The decentralized derivatives market has long faced persistent challenges with liquidity shortages and limited trading depth. Unlike centralized exchanges, which leverage professional market makers and significant capital resources, many on-chain trading platforms must independently establish liquidity pools—leading to diminished capital efficiency and fragmented market liquidity.

The launch of CyberDEX introduces a novel approach. Built as a perpetual futures trading platform on the Optimism network, CyberDEX forgoes building its own liquidity infrastructure and instead directly integrates with the shared liquidity network established by Synthetix. This strategy enables CyberDEX to access deeper liquidity, deliver a more stable trading experience, and minimize protocol scaling costs.

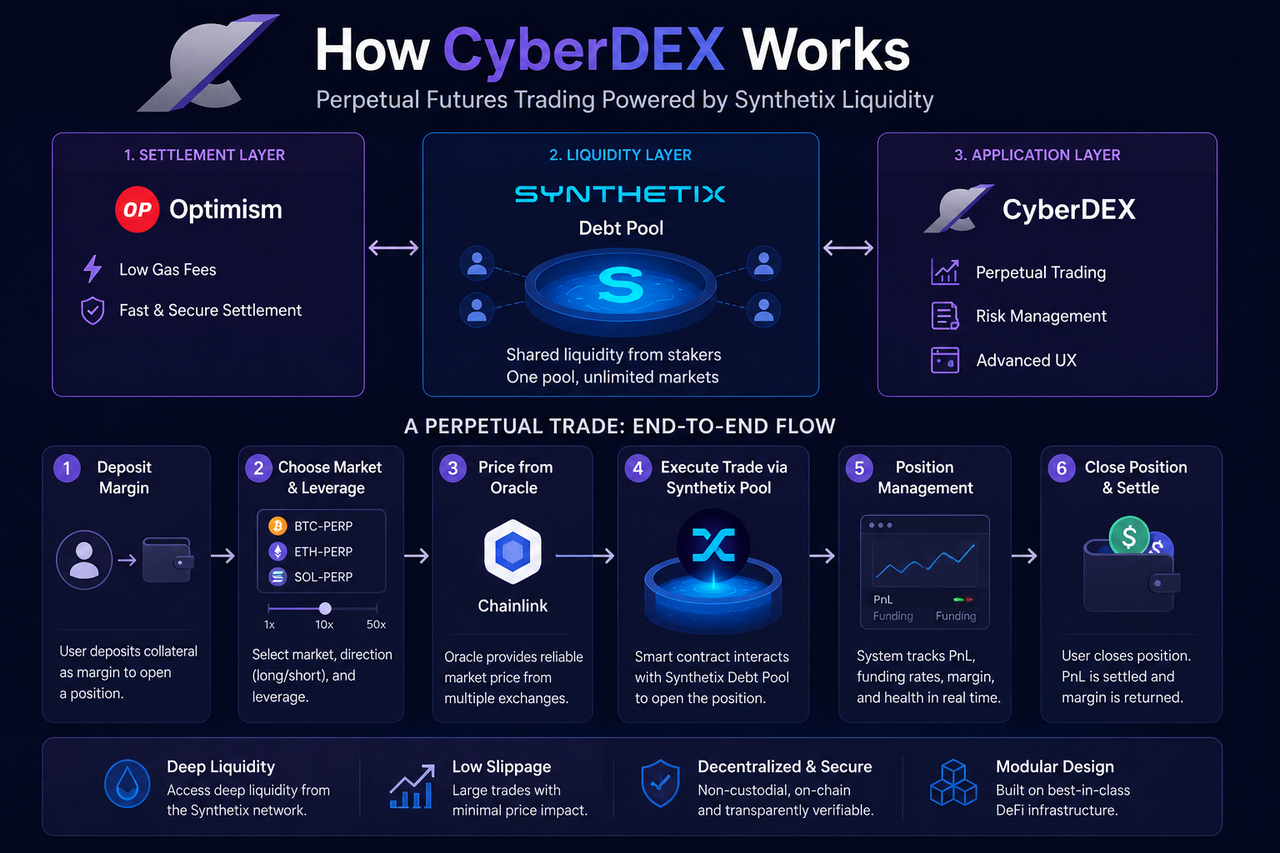

What Is the CyberDEX Trading Architecture?

