TL;DR

- The Federal Reserve Bank of Dallas Q4 energy survey shows a second straight quarter of contraction, flagging persistent weakness in energy and higher odds of future supply-driven price spikes if underinvestment continues.

- Energy softness raises the chance of a cyclical pullback (~10%) in major indices like the S&P 500, which could still be consistent with a positive full-year outcome depending on timing.

- Growth remains intact and AI-driven optimism persists, but risks are increasingly uneven across sectors — arguing for selectivity and higher cash buffers.

- Key data ahead: Focus on delayed U.S. non-farm payrolls and unemployment (Fri, Jan 9) and CPI (Tue, Jan 13) for signals on labor strength and inflation persistence.

- Dollar easing: DXY is soft around ~98, reflecting expectations for further easing in 2026 and a narrowing U.S. rate advantage.

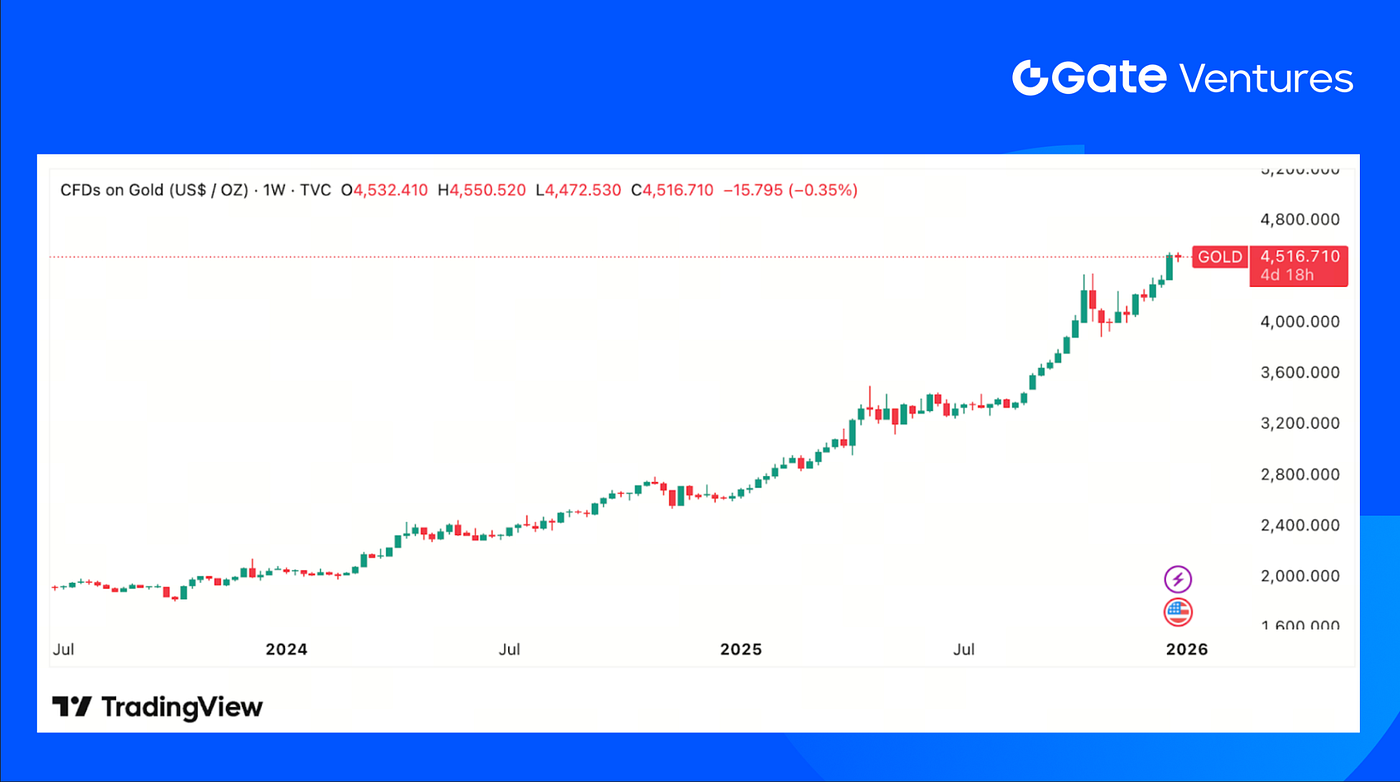

- Precious metals bid: Gold holds above ~$4,500/oz on rate-cut expectations and safe-haven demand; silver remains strong after briefly topping ~$80/oz, supported by inflation-hedge and supply-demand dynamics.

