consistent? |

Supply, holdings, LP destination, permissions |

| Behavioral Layer |

Does narrative match behavior? |

Social media rhythm, discussion density, liquidity actions |

This framework prevents single-point judgment. Even if a parameter appears positive, if on-chain or behavioral evidence does not match, conclusions should be cautious. The behavioral layer can be referenced against the staged content rhythm described in Roadmeow and Community Growth to see if parameter narratives are being amplified or distorted in sync with community promotion phases.

Figure 1. Three-layer interpretive framework for CASHCAT: parameter, on-chain verification, and behavioral layers.

Figure 1. Three-layer interpretive framework for CASHCAT: parameter, on-chain verification, and behavioral layers.

What Are the Most Common Pitfalls in Parameter Analysis?

Common mistakes include: equating 0 tax with low risk, equating LP burned with absolute safety, ignoring holding concentration, and relying on screenshots instead of on-chain data. Another frequent error is evaluating meme projects with a protocol revenue model, leading to mismatched metrics. Parameter analysis should support risk identification, not replace it.

Another pitfall is treating “screenshots as evidence”: social media parameter cards, chat logs, or edited images may not reflect the current contract state. The safer approach is to cross-reference public websites and blockchain explorers, then conduct small-scale test transactions. Stepwise verification at the operational level can be combined with the preparation, trading, and review steps outlined in How to Participate in CASHCAT.

Advantages, Risks, and Limitations of Interpreting CASHCAT Parameters

The advantage is clear parameter disclosure, making it easy to quickly start research: total supply, tax rate, and LP status are listed together, lowering information retrieval costs for newcomers. For content analysis, these parameters serve as a starting “verification checklist,” not as the final word.

The risk is that during periods of high attention, information noise increases and out-of-context dissemination becomes common. Counterfeit contracts, incorrect tax screenshots, and unverified “burned” claims can all spread on social media. The simpler the parameters, the easier they are to be repeated out of context, amplifying information risk.

The limitation is that parameters alone have limited explanatory power and cannot independently capture sentiment swings, liquidity crunches, or operational errors. Meme asset price discovery relies heavily on narrative and liquidity, and tokenomics can only constrain certain mechanism variables. For a more systematic analysis of boundaries, see CASHCAT Risks and Limitations. Note: CASHCAT is not officially affiliated with Robinhood, and parameter interpretation should not be viewed as platform endorsement.

Summary

CASHCAT tokenomics provides a “quick project outline” entry point, but not a full conclusion. The most effective approach is to place the 1B total supply, 0/0 tax, and LP burned into a verifiable framework, continually cross-checking on-chain data and community behavior. Parameters can help reduce information noise, but cannot substitute for disciplined risk management and verification.

FAQ

Does a 1B Total Supply Alone Indicate Project Quality?

No. Total supply is only a basic descriptor—the key is the allocation structure, holding concentration, and actual circulation. Without this information, the total supply figure is not very informative. 1B is best used to express a supply cap, not as a quality metric.

Does a 0/0 Tax Rate Mean Safer Trading?

A 0/0 tax rate only simplifies the transaction fee structure; it does not reduce volatility risk. Price risk is still determined by market sentiment and liquidity. A comprehensive safety assessment requires more dimensions, such as holding distribution, pool depth, and verification of information sources.

Can LP Burned Completely Eliminate Risk?

No. It may reduce some liquidity control risks, but cannot address contract, market, or information risks. Treat it as one variable in the risk structure, and always verify LP destination and contract permissions on-chain—it is not a final conclusion.

Why Should Parameters Be Reviewed Alongside On-Chain Data?

Because parameter statements can be misread or distorted in secondary dissemination. On-chain data provides verifiable facts and is the foundation for checking parameter authenticity and consistency. Comparing parameter, on-chain, and behavioral layers yields a more robust analytical framework.

How Does CASHCAT Tokenomics Differ from Typical Meme Coins?

The difference is rarely in “whether total supply and tax rate are disclosed,” but in how narrative anchors, chain context, and community communication templates organize these parameters. CASHCAT presents its parameters within the Robinhood Chain meme narrative; for cross-project comparison, review the narrative sources and parameter conventions of typical meme coins.

What Should Be Done After Interpreting Parameters?

After interpreting parameters, always conduct contract verification, small test trades, and authorization reviews as part of operational discipline. Tokenomics only describes “how the mechanism is presented,” not path security or position management. Rely on public websites and blockchain explorers as information sources, and note that the project is not officially affiliated with Robinhood.