In most Web3 projects, Utility Tokens typically serve only fee or governance functions, making it hard to create a closed loop with actual business revenue. PLLD represents a tokenomics model that integrates "profit redistribution, supply management, and participation incentives" into a single framework: trading engine profits fund secondary market buybacks, the burn mechanism compresses the long-term supply ceiling, and staking and holding tiers raise user switching costs. As the market shifts from narrative-driven hype to verifiable cash flow, designs that map off-chain productivity onto on-chain token rules are more likely to be adopted in long-term evaluation frameworks.

From the overall architecture of Palladium Network, PLLD sits at the hub between the RWA asset layer, the algorithmic trading layer, and the application layer. In 2025, it completed its TGE, five public market buybacks, staking, and swaps; in 2026, it will advance real estate RWA NFTs and profit distribution, and complete the upgrade from PLLDv2 to PLLDv3 in May 2026. The following sections cover PLLD's functions, issuance and distribution, incentive logic, growth mechanisms, value drivers, risks, and long-term potential, explaining how the token is designed as an ecosystem growth engine and what on-chain and off-chain evidence to verify during evaluation.

Core Functions and Use Cases of PLLD

PLLD serves four functions within the Palladium Network:

- Liquidity Medium: Through Palladium Swap on Ethereum, PLLD can be exchanged for other assets, providing a unified unit of pricing and transfer within the ecosystem.

- Staking and Tiered Rights: Lock up assets to earn rewards; holding tiers may affect fee rates, event eligibility, or additional incentives (subject to DApp parameters).

- RWA Gateway: Real estate NFT subscriptions and profit collection are expected to be linked to PLLD holdings or staking, connecting on-chain tools with SPV properties.

- Growth Incentive Vehicle: The referral program rewards user acquisition, trading, and other actions in part with PLLD.

PLLD does not represent equity in SPV properties; rights are defined by contracts, NFT metadata, and offline legal documents. Holders receive utility and distribution rights under ecosystem rules, not direct claims to the underlying real estate registry.

As of May 2026, PLLDv3 is active (contract 0x396382F6048cEb0407e5B8F0b6FeFeEBd244c6F7), emphasizing architectural compatibility with subsequent RWA, staking, and swaps; v2 has been deprecated and can only be migrated via the official website interface or exchange announcements. The project has warned about counterfeit PLLD tokens on DEXs—always verify the contract source before interacting.