- Majors muted: BTC (-0.8%) and ETH (-1.76%) traded lower amid heavy ETF outflows (BTC: -$782m, ETH: -$102.34m). ETH/BTC slipped to 0.033, and sentiment stayed weak with Fear & Greed at 26 (Extreme Fear).

- Market cap divergence: Total crypto market cap was broadly flat (-0.7%). Ex-BTC/ETH was nearly unchanged (-0.07%), while ex–Top 10 surged +3.06%, signaling strength in smaller caps.

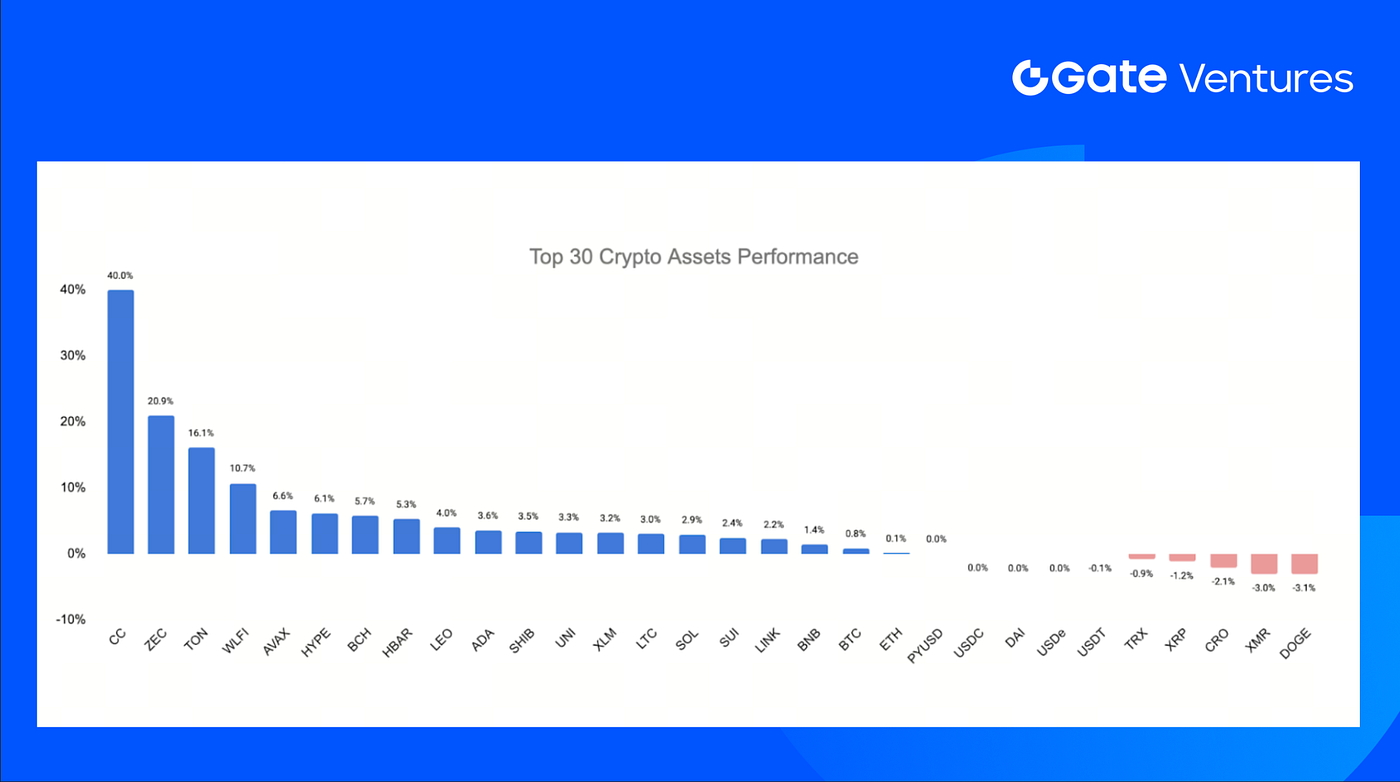

- Top 30 outperformance: Top 30 assets gained an average of +3.92%, driven by selective, catalyst-led moves.