CyberDEX’s trading architecture is composed of three distinct layers: the Optimism settlement layer, the Synthetix liquidity layer, and the CyberDEX application layer. Together, they form a comprehensive on-chain derivatives trading system.

Optimism manages trade execution and on-chain settlement with low gas costs and high efficiency. Synthetix supplies a unified liquidity pool and the foundational synthetic asset infrastructure. CyberDEX is responsible for order management, the trading interface, and overall user experience.

This layered approach means CyberDEX does not shoulder the burden of building liquidity, allowing it to focus on product innovation and the development of advanced derivatives trading features.

| Architecture Layer |

Core Protocol |

Core Functionality |

| Application Layer |

CyberDEX |

Trading interface and features |

| Liquidity Layer |

Synthetix |

Shared liquidity provision |

| Settlement Layer |

Optimism |

On-chain execution and settlement |

This structure stands in stark contrast to traditional exchanges, where all functions are centralized within a single system.

How Does the Synthetix Debt Pool Provide Liquidity?

Synthetix’s core innovation is its Debt Pool mechanism. Unlike conventional liquidity pools, which require users to deposit specific trading pair assets, Synthetix aggregates all staked assets into a single, unified liquidity source.

When users stake assets to mint synthetic assets, they collectively enter the system's Debt Pool. All stakers share the system’s debt and jointly benefit from trading fees and ecosystem incentives.

Once CyberDEX connects to this liquidity network, users no longer need to find counterparties to open positions—they transact directly with the Debt Pool. Regardless of market direction, the unified liquidity pool ensures robust market depth.

This model resolves the liquidity fragmentation that plagues many traditional DeFi trading platforms, while significantly improving capital efficiency.

How Does CyberDEX Achieve Low Slippage?

Slippage typically arises when market depth is lacking. Large trades consume multiple orders in the market, causing fill prices to deviate from expectations.

By adopting a shared liquidity model, CyberDEX eliminates reliance on individual trading pairs or isolated capital pools. Instead, it sources liquidity from the entire Synthetix network’s unified pool.

With all trades drawing from the same liquidity source, the market can accommodate larger trades and reduce price impact risk. This is a key reason why Synthetix-based derivatives platforms can deliver an institutional-grade trading experience.

That said, slippage cannot be entirely eliminated. Extreme market volatility or high liquidity utilization can still result in price deviations.

How Do Chainlink and Oracles Deliver Price Data?

The stability of perpetual futures markets depends on accurate pricing data. Any discrepancy in price feeds can trigger erroneous liquidations, arbitrage exploits, and systemic risk.

CyberDEX utilizes on-chain oracles to acquire real-time external market prices for both trade execution and risk management. These oracle networks aggregate data from multiple sources to provide robust price feeds.

When users open or close positions, the system ignores order book quotes and instead uses oracle prices for calculations. This approach reduces the scope for market manipulation and enhances trading fairness.

Oracle prices are mainly used for:

-

Position opening

-

Position closing

-

Margin calculations

-

Funding rate settlements

-

Liquidation assessments

As such, oracles serve as a vital component of the CyberDEX trading architecture.

How Does a Perpetual Futures Trade Execute?

From the user’s perspective, the CyberDEX trading flow resembles that of a centralized exchange, but the underlying execution logic is entirely on-chain and smart contract-driven.

Users first deposit margin on the platform and select their trading market. Next, they configure leverage and position direction, with the system calculating the maximum allowable position size using current oracle prices.

Upon order submission, a smart contract interacts with the Synthetix liquidity pool to execute the trade and record position data. Throughout the position’s lifetime, the system continuously updates floating PnL and funding rate changes.

