With the growth of Real World Asset (RWA) tokenization and decentralized finance (DeFi), more and more traditional financial assets are appearing on-chain. Among them, tokenized stocks and synthetic assets are the two most common stock-based on-chain products.

In the on-chain financial system, tokenized stocks represent a key direction for bringing real-world assets on-chain, while synthetic assets are a major innovation in DeFi derivatives. Although both are linked to stock prices, they differ fundamentally in asset source, operational logic, and risk structure.

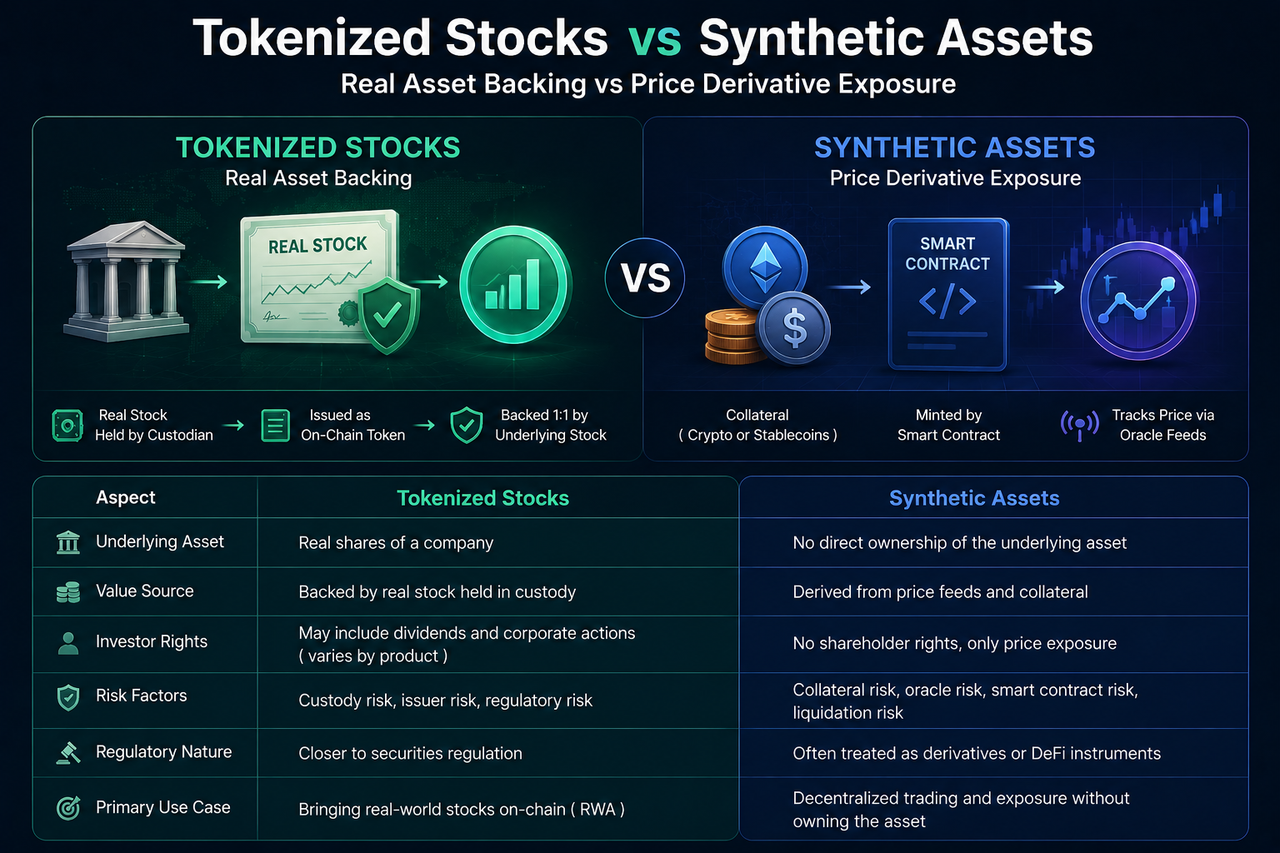

What Are Tokenized Stocks?