- Canton Network standout: +40% on DTCC’s plan to tokenize U.S. Treasuries on Canton, highlighting institutional-grade RWA momentum.

- Toncoin strength: +16.1% following Telegram’s expansion of NFT-enabled gifts minted on TON.

- WLFI catalyst: +10.7% after a governance proposal to deploy < 5% of unlocked tokens to accelerate USD1 stablecoin adoption across DeFi and payments.

- Tether-linked firms buy Northern Data’s mining business for up to $200M.

- Coinbase strengthens regulated prediction markets with strategic The Clearing Company acquisition.

- DWF Labs settles first physical gold trade as crypto capital moves into commodities.

Macro Overview

Recent macro signals point to growing risks beneath an equity market that still appears strong on the surface. The Federal Reserve Bank of Dallas Q4 energy survey shows industry activity contracting for a second quarter in a row, highlighting ongoing weakness in the energy sector. Historically, low energy prices tend to correct themselves as reduced investment eventually tightens supply, but if the current slowdown persists, it raises the risk of sharper price increases later, which is similar to what happened in 2022. Industry executives also flagged policy uncertainty and a lack of alignment between policymakers and the energy sector as key concerns, weighing on confidence and future investment plans. (1)

This matters for the broader market because energy underpins much of the economy. Prolonged weakness increases the likelihood of a cyclical market pullback, even if major equity indices remain near record highs for now. Similar supply-cycle dynamics are emerging in other areas such as food and agriculture, where labor shortages and delayed production responses may push prices higher next year.

Combined with strong year-end equity momentum, elevated valuations, and continued optimism around AI-driven growth, the overall backdrop can be characterized as one of cautious optimism. The economy continues to expand, but risks are becoming more uneven across sectors, reflecting increasing divergence beneath the surface. In this context, any market correction would more likely represent a normalization of valuations rather than a signal of a deeper economic downturn, and could help reset market conditions as the cycle progresses.

This week’s incoming data includes the delayed non-farm payrolls and unemployment report which is scheduled for Friday, January 9, providing a key read on labor market conditions. Inflation data will follow with the Consumer Price Index (CPI) release on Tuesday, January 13, which markets will closely watch for signs of easing or persistence in price pressures. (2,3)

DXY

Following the recent Federal Reserve interest rate cut and ongoing market bets on additional easing in 2026, the U.S. Dollar Index has continued to soften, trading around the 98 level.

The yield on the 10-year note finished December 29, 2025, at 4.139%, and the 30-year note ended at 4.819%.

Gold

Gold prices have continued to hold elevated levels, recently trading above $4,500/oz, supported by rate-cut expectations, safe-haven demand, and broader macro risk concerns such as geopolitical tensions and elevated global debt levels.

Sliver

Silver has also seen notable strength, briefly surging past $80/oz before a modest pullback, reflecting strong investor interest as a hedge against inflation and supply-demand imbalances.

Crypto Markets Overview

1. Main Assets

BTC Price

ETH Price

ETH/BTC Ratio

BTC prices were largely unchanged, edging down 0.8% over the period, while ETH underperformed with a steeper 1.76% decline. On the flows side, BTC ETFs saw significant net outflows of $782m, and ETC ETFs recorded $102.34m in net outflows. (4)

The ETH/BTC ratio slipped a further 0.92% to 0.033, underscoring ETH’s continued relative weakness. Overall market sentiment remains fragile, with the Fear & Greed Index still anchored in “Extreme Fear” territory at a reading of 26. (5)

2. Total Market Cap

Crypto Total Marketcap

Crypto Total Marketcap Excluding BTC and ETH

Crypto Total Marketcap Excluding Top 10 Dominance

The total crypto market capitalization was broadly flat, edging down 0.7% over the period. Market cap excluding BTC and ETH was even more stable, slipping just 0.07%. In contrast, the market cap excluding the top 10 assets rose 3.06%, notably outperforming the broader market and signaling relative strength in smaller-cap tokens.

3. Top 30 Crypto Assets Performance

Source: Coinmarketcap and Gate Ventures, as of Dec, 29nd 2025

The top 30 cryptocurrencies by market capitalization posted an average gain of 3.92%, led by strong performances in Canton Network, Zcash, Toncoin, and World Liberty Financial.