When the user closes the position, the smart contract again references the oracle price to calculate final PnL and settle the assets.

The streamlined process is as follows:

| Stage |

System Action |

Core Functionality |

| Margin Deposit |

Lock trading funds |

Trading interface and features |

| Open Position |

Tap Debt Pool liquidity |

Shared liquidity provision |

| Position Holding |

Real-time PnL calculation |

On-chain execution and settlement |

| Funding Rate Settlement |

Adjust long-short balance |

|

| Close Position |

Settle PnL |

|

All operations are fully automated via on-chain smart contracts, eliminating the need for centralized intermediaries.

How Does CyberDEX Compare With AMM DEXs?

While CyberDEX is often compared to AMM-based DEXs like Uniswap, the two serve different markets and rely on fundamentally different mechanisms.

AMMs use a liquidity pool pricing model, with prices determined by the asset ratio within the pool. As trade size grows, prices shift, causing slippage.

CyberDEX, in contrast, leverages an oracle-driven perpetual futures model. Prices are pegged to external market data, and liquidity is supplied by the shared Debt Pool.

| Comparison Metric |

CyberDEX |

AMM DEX |

| Product Type |

Perpetual Futures |

Spot Trading |

| Liquidity Source |

Debt Pool |

LP Liquidity Pool |

| Pricing Model |

Oracle Price |

AMM Curve |

| Counterparty |

Shared Liquidity Pool |

Liquidity Pool |

| Main Use |

Leverage & Hedging |

Token Swaps |

Although both are DeFi trading platforms, they address distinct user needs.

Advantages and Limitations of CyberDEX’s Operational Model

CyberDEX’s primary advantage is its shared liquidity architecture. By leveraging Synthetix’s established liquidity network, the platform avoids duplicating liquidity pools, boosts capital efficiency, and offers deeper market depth to users.

The modular design allows CyberDEX to concentrate on product innovation without the responsibility of managing underlying liquidity. This division of labor drives the DeFi ecosystem toward greater specialization and maturity.

However, reliance on shared infrastructure means CyberDEX’s operations are contingent on upstream protocols. If the Synthetix liquidity layer or oracle systems malfunction, CyberDEX’s trading functions may be affected. Inter-protocol dependencies are a critical challenge for this model.

Summary

CyberDEX’s fundamental operating model is built on Synthetix’s shared liquidity network. When users trade perpetual futures on CyberDEX, they interact directly with the unified Debt Pool, rather than relying on order book matching or AMM liquidity pools.

By positioning Optimism as the settlement layer, Synthetix as the liquidity layer, and CyberDEX as the application layer, the platform delivers a modular DeFi derivatives trading architecture. This design enhances capital efficiency and establishes a new infrastructure paradigm for the evolving on-chain derivatives market.

FAQs

Why Doesn’t CyberDEX Need Traditional Market Makers?

CyberDEX leverages the Synthetix Debt Pool for unified liquidity. Trades are executed directly with the shared pool, eliminating the need for traditional market makers to maintain market depth.

Where Does CyberDEX’s Liquidity Originate?

CyberDEX’s liquidity is sourced from the Synthetix Debt Pool, which aggregates all staked assets. This collective pool forms a unified source of market liquidity.

Does CyberDEX Use an Order Book?

CyberDEX does not employ a traditional order book. Trade prices are determined by oracle data, with execution handled via smart contracts and the shared liquidity pool.

How Does CyberDEX Minimize Slippage?

Since liquidity is pooled from the entire Synthetix network, market depth is enhanced and large trades cause less price impact compared to isolated pools.

How Does CyberDEX’s Liquidity Mechanism Differ From GMX?

CyberDEX relies on the Synthetix Debt Pool for liquidity, while GMX uses a GLP multi-asset liquidity pool. Both employ shared liquidity models, but their underlying structures and risk-sharing mechanisms differ.