Token Issuance and Distribution Mechanism

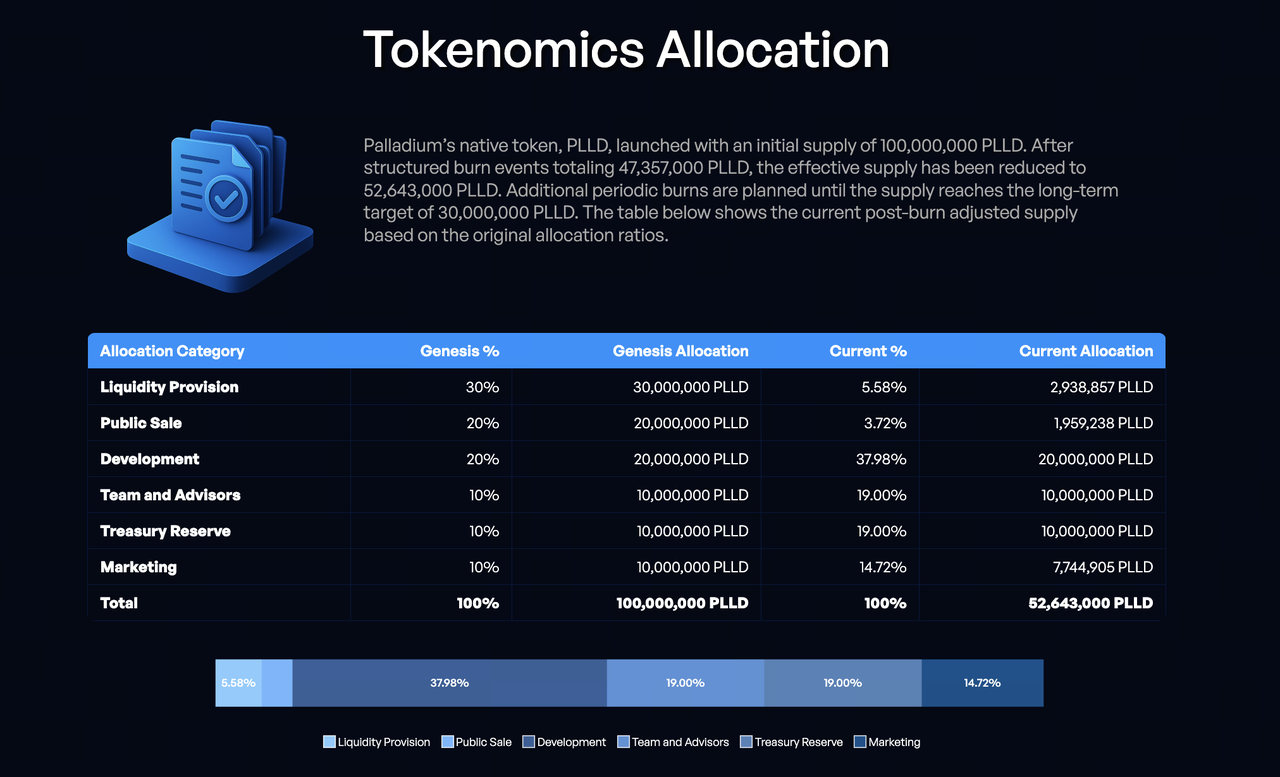

According to the Litepaper (v1.2), the genesis supply is 100 million tokens, with initial allocation: Liquidity 30%, Public Sale 20%, Development 20%, Team & Advisors 10%, Treasury 10%, Marketing 10%.

Approximately 47.357 million tokens have been burned, with a circulating supply of about 52.64 million, targeting a long-term supply of 30 million. After burns, official examples show: Team & Advisors and Treasury each account for about 19%, Palladium Network overall architecture Marketing approximately 14.72%, Liquidity and Public Sale combined less than 10%—early burns significantly altered the token distribution structure, making the circulating supply more sensitive to Sablier unlock schedules and Treasury buybacks.

Unlock Highlights:

- Development: Locks for 6 months post-TGE, then releases based on milestones.

- Team: Locks for 6 months plus 25-month linear release.

- Treasury: Locks for 12 months, then linear release.

- Marketing: Releases 25% at TGE, with the remaining 12-month linear release.

Buyback and Burn: Arbitrage profits enter a buyback pool, used to purchase PLLD on secondary markets at random intervals to reduce front-running from predictable windows; burns are sent to the Ethereum Null address, planned at least annually until approaching the long-term cap. The team states buybacks will be disclosed quarterly with scale and proof. Investors should cross-reference disclosed data with on-chain transfers and exchange trade records. In 2025, five public market buybacks were completed, and the 2026 roadmap includes a new round of burns—the "supply-side story" of tokenomic growth requires sustained realization of buybacks and burns over time to resonate with the "demand-side story" from staking.

PLLD Role in Ecosystem Incentives

Incentives revolve around "Retention—Activity—Expansion":

- Retention: Staking rewards and tier benefits increase the marginal benefit of long-term holding, reducing short-term selling pressure.

- Activity: Swaps increase PLLD turnover and depth, indirectly supporting buyback execution efficiency.

- Expansion: Referral commissions and linear marketing releases tokenize customer acquisition costs.

Unlike pure governance tokens, incentives partially derive from arbitrage profits and future RWA rental distribution, aiming to link to revenue rather than solely inflation—assuming engine profitability and property delivery meet expectations. Official sources also tie tier levels to longer holding periods, intended to convert "short-term speculation to sell-off" into "long-term participation to benefit sharing," complementing buyback and burn: the former manages demand-side behavior, the latter manages supply-side scale.

How PLLD Supports Network Growth and User Engagement

Palladium's growth flywheel can be summarized as: Arbitrage/Rental Cash Flow → Buyback and Burn Compress Supply → Strengthened Holding and Staking Expectations → Swaps and Referrals Drive New Users → Trading Engine and RWA Portfolio Expansion → Cash Flow Reinvested into Buybacks.

Typical User Path: Acquire PLLD via Swap and stake → Participate in RWA NFT presales for real estate exposure → Refer others for commissions → Track on-chain burns and buybacks to evaluate supply changes. For institutional or high-net-worth participants, the tokenomics offer another way to participate: without directly operating cross-exchange arbitrage bots, they can align with Treasury strategies through holding and staking; for retail users, tiered structures lower the "all-or-nothing" participation barrier, allowing different capital sizes to obtain differentiated rights under unified rules.

