As the on-chain derivatives market expands, decentralized perpetual futures protocols are becoming a key component of Solana DeFi.

In the Jupiter Perps system, users trading long or short positions interact directly with the protocol's liquidity pool rather than relying on traditional order book matching. This design requires the liquidity pool to consistently provide sufficient asset depth to support user activities such as opening and closing positions and leveraged trading. In return, JLP holders earn protocol fees and potential profit distributions by taking on market risk.

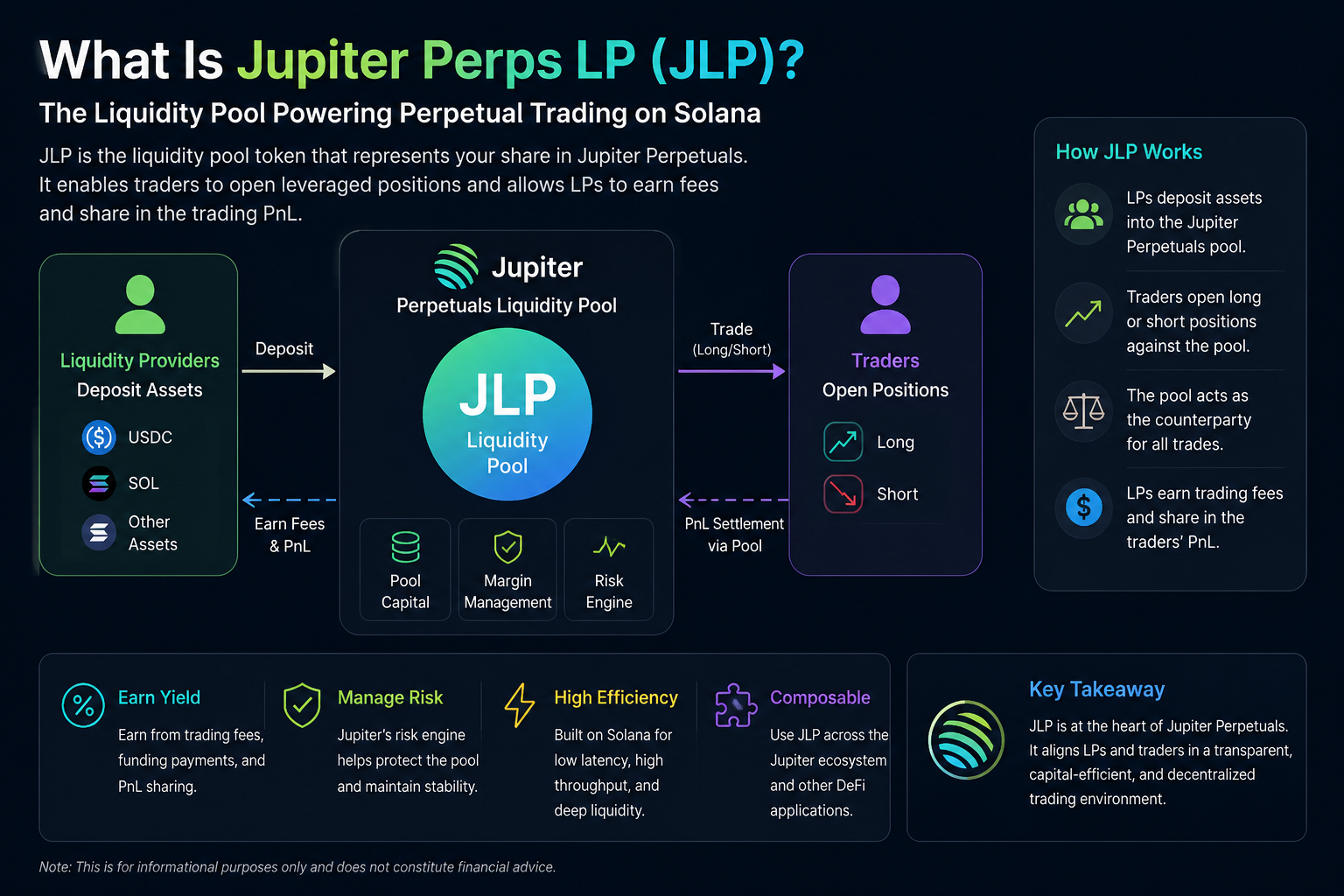

How JLP Works

JLP's operating logic is similar to certain on-chain perpetual protocols. Users who deposit designated assets into the Jupiter liquidity pool receive a corresponding amount of JLP based on their pool share.

When a trader opens a leveraged position on Jupiter Perps, the protocol's liquidity pool becomes the counterparty to that trade. For example, if a user goes long on an asset and realizes a profit, the pool may incur a corresponding loss. Conversely, when traders lose, the pool may gain.

