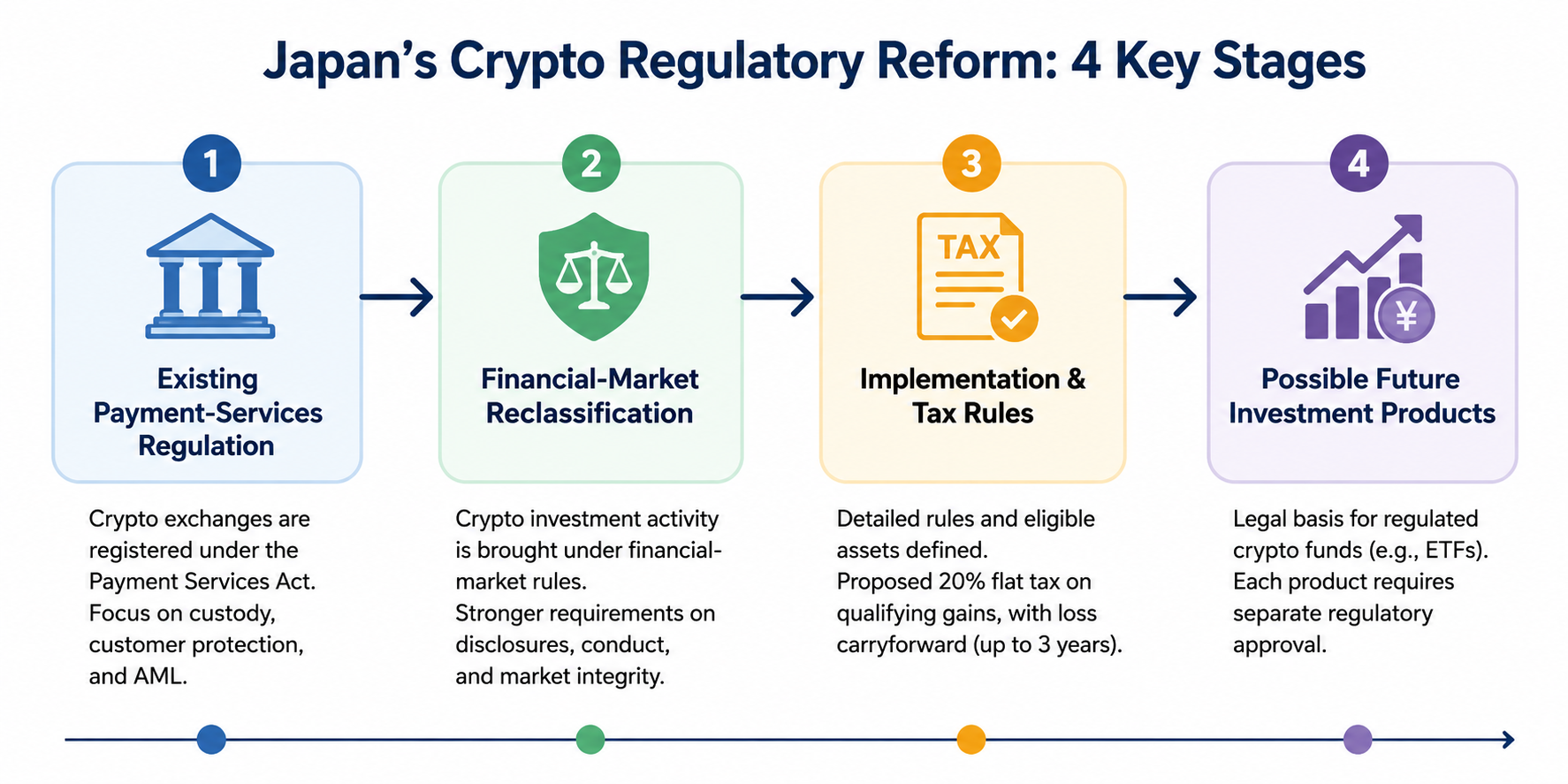

Japan has approved legislation that places crypto investment activity within a stronger financial-market regulatory framework. The change moves the country beyond treating crypto mainly as transferable digital value under payment-services rules and brings investment disclosures, market conduct, and investor protection more directly within financial regulation.