Tokenized stocks are a form of digital asset that maps real-world stocks onto the blockchain using blockchain technology.

In most models, the issuer first purchases real stocks and holds them with a regulated custodian. Then, on-chain tokens are issued at a certain ratio. For example, if the custodian holds one share of Apple stock, the issuer issues one corresponding stock token.

Therefore, the value of tokenized stocks comes from the actual underlying stock assets. Although investors hold on-chain tokens, their value is based on real stocks in the securities market.

This model is essentially the tokenization of real-world assets and is one of the most important use cases in the current RWA sector.

What Are Synthetic Assets?

Synthetic assets are a class of on-chain financial products that simulate the price performance of real assets through smart contracts and collateral mechanisms.

Unlike tokenized stocks, synthetic assets typically do not require actual ownership of the underlying stock.

The system uses collateral assets, oracle price data, and smart contract rules to create on-chain assets pegged to a specific stock price. For example, a user can hold a synthetic asset tracking Apple's stock price without the system itself holding any Apple shares.

In essence, synthetic assets are on-chain derivatives designed to replicate price performance, not to represent ownership of real assets.

What Is the Core Difference Between the Two Models?

The biggest difference between tokenized stocks and synthetic assets lies in whether they are backed by real assets.

Tokenized stocks are typically built on the foundation of real stock custody, with on-chain tokens corresponding to real stocks. Investors receive a representation of the value of real assets, and the market relies on real stock reserves and custody systems.

Synthetic assets, on the other hand, are built on price-tracking mechanisms. Their value comes from market prices provided by oracles, not from actual stock holdings. Investors gain exposure to price movements rather than the stocks themselves.

Simply put, tokenized stocks solve the problem of "how to bring real stocks onto the chain," while synthetic assets solve the problem of "how to replicate stock prices on-chain."

How Do the Asset Support Methods Differ?

The asset support structure determines the operational logic of the two products.

Tokenized stocks typically use a real stock custody model. The issuer first holds the underlying stocks and then issues on-chain tokens at a corresponding ratio. Therefore, the number of tokens is theoretically limited by the size of the real assets. If the custody account holds 1,000 shares, the system can generally only issue that same number of tokens.

Synthetic assets operate using a collateral mechanism. Users collateralize crypto assets or stablecoins and use smart contracts to generate synthetic assets pegged to stock prices. The issuance scale depends on the collateral value and system risk parameters, not on the number of real stocks.

Thus, tokenized stocks rely on real-world assets to support value, while synthetic assets rely on financial engineering to maintain price correlation.

Do Investors Receive the Same Rights?

Investor rights are one of the key differences between the two.

Because tokenized stocks have a mapping relationship with real stocks, some products may offer investors economic rights such as dividend payments and stock split adjustments. While they may not have full shareholder rights, their rights structure is typically linked to the underlying stocks.

Synthetic assets, on the other hand, are essentially price-tracking tools. Investors gain profits or losses from price fluctuations, not the economic rights attached to the stocks themselves.

For example, when a listed company pays dividends, a tokenized stock product may distribute corresponding returns to investors according to its issuance rules; a synthetic asset tracking the same stock price typically does not automatically receive dividend income.

Therefore, there are clear differences in investment characteristics and sources of returns.

How Do the Risk Sources Differ?

Although both tokenized stocks and synthetic assets provide exposure to stock markets, their risk structures differ significantly.

Tokenized stocks mainly rely on real stock custody and the operations of the issuing institution. Therefore, risks typically center on asset custody, reserve transparency, the issuer's ability to perform, and regulatory compliance. If the management of underlying assets has issues, or the issuer cannot maintain the mapping between tokens and stocks, investor rights may be affected.

In contrast, the risks of synthetic assets come more from the on-chain system itself. Because their value depends on collateral mechanisms, smart contracts, and price oracles, events such as sharp volatility in collateral assets, abnormal oracle prices, or smart contract vulnerabilities can lead to forced liquidations, price de-pegging, or insufficient liquidity.