Thus, JLP holders' returns are not solely derived from trading fees but are also influenced by overall market trading outcomes. If the majority of traders incur losses, the liquidity pool may see increased gains; if market movements result in substantial trader profits, the pool may face pressure.

This model positions JLP more as a "protocol market-making pool" rather than a standard liquidity mining asset.

What Are the Sources of JLP Returns?

JLP returns primarily come from protocol fees, funding rates, and the profit/loss structure of traders.

In the perpetual futures market, users typically pay fees when opening, closing, or adjusting leverage on positions. A portion of these fees flows into the liquidity pool, providing a return source for JLP holders.

Additionally, the funding rate mechanism in the perpetual market can affect the pool's overall returns. When market sentiment becomes unbalanced between longs and shorts, the funding rate rebalances capital flows accordingly.

Another critical factor is the aggregate profit/loss performance of traders. Because the liquidity pool serves as the counterparty, the long-term profitability of traders directly impacts the financial health of the JLP pool.

How Is JLP Different from Traditional LP Tokens?

Although JLP is also a liquidity pool asset, it differs significantly from LP tokens found in traditional AMMs.

Traditional DEX liquidity pools typically support spot swaps, with returns mainly derived from trading fees. JLP, however, operates within the perpetual futures market, exposing it not only to fee income but also to leveraged trading risk and market volatility.

Moreover, traditional LP tokens are more susceptible to impermanent loss, whereas JLP's risk profile is more heavily weighted toward trader profit/loss dynamics and directional market exposure.

| Comparison Dimension |

JLP |

Traditional LP Token |

| Use Case |

Perpetual Futures |

Spot AMM |

| Return Source |

Fees + Trading P&L |

Fees |

| Risk Structure |

Directional Market Risk |

Impermanent Loss |

| Liquidity Role |

Counterparty |

Asset Swap Pool |

| Leverage Linked |

Yes |

No |

What Role Does JLP Play in the Jupiter Ecosystem?

JLP is not only the core liquidity layer for Jupiter Perps but is also gradually becoming an integral asset within the broader Jupiter ecosystem.

Thanks to Jupiter's strong aggregation trading capabilities and deep connections with Solana DeFi, JLP can be easily integrated into lending, yield strategies, and on-chain asset management scenarios. This means JLP is more than just a single-protocol asset—it has the potential to evolve into a yield-bearing foundational asset across Solana DeFi.

What Risks Does JLP Face?

While JLP can deliver potential returns, its risk structure is considerably more complex than that of standard stable-yield assets.

First, JLP is exposed to market volatility. If a one-sided market trend emerges and a large number of traders profit, the liquidity pool may face significant loss pressure.

Second, the perpetual futures market inherently involves high leverage. When market liquidity is low or volatility spikes, the protocol may encounter liquidation pressure and risk management challenges.

Additionally, JLP carries smart contract risk, protocol governance risk, and risks related to the Solana network layer. For on-chain derivatives protocols, robust risk control mechanisms are even more critical than for typical DeFi protocols.

How Is Jupiter Perps Different from Protocols Like GMX?

Jupiter Perps and other on-chain perpetual protocols like GMX share certain design principles, such as using a liquidity pool as the counterparty.

However, the two operate in distinct ecosystems. GMX is primarily deployed on Arbitrum and Avalanche, while Jupiter is deeply integrated with Solana's high-performance trading environment. Solana's lower transaction costs and faster confirmation speeds make Jupiter better suited for high-frequency trading scenarios.

Furthermore, Jupiter's mature DEX aggregator system enables its Perps product to achieve stronger synergies with spot liquidity, routing systems, and other Solana DeFi protocols.

Summary

As the core liquidity asset in Jupiter's perpetual futures ecosystem, JLP supports leveraged trading and the operation of the on-chain derivatives market on Solana.

Unlike traditional LP tokens, JLP not only provides liquidity but also acts as the counterparty, resulting in a more complex return and risk structure. Protocol fees, funding rates, and trader profit/loss outcomes all influence JLP's overall performance.

FAQs

Where does JLP's return come from?

JLP returns are primarily derived from trading fees, funding rates, and the overall profit/loss structure of traders.

What is the difference between JLP and ordinary LP tokens?

Ordinary LP tokens are typically used for spot AMMs, while JLP is primarily designed for the perpetual futures market and bears counterparty risk.

Does JLP involve risk?

Yes, JLP is subject to market volatility, trader profitability, protocol mechanisms, and smart contract risks.

Is Jupiter Perps a DEX?

Jupiter Perps is an on-chain perpetual futures protocol, distinct from traditional spot DEXs, as it provides leveraged derivative trading functions.

Is JLP similar to GMX's GLP?

Both use a liquidity pool as the counterparty, but they differ in their deployment ecosystems, liquidity structures, and protocol synergy mechanisms.