Canton Network surged roughly 40%, significantly outperforming a broader crypto market that remained largely flat.

The rally was driven by Depository Trust & Clearing Corporation’s outlining its solid plans to tokenize the U.S. Treasury securities using the Canton Network infrastructure, starting with assets held at its Depository Trust Company subsidiary. DTCC’s CEO noted that the initiative establishes a roadmap for bringing institutional-grade, real-world tokenization use cases to market, with plans to expand beyond Treasuries to other eligible securities. (6)

Toncoin rallied 16.1%, supported by a product-driven catalyst from Telegram. The platform expanded its NFT-enabled gifts feature, which was first introduced in October 2024, allowing users to send animated gifts that can be minted as NFTs on the TON blockchain, reinforcing on-platform digital ownership and utility. (7)

WLFI advanced 10.7%, supported by a governance-driven catalyst at World Liberty Financial. The rally followed a proposal to allocate under 5% of unlocked tokens toward a targeted incentive program aimed at accelerating adoption of the USD1 stablecoin across DeFi protocols, payment gateways, and merchant services. (8)

The Key Crypto Highlights

1. Tether-linked firms buy Northern Data’s mining business for up to $200M

Northern Data, a data center operator majority-owned by Tether, sold its Bitcoin mining subsidiary Peak Mining for up to $200M to companies controlled by Tether executives, according to the Financial Times. The transaction, undisclosed at the time due to regulatory requirements, underscores the increasingly complex financial ties between Tether, Northern Data, and affiliated entities. Coming ahead of Rumble’s acquisition of Northern Data and amid ongoing regulatory scrutiny, the deal highlights how Tether is restructuring exposure across mining, data infrastructure, and strategic equity stakes beyond its core stablecoin business. (9)

2. Coinbase strengthens regulated prediction markets with strategic The Clearing Company acquisition

Coinbase agreed to acquire The Clearing Company, a prediction markets startup backed by Coinbase Ventures, as it accelerates its expansion into event-based trading. The deal follows Coinbase’s recent launch of prediction markets and will bring the startup’s team onboard to help scale the product, with closing expected in January. Founded by a former Polymarket and Kalshi executive, The Clearing Company was building a regulated, onchain prediction platform, reinforcing Coinbase’s strategy to broaden engagement beyond spot trading into real-world outcome markets. (10)

3. DWF Labs settles first physical gold trade as crypto capital moves into commodities

DWF Labs completed its first physical gold trade, settling a 25-kilogram bullion transaction using traditional custody and settlement infrastructure rather than blockchain rails. The move marks a rare step by a crypto-native market maker into legacy commodities, as gold prices hit record highs and outperform digital assets. DWF said the trade was a test tranche with plans to scale into other commodities, highlighting a broader trend of crypto firms diversifying revenue and exposure beyond purely onchain markets amid shifting macro conditions. (11)

Key Ventures Deals

1. Coinbax raises $4.2M Seed amid growing demand for compliant stablecoin rails and programmable payment layer

Coinbax raised a $4.2M Seed round led by BankTech Ventures with Connecticut Innovations, Paxos and other investors to build a programmable trust layer for stablecoin payments. The platform adds escrow, approvals, spend limits and policy enforcement to onchain settlement while preserving auditability for banks. As stablecoins move into core banking workflows under clearer regulation, the investment reflects demand for control infrastructure that enables institutions to deploy programmable payments without compromising risk and compliance. (12)

2. Architect raises $35M Series A to scale institutional perps exchange

Architect Financial Technologies raised a $35M Series A led by Miami International Holdings and Tioga Capital with Galaxy Ventures, ARK Invest, VanEck, Coinbase Ventures and other investors to scale AX, a regulated perpetual futures exchange for traditional assets. Operating under Bermuda’s regulatory regime, AX offers perps on FX, rates, equities and commodities for institutions. As demand grows for capital-efficient, always-on derivatives beyond crypto, the round reflects interest in bringing perpetuals into compliant global market infrastructure. (13)

