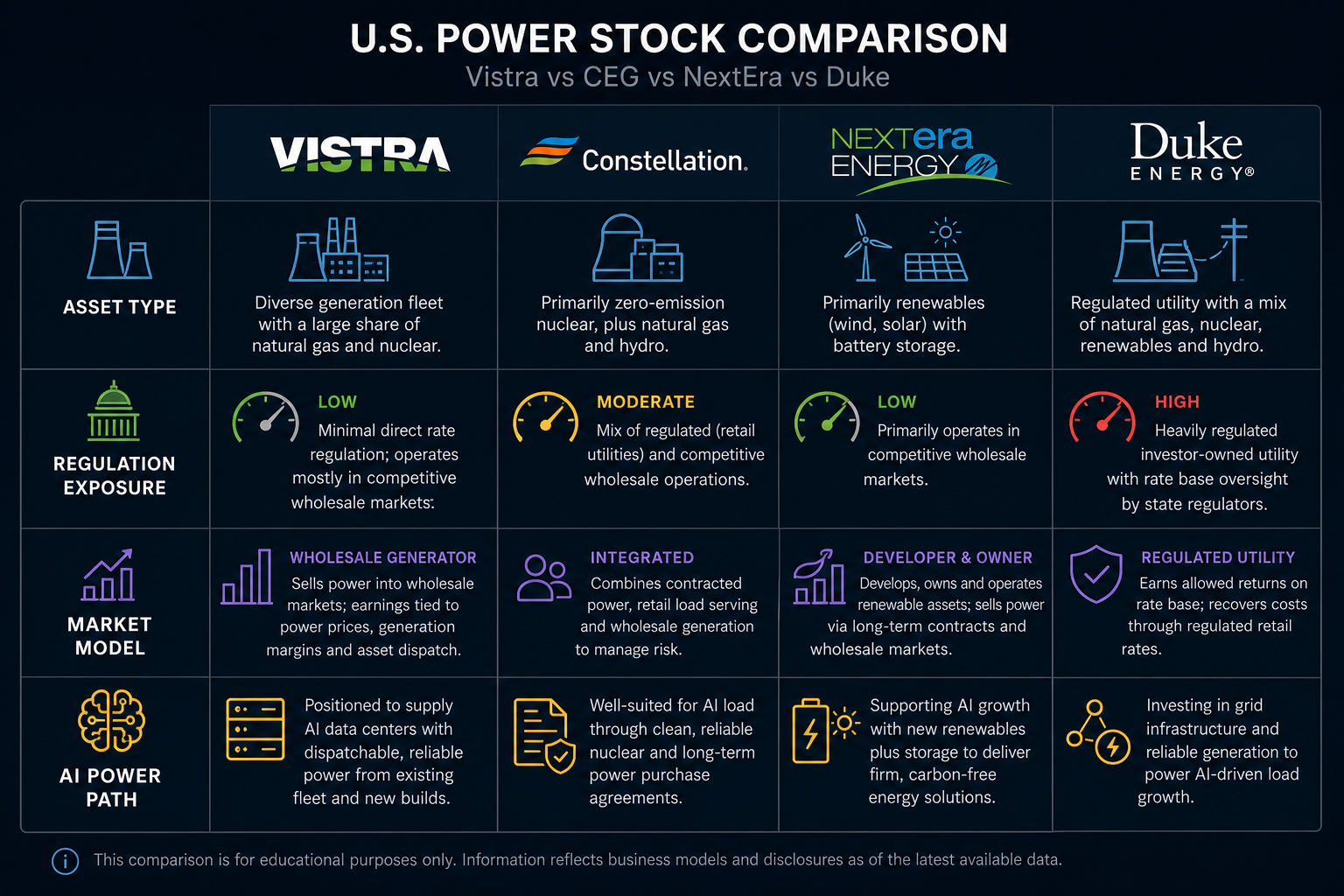

The primary distinctions among Vistra, Constellation Energy (CEG), NextEra Energy, and Duke Energy are rooted in their company structures and asset compositions. Vistra is characterized by its integrated approach to multi-asset power generation and retail electricity; CEG operates as an independent power producer with a core focus on nuclear energy; NextEra stands out for its emphasis on renewable energy and regulated utility operations; and Duke Energy most closely resembles a traditional regulated utility. While all four are publicly traded U.S. power sector stocks, their revenue drivers and risk exposures are fundamentally different.