For investors, the reform may eventually affect how qualifying crypto gains are taxed, what information businesses must disclose, how unfair trading is investigated, and which regulated investment products can hold crypto assets.

The changes should not be interpreted as an immediate tax cut or blanket approval of crypto exchange-traded funds. Japan’s tax outline makes the proposed tax treatment dependent on amendments to financial-market legislation and ties its application date to the law’s commencement.

What Has Japan Changed?

Japan has regulated domestic crypto exchanges under the Payment Services Act since 2017. Businesses exchanging crypto assets for legal tender must register, follow custody requirements, and comply with customer-protection and anti-money-laundering obligations. The Financial Services Agency continues to maintain this registration framework.

The new reform does not simply erase those rules. Instead, it broadens the regulatory structure by treating crypto investment activity more like activity in a financial market.

This distinction matters because payment regulation and investment regulation address different risks. Payment rules focus on custody, transfers, exchange operations, and safeguarding customer assets. Financial-market rules place greater emphasis on disclosures, solicitation, conflicts of interest, price formation, and unfair trading.

| Regulatory Area |

Earlier Main Emphasis |

Direction Under the Reform |

| Crypto classification |

Transferable value and payment use |

Investment and financial-market characteristics |

| Business oversight |

Exchange registration and custody |

Expanded conduct and disclosure obligations |

| Investor information |

Platform and listing controls |

More structured information about eligible crypto assets |

| Market abuse |

General exchange supervision |

Stronger rules against unfair or information-based trading |

| Tax treatment |

Generally taxed with other miscellaneous income |

Proposed separate taxation for qualifying transactions |

| Investment funds |

Significant legal limitations |

Potential basis for future regulated crypto funds |

Calling crypto a financial asset does not mean every token becomes a share, bond, or conventional security. Crypto holders do not automatically receive ownership, voting, dividend, or creditor rights. Those rights depend on the design and legal terms of the individual asset.

How Could Japan’s Crypto Tax Rules Change?

Japan’s Ministry of Finance has outlined a separate 20% tax rate for certain crypto disposals. The proposed rate consists of 15% national income tax and 5% local resident tax. It would apply only to specified crypto assets transacted through businesses covered by the future regulatory framework.

The outline also allows qualifying losses that cannot be fully offset in the year they arise to be carried forward for up to three years and deducted from future qualifying crypto gains. It separately addresses eligible crypto derivatives and reporting duties for regulated businesses.

These details are important because the widely reported “20% crypto tax” is not a universal flat tax on every type of crypto activity.

The final rules must clarify the treatment of:

-

crypto assets not included in the relevant regulatory register;

-

transactions through overseas platforms;

-

decentralized exchange transactions;

-

wallet-to-wallet disposals;

-

staking, lending, mining, and airdrop income;

-

crypto received as payment;

-

derivatives linked to assets outside the qualifying category.

The Ministry of Finance states that the main separate-taxation provisions will apply from January 1 of the year after the amended financial law takes effect. That formula is more precise than assuming a fixed implementation year before the commencement date is officially confirmed.

Investors must therefore continue following the rules applicable at the time each transaction occurs.

How Could Investor Protection Improve?

Financial-market regulation may require more consistent disclosure of information that can materially affect an investor’s decision.

Depending on the final implementing rules, relevant information could include an asset’s issuance structure, supply, governance, technical design, conflicts of interest, price risks, and the responsibilities of businesses making it available to investors.

Market-conduct rules are another important part of the reform. Crypto prices can react sharply to exchange listings, token unlocks, project announcements, security incidents, or undisclosed business decisions. A clearer financial-market framework can give regulators stronger authority to address unfair trading involving material non-public information.

