The U.S. consumer market is enormous, and credit-based purchasing has become a cornerstone of modern retail. From daily shopping and medical expenses to home renovations and electronics purchases, a vast array of consumer transactions rely on financing tools. Synchrony Financial delivers financial services within these consumption contexts, evolving into one of the most iconic companies in the U.S. consumer finance industry.

SYF Stock: Key Facts

Synchrony Financial originated from General Electric's (GE) financial arm, later spinning off as an independent public company dedicated to consumer finance. Unlike traditional commercial banks, the company doesn't focus on corporate lending or investment banking. Instead, it builds its operations entirely around consumer financing needs.

SYF is Synchrony Financial's ticker symbol on the New York Stock Exchange (NYSE). Headquartered in Connecticut, the company is a major force in the U.S. consumer finance landscape.

Today, Synchrony Financial partners with many retail brands, healthcare providers, and service companies nationwide. Its product suite spans credit cards, consumer loans, installment plans, and digital payment solutions. Within the U.S. consumer finance market, SYF has achieved significant market share and brand recognition.

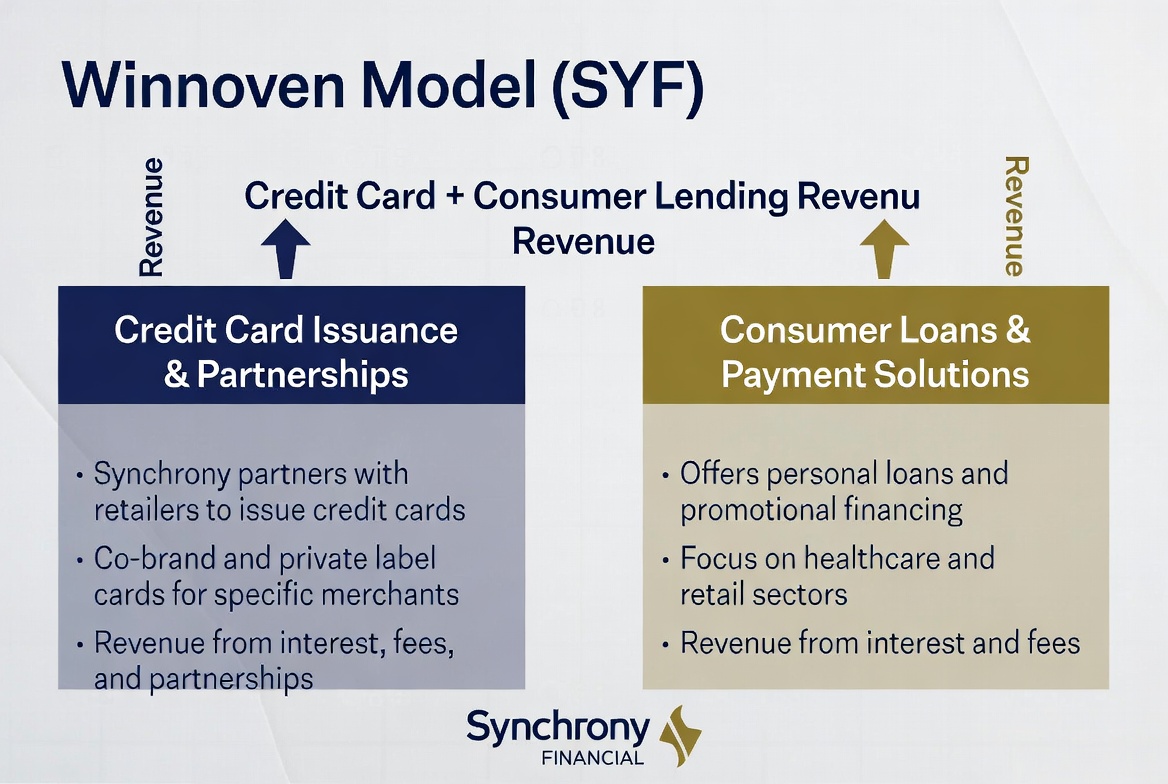

How Synchrony Financial Makes Money

Synchrony Financial's revenue model revolves around consumer credit. The company earns interest income by extending credit lines and financing to consumers, while long-term retail partnerships drive sustained business growth.

Compared to traditional banks, SYF's revenue is more closely tied to consumer spending and credit utilization. Every time a consumer uses a credit card, opts for an installment plan, or takes out a personal loan, Synchrony generates income from the funds deployed.

In summary, Synchrony Financial's revenue streams include:

| Revenue Source |

Description |

| Credit Card Interest Income |

Interest on outstanding credit card balances |

| Consumer Loan Income |

Installment payments and financing services |

| Merchant Partnership Income |

Co-branded card programs and retail collaborations |

| Fee Income |

Account servicing and related charges |

| Deposit Business Income |

Earnings from select deposit products |

This structure allows the company to benefit simultaneously from rising consumer spending and the expansion of its partner ecosystem.

How Credit Cards Drive Revenue

The credit card business is one of Synchrony Financial's primary revenue engines. Unlike many financial institutions, SYF zeroes in on retail-branded and co-branded credit cards rather than issuing general-purpose cards.