A frequent pitfall when comparing power stocks is to focus solely on labels like “AI power demand,” “nuclear,” or “clean energy,” neglecting the underlying business models. Vistra (VST) is positioned as an integrated platform spanning retail electricity and power generation, with operations across both the ERCOT and PJM markets. To accurately assess sector differences, it’s essential to first determine whether a company is an independent power producer, a vertically integrated utility, a renewable energy platform, or a hybrid nuclear and natural gas entity—then separately analyze market-based generation revenue, regulated grid income, and retail contract structures.

Figure 1. Comparison of four U.S. power stocks: asset types, regulatory exposure, and market orientation all vary.

What Kind of Power Company Is Vistra?

Vistra Corp (VST) is a Fortune 500 integrated retail electricity and power generation company traded on the NYSE under the ticker VST. The company’s business model is built on a “generation + market + retail” platform, distinguishing it from single-technology generators and traditional regulated utilities.

Vistra’s generation mix includes natural gas, nuclear, coal, solar, and battery storage, with primary operations in ERCOT and PJM. Its retail brands—TXU Energy, Ambit Energy, Dynegy, and others—serve residential, commercial, and industrial customers. The company’s revenue is closely tied to generation asset performance, wholesale power prices, capacity values, retail contract structures, and fuel costs.

Relative to CEG, Vistra has a lower concentration of nuclear power, with natural gas, storage, and retail electricity playing more prominent roles and greater ERCOT market exposure. Analyzing Vistra’s business model requires examining its generation portfolio, wholesale market activities, and retail contracts to fully understand VST’s revenue structure.

What Kind of Power Company Is Constellation Energy (CEG)?

Constellation Energy (CEG) operates as a large-scale independent power producer and energy services provider, distinguished by its significant nuclear asset base and high proportion of clean, reliable electricity. CEG is listed on Nasdaq under the ticker CEG, with its primary nuclear assets concentrated in the PJM region.

CEG’s revenue streams include nuclear plant operations, energy and capacity markets, long-term power purchase agreements, and retail supply. Unlike Vistra’s diversified portfolio, CEG is more heavily weighted toward nuclear power, with a greater share of market-driven generation and contractual arrangements. The key distinction from Vistra lies in revenue recognition: Vistra’s natural gas and retail businesses alter the transmission of power price and fuel risks, while CEG more closely follows a nuclear-driven independent generator model.

What Kind of Power Company Is NextEra Energy?

NextEra Energy is best understood as a blend of renewable energy development and regulated utility operations. Its portfolio includes regulated utilities such as Florida Power & Light, as well as large-scale wind, solar, and storage projects under NextEra Energy Resources.

Critical variables for NextEra include installed wind and solar capacity, storage, transmission access, interest rates, and capital expenditures. Compared to Vistra and CEG, NextEra has less nuclear exposure and places greater emphasis on renewables and regulated rate frameworks. Vistra is more exposed to market-based pricing in ERCOT and PJM, while NextEra faces both project development returns and rate approval processes, requiring separate revenue analyses.

What Kind of Power Company Is Duke Energy?

Duke Energy most closely fits the model of a traditional regulated utility, with power generation, transmission, and distribution operations spanning the southeastern and midwestern U.S. Its revenue is closely linked to regulatory approvals, capital recovery, and regional demand. The key difference with Vistra is the split between regulated and market-based revenue: Vistra is directly exposed to wholesale price volatility, while Duke Energy’s income is primarily determined by regulatory rate cases, making direct valuation comparisons inappropriate.

At-a-Glance: Asset and Regulatory Differences

| Comparison Item |

Vistra (VST) |

CEG |

NextEra |

Duke Energy |

| Core Positioning |

Multi-asset generation + retail electricity |

Nuclear-focused independent generator |

Renewable energy + regulated utility |

Traditional regulated utility |

| Primary Listing |

NYSE |

Nasdaq |

NYSE |

NYSE |

| Nuclear Exposure |

High |

Very high |

Low |

Medium/region-specific |

| Natural Gas/Coal Exposure |

High |

Medium |

Low |

Region-dependent |

| Renewable Exposure |

Medium (solar, storage) |

Medium |

Very high |

Increasing |

| Retail Electricity Business |

Yes (TXU Energy, etc.) |

Yes |

Limited |

Regulated retail |

| Market Exposure |

High (ERCOT, PJM) |

High (mainly PJM) |

Medium |

Low |

| Regulatory Attribute |

Primarily market-based generation |

Primarily market-based generation |

Regulated + project development |

Highly regulated |

| Data Center Power Link |

Strong, broad-based supply |

Strong, 24/7 clean nuclear |

Strong, renewables and storage |

Linked to regional demand growth |

This table illustrates that U.S. power stocks cannot be analyzed solely on “power demand growth.” Vistra’s distinctiveness lies in its multi-asset portfolio and retail electricity presence, facing three major variables: wholesale market pricing, fuel costs, and retail competition.