The key for the 2026 expansion year is whether the flywheel extends to the asset layer: if the first batch of real estate NFTs distributes property income as planned, PLLD incentives will for the first time connect with auditable RWA cash flows; if delayed, growth may still rely mainly on the engine and marketing. The PLLDv3 migration reduces friction for wallet and exchange integration but does not replace fundamental delivery. The trading engine covers 15+ exchanges with automated arbitrage (including standard and triangular arbitrage), remaining the realistic source of buyback funds—the "fuel" quality of tokenomic growth ultimately depends on the engine's sustainable profitability under real market conditions, not on the theoretical closure in a whitepaper.

Key Factors Influencing PLLD Token Value

Endogenous: Arbitrage profits (buyback funds), buyback and burn execution, staking rate and tier distribution, RWA NFT progress, Sablier unlock selling pressure.

Exogenous: Ethereum liquidity and Gas, global RWA regulation, competitor diversion, macro interest rates affecting risk assets and real estate valuations.

These factors can be summarized in a simple table:

| Type |

Typical Variables |

Transmission to PLLD |

| Revenue Side |

Arbitrage profits, property rents |

Affects buyback pool and RWA narrative credibility |

| Supply Side |

Burns, unlocks |

Affects circulating supply and market expectations |

| Demand Side |

Staking rate, Swap volume |

Affects selling pressure and ecosystem activity |

| Environment Side |

Macro market, regulation |

Affects valuation multiples and capital risk appetite |

Third-party data shows PLLD's market cap was at a high in early 2026, then corrected with the broader market—even with ongoing buybacks and burns, price may still closely follow crypto beta. Supply management is a necessary condition, not a sufficient one.

Risks to Consider When Investing in PLLD

- Model Risk: Arbitrage is not guaranteed profitable; RWA faces occupancy, legal, and SPV governance risks.

- Structural Risk: Unlock period selling pressure may dilute the deflationary narrative; if buybacks fall short of releases, the narrative weakens.

- Security Risk: Phishing and counterfeit tokens during migration (official warning in March 2026); use only the official PLLDv3 contract.

- Compliance Risk: Real estate tokenization and referral commissions are sensitive in some jurisdictions.

- Transparency Risk: Buybacks and burns must be independently verified on block explorers.

The above does not constitute investment advice.

Long-Term Development Potential of the PLLD Ecosystem

Short-Term (2026): Close the loop on RWA NFT profit distribution, execute burns, expand property portfolio, complete full PLLDv3 integration.

Medium-Term: Strengthen Swap interoperability, NFT secondary liquidity, and arbitrage strategy diversification to avoid over-reliance on a single strategy for revenue.

Long-Term: Official mentions of a proprietary chain and cross-chain bridge; if realized, PLLD could become a broader RWA + quantitative yield settlement unit, but the roadmap and regulation remain uncertain.

If RWA penetration increases and buybacks, burns, and property income become verifiable, PLLD may see allocation demand under a "utility + deflation + asset exposure" framework; conversely, it may merely reflect liquidity beta. Long-term potential depends on whether the three timelines—unlocks, buybacks, and RWA income—move in the same direction. Around March 2026, the project reached its one-year anniversary and continued to disclose buybacks, legal progress, and the Palladium NFT platform schedule—these public updates can serve as windows into execution capability, but must be cross-verified with on-chain records like Etherscan to avoid mistaking marketing pace for fundamental improvement.

Conclusion

PLLD stitches off-chain income, on-chain liquidity, and user behavior into a unified set of rules: Swaps and staking drive participation, buybacks and burns manage supply, RWA NFTs and the arbitrage engine provide value sources, and referrals and tiers amplify network effects. In 2025, the issuance and buyback infrastructure was consolidated; in 2026, PLLDv3 and RWA expansion will test whether the model can move from design completeness to verifiable delivery. Evaluation should balance Sablier unlocks, on-chain burn records, and NFT profit distribution—when these three lines move in the same direction, PLLD is closer to being an ecosystem growth engine; if any one lags, the growth logic requires re-examination. In a market environment that values verifiable cash flow, PLLD is a hybrid token experiment worth studying, but must be approached with independent due diligence and caution.