When consumers shop at partner merchants, they can pay using a Synchrony-issued card. If they carry a balance beyond the billing cycle, interest charges kick in—and this interest makes up a significant portion of the company's profits. Certain card products also generate account management fees and other service income.

For merchants, these credit card programs are more than just payment tools—they're customer retention engines. Through rewards, member benefits, and exclusive discounts, merchants can boost repeat purchases and transaction frequency. For Synchrony, this partnership model steadily expands its user base and creates a reliable stream of transaction volume.

The value of the credit card business isn't in individual transactions alone. It lies in the recurring income generated as consumers continue to use their credit lines over time. That makes customer retention and engagement critical growth drivers.

How Consumer Loans Fuel Growth

Beyond credit cards, consumer loan services are another key growth driver for Synchrony Financial. Many high-value purchases don't lend themselves to one-time payments, making installment financing a crucial enabler of consumption.

Furniture, home renovations, medical care, auto repairs, and major electronics are all classic consumer loan use cases. Consumers can make purchases upfront through financing and repay the principal over a set period.

For merchants, consumer loans lower the payment barrier, boosting conversion rates and average order value. For Synchrony Financial, higher loan balances mean more interest income, making consumer loans a vital part of its revenue mix.

As demand for flexible payment options grows, consumer loan services have evolved from a supplementary offering into an essential component of the modern consumer finance ecosystem.

How Retail Partnerships Expand the Customer Base

Synchrony Financial's retail partner network is a key competitive edge that sets it apart from traditional banks. The company focuses on building relationships with brands and retailers, embedding co-branded credit cards and financing services directly into the shopping experience.

In this model, consumers typically don't go looking for a financial institution. Instead, they encounter financial products at the point of sale—a furniture store, a medical clinic, or an electronics retailer—backed by Synchrony.

This acquisition strategy is highly efficient. Merchants see higher sales, consumers get payment flexibility, and Synchrony gains new customers. As the partner network grows, the company can cover more consumption scenarios and capture more market share.

This long-built partner network has become one of Synchrony Financial's most significant competitive moats and a powerful engine for ongoing expansion.

Why Risk Management Is Key to Profitability

The core challenge in consumer finance isn't customer acquisition—it's risk control. Since SYF extends credit to a large number of individual consumers, credit risk management directly determines the company's bottom line.

When default rates rise, the company must increase its loan loss provisions, squeezing profits. Conversely, a robust credit evaluation system that weeds out high-risk borrowers improves asset quality and boosts profitability. That's why risk management is widely regarded as the most critical capability for any consumer finance firm.

Synchrony Financial has invested heavily in data analytics and credit scoring, using consumer behavior data, credit history, and payment records to assess risk. This capability affects not only loan approval efficiency but also long-term financial performance.

In the consumer finance industry, growth matters—but risk control often determines whether a company can stay profitable over the long haul. That makes risk management a defining feature of Synchrony Financial's business model.

How to Buy SYF (Synchrony Financial) Stock

SYF is the ticker for Synchrony Financial on the New York Stock Exchange. Traditionally, investors can buy SYF through a brokerage account that supports U.S. equities, giving them exposure to the U.S. consumer finance sector.

Since Synchrony Financial's business spans credit cards, consumer loans, and retail financial services, its performance is influenced by consumer spending, interest rates, and credit conditions. Many market participants see SYF as a bellwether for the U.S. consumer finance market.

As digital assets and traditional finance converge, more trading instruments centered on stock price movements have emerged. For example, some platforms offer CFD products tied to stock prices, allowing users to participate through price changes without directly owning the underlying shares.

Take Gate TradFi as an example: users can track digital assets, stocks, ETFs, indices, and commodities from a single account. Select markets also offer Gate CFD products, giving users more options for cross-market allocation and price monitoring.

Regardless of the method, investors should fully understand the product structure, trading rules, and applicable regulations in their jurisdiction.

Key Takeaways

Synchrony Financial's business model is built on the consumer finance ecosystem. Through credit cards, consumer loans, and a vast retail partner network, the company connects consumers and merchants while generating revenue from spending activity. Meanwhile, risk management determines asset quality and profitability, making it a cornerstone of Synchrony Financial's long-term competitiveness. As digital payments and consumer finance continue to evolve, SYF has cemented its place as one of the most representative names in the U.S. consumer finance market.

FAQ

What is SYF's primary source of revenue?

Synchrony Financial generates revenue mainly from credit card interest, consumer loan interest, and financial service programs with retail partners.

Is Synchrony Financial a bank?

Synchrony Financial offers some banking-like services, but its core business is consumer finance, with a focus on credit cards and consumer loans.

Why is the credit card business such a major revenue driver?

Credit cards generate consistent interest income and service fees while offering high customer stickiness, making them a key profit center for consumer finance firms.

Why is the retail partnership model important?

Retail partnerships give Synchrony direct access to point-of-sale financing opportunities, boosting customer acquisition efficiency and scale.

Why does risk management affect consumer finance company profits?

Credit risk directly determines the level of bad debt. If default rates rise, the company absorbs more losses, so strong risk control improves profitability.

What's the difference between Synchrony Financial and Capital One?

Synchrony Financial focuses on retail partnerships and consumer credit, while Capital One is a broader financial institution with a wider range of products and services.