In essence, tokenized stocks carry real-world asset management risks, while synthetic assets carry on-chain financial engineering risks.

Why Do Regulatory Attitudes Differ?

Regulators typically take different approaches to tokenized stocks and synthetic assets.

Since tokenized stocks directly involve real securities, they are often subject to securities regulatory frameworks. Issuers must handle asset custody, investor qualification reviews, and information disclosure, with regulatory logic similar to traditional securities markets.

Synthetic assets do not necessarily hold real stocks, making their legal status more complex. In some regions, regulators tend to treat them as financial derivatives; in other markets, they may be classified as digital asset innovations. Due to a lack of uniform standards, the regulatory environment for synthetic assets is typically more diverse than that for tokenized stocks.

This difference is also a major reason why the RWA and DeFi sectors follow different regulatory paths.

How Do Their Positions Differ in the RWA Sector?

Although both tokenized stocks and synthetic assets are related to stock prices, they belong to different development paths.

The core goal of tokenized stocks is to bring real-world stock assets onto the blockchain, enabling asset digitization and on-chain circulation. Therefore, they are considered a key part of the RWA sector. The focus is on asset mapping, custody mechanisms, and compliant issuance.

Synthetic assets emphasize native on-chain financial innovation. They do not require bringing real assets onto the chain; instead, they use smart contracts to build price-tracking tools. As a result, synthetic assets are more a part of the DeFi derivatives ecosystem, with development focus on collateral models, oracle mechanisms, and on-chain liquidity design.

From an industry perspective, tokenized stocks represent real-world assets going on-chain, while synthetic assets represent on-chain financial innovation. They solve different problems.

Comparison: Tokenized Stocks vs. Synthetic Assets

| Dimension |

Tokenized Stocks |

Synthetic Assets |

| Underlying Assets |

Real stocks |

No real stocks required |

| Source of Value |

Backed by stock assets |

Price-tracking mechanism |

| Asset Structure |

RWA mapping |

On-chain derivatives |

| Custody Requirement |

Requires a custodian |

Typically no stock custody needed |

| Dividend Rights |

Supported by some products |

Typically not supported |

| Issuance Limit |

Limited by quantity of real assets |

Limited by collateral size |

| Risk Source |

Custody and issuing institution |

Collateral and oracle systems |

| Regulatory Nature |

Similar to securities regulation |

Closer to derivatives regulation |

| Industry Position |

RWA sector |

DeFi sector |

Conclusion

Tokenized stocks and synthetic assets both offer exposure to stock prices, but their underlying logic is completely different. Tokenized stocks rely on real stock custody, mapping real-world asset value through on-chain tokens; synthetic assets use collateral mechanisms and price oracles to simulate stock price movements.

From an industry positioning standpoint, tokenized stocks are a key part of the RWA sector, while synthetic assets belong to the DeFi derivatives ecosystem.

FAQs

Are tokenized stocks and synthetic assets the same thing?

No. Tokenized stocks typically correspond to real stock assets, while synthetic assets mainly track price performance. Their underlying structures and sources of value are completely different.

Do synthetic assets require real stock backing?

Typically not. Synthetic assets generally simulate stock prices through collateral mechanisms, smart contracts, and price oracles, without actually holding the corresponding stocks.

Do tokenized stocks belong to RWA?

Yes. Tokenized stocks are an important use case of Real World Asset (RWA) tokenization, with the core feature of putting real stock assets on the chain.

Why are synthetic assets considered DeFi products?

Because synthetic assets primarily rely on smart contracts, oracles, and on-chain collateral mechanisms to operate, and their essence belongs to the decentralized financial derivatives system.

Which product has lower risk?

The risk structures differ. Tokenized stocks primarily face custody and regulatory risks, while synthetic assets primarily face oracle, liquidation, and smart contract risks. Therefore, a simple comparison of risk levels is not possible.