However, regulation cannot remove the underlying risks of crypto ownership. Investors may still face:

-

severe price volatility;

-

exchange or custodian failure;

-

wallet compromise;

-

smart contract vulnerabilities;

-

limited liquidity;

-

misleading token disclosures;

-

project abandonment;

-

changes in regulation or tax treatment.

Regulatory classification improves the framework for oversight. It does not certify that an individual crypto asset is safe, legitimate, liquid, or suitable for a particular investor.

No. Reclassifying crypto within an investment-focused framework does not automatically approve a spot Bitcoin ETF or another crypto fund.

The Ministry of Finance tax outline refers to future tax treatment for interests in certain investment trusts that invest in specified crypto assets. This suggests that the government is preparing a legal and tax framework capable of accommodating regulated crypto investment products.

A specific fund would still require its own regulatory review. Authorities would need to consider matters such as:

Investors should separate three different events:

-

The law permits a category of product.

-

Regulators publish detailed product rules.

-

A specific fund receives approval and becomes available.

Only the third event confirms that an investor can access a particular product.

What Should Investors Do Next?

The reform is best followed as a sequence rather than as a single announcement.

First, confirm the formal commencement date of the amended financial legislation. Second, review Financial Services Agency rules identifying covered businesses, eligible assets, disclosures, and market-conduct requirements. Third, check final tax guidance before assuming that a transaction qualifies for the 20% separate rate. Fourth, treat any crypto fund as unavailable until the specific product receives regulatory approval.

Investors should also retain complete transaction records, including acquisition dates, purchase costs, sale proceeds, fees, wallet transfers, exchange statements, and the Japanese-yen value used for reporting. A simpler headline tax rate does not eliminate the need to calculate gains accurately.

Summary

Japan’s crypto reform shifts investment activity toward a more formal financial-market framework while preserving relevant payment, custody, and exchange controls.

The reform creates the foundation for stronger disclosures, market-abuse enforcement, conditional 20% separate taxation, loss carryforwards, and possible regulated crypto investment funds. These outcomes depend on commencement dates, implementing regulations, eligible-asset definitions, and product-specific approvals.

The key investor takeaway is not that every change applies immediately. It is that Japan is building a more integrated regulatory structure in which crypto investment activity may be supervised and taxed more like other financial-market activity.

This content is for educational purposes only and does not constitute investment, tax, or legal advice. Digital assets involve market, liquidity, custody, technical, counterparty, and regulatory risks.

FAQs

Has Japan officially made every cryptocurrency a financial security?

No. Japan has moved crypto investment activity into a stronger financial-market framework, but that does not give every token the legal characteristics of a share, bond, or conventional security. The rights attached to an asset still depend on its structure and legal terms.

Is crypto income in Japan now taxed at 20%?

Not automatically. The Ministry of Finance has outlined a 20% separate rate for qualifying transactions involving specified crypto assets. The provisions are linked to the commencement of amended financial legislation and detailed eligibility requirements.

Can crypto losses be carried forward?

The tax outline provides for qualifying unused losses to be carried forward for up to three years and offset against future qualifying crypto gains, subject to the final requirements. It does not establish unrestricted loss offsetting against salary or unrelated income.

Has Japan approved a spot Bitcoin ETF?

No specific spot Bitcoin ETF is approved merely because the law has changed. The reform may provide a legal basis for future crypto investment funds, but regulators must publish detailed rules and approve individual products.

Will overseas exchange transactions receive the same tax treatment?

That remains subject to final guidance. The official outline connects the separate tax treatment to specified crypto assets and businesses operating under the relevant regulatory framework, so investors should not assume that every overseas or decentralized transaction qualifies.

Does stronger regulation remove crypto investment risk?

No. Regulation may improve disclosures and enforcement, but it cannot prevent volatility, technological failure, hacking, fraud, liquidity shortages, or losses caused by poor custody practices.