How Do AI Power Demand Benefit Pathways Differ?

AI data centers have raised demand for reliable, continuous, and dispatchable electricity, but the benefit pathways are not the same. Vistra may gain exposure through nuclear baseload, natural gas peaking, storage, and retail contracts; CEG emphasizes stable nuclear baseload; NextEra participates via renewables and storage; Duke Energy’s exposure is more closely tied to regional demand and grid investment.

Data center electricity usage must be considered alongside grid interconnection approvals, transmission capacity, long-term power purchase agreements, and regulatory frameworks. AI data center power and PPA mechanisms can lock in some volumes, but plant upgrades, fuel costs, and ERCOT price volatility all impact execution. Focusing solely on demand growth without considering interconnection and contract fulfillment risks conflating the benefit pathways across these companies.

What Are the Limitations of Comparison?

Peer comparisons have inherent structural limitations. The four companies use different financial reporting standards, and market-based generation, regulated rates, retail gross margin, and project development revenue cannot be directly combined. Asset portfolios shift with M&A and plant retirements, so static classifications must be regularly verified against public disclosures; the VST risk metrics checklist breaks down nuclear operations, market exposure, and trading execution variables for cross-comparison. Regional market rules also differ greatly, meaning Vistra’s ERCOT exposure and CEG’s PJM nuclear assets face distinct pricing and capacity regimes.

AI data center electricity usage is a demand driver, not a guaranteed revenue stream. Trading page identification and business analysis should remain separate: when searching for VST on Gate Stocks, always confirm Vistra Corp; Buying VST on Gate Stocks covers search and order checks; the CEG vs Vistra vs NextEra vs Duke article under the Constellation Energy theme provides a parallel comparison from CEG’s perspective.

Summary

Vistra, CEG, NextEra, and Duke Energy are all influenced by U.S. power demand, but their business models differ significantly. Vistra’s core strength lies in integrated multi-asset generation and retail electricity; CEG is centered on nuclear and clean, reliable power; NextEra prioritizes renewables and regulated utilities; and Duke Energy operates as a traditional utility. When comparing these companies, first classify by asset type and regulatory exposure, then analyze AI data center demand, power markets, fuel costs, and execution risks—avoiding single-label shortcuts in place of comprehensive, multi-dimensional analysis.

FAQ

What Kind of Power Company Is Vistra?

Vistra (VST) is an NYSE-listed, integrated multi-asset generation and retail electricity platform. Its generation portfolio includes natural gas, nuclear, solar, storage, and coal, with major operations in ERCOT and PJM. Retail brands include TXU Energy and Ambit Energy, among others. Revenue is linked to wholesale power prices, fuel costs, and retail contracts.

How Does Constellation Energy (CEG) Differ from Vistra?

CEG is centered on nuclear assets, with higher concentration in PJM nuclear operations and functions more as a nuclear-driven independent generator. Vistra has a greater share of natural gas, storage, and retail electricity, with more significant ERCOT market exposure and a more diversified revenue and risk profile.

What Is the Core Difference Between Vistra and NextEra?

NextEra is more focused on renewable energy development and regulated utility operations, with large-scale wind and solar capacity. Vistra operates as an integrated, market-based generator and retailer, with revenue closely tied to ERCOT and PJM wholesale prices and natural gas costs. Its nuclear concentration is lower than CEG’s but higher than NextEra’s.

Can Duke Energy and Vistra Be Directly Compared?

They can be compared within the U.S. power sector, but not with the same valuation approach. Duke Energy’s revenue is primarily derived from regulated transmission, distribution, and rate approvals, with limited market exposure. Vistra is directly affected by wholesale price volatility and fuel cost changes.

Does AI Data Center Electricity Usage Affect All Four Power Stocks Equally?

Rising demand has increased the focus on reliable electricity, but the benefit pathways differ: Vistra has multi-layered exposure through nuclear baseload, natural gas peaking, and retail contracts; CEG focuses on 24/7 nuclear supply; NextEra emphasizes renewables and storage; Duke Energy’s exposure is tied to regional demand and grid investments. The impact cannot be assumed to be the same for all.