3. Rocket lands $1.5M Seed to launch continuous-reward prediction markets

Rocket raised a $1.5M Seed round led by Electric Capital with Tangent, Amber Group, Bodhi Ventures and other investors to launch real-time, non-binary prediction markets with continuous payouts. The protocol lets users reuse capital across multiple predictions without liquidation risk. As traders seek exposure to information and sentiment without perp-style leverage constraints, the investment reflects demand for new market structures that monetize accuracy while aligning incentives around price discovery and real-time forecast. (14)

Ventures Market Metrics

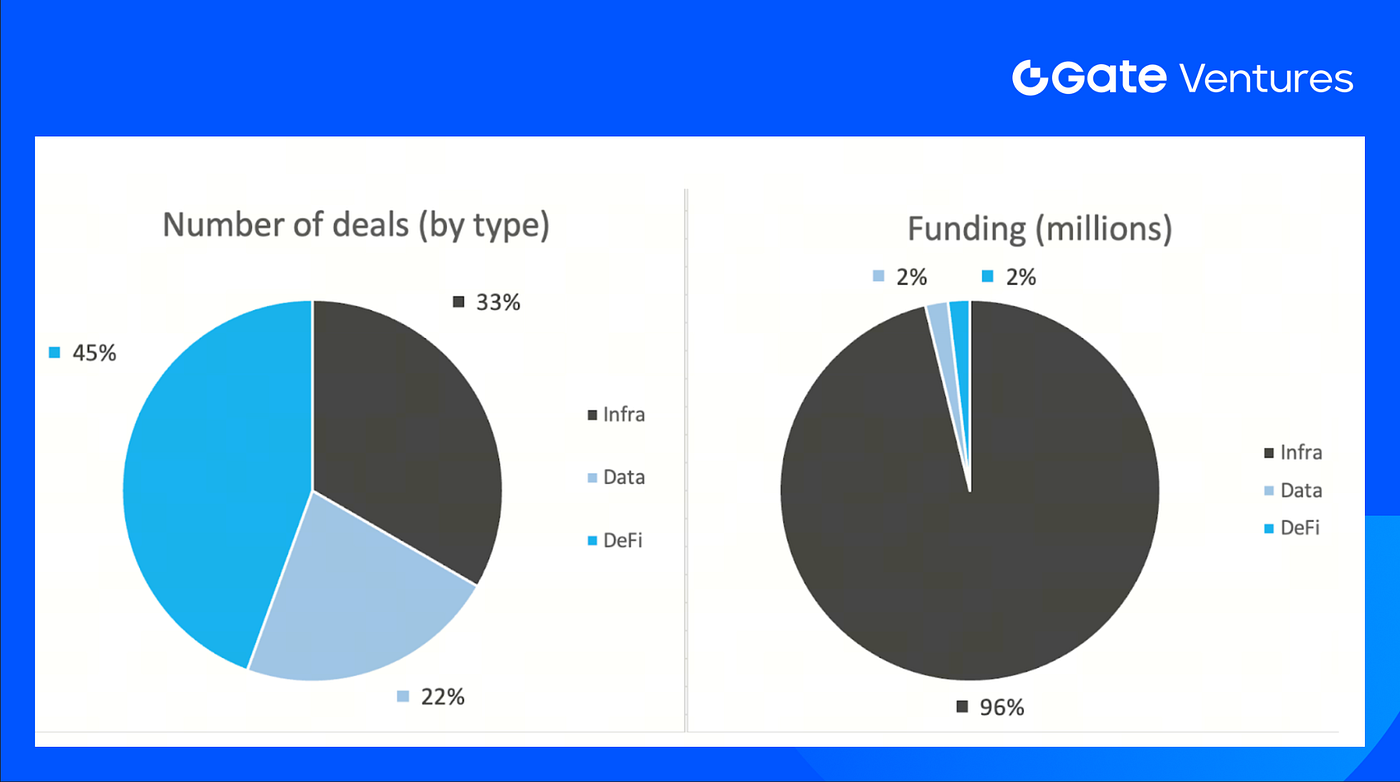

The number of deals closed in the previous week was 9, with DeFi having 4 deals, representing 44% of the total number of deals. Meanwhile, Infra had 3 (33%), and Data had 2 (22%).

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 29th Dec 2025

The total amount of disclosed funding raised in the previous week was $296M, 4/9 deals in the previous week didn’t announce the raised amount. The top funding came from the Infra sector with $207M. Most funded deals: HashKey $250M, Architect $35M.

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 29th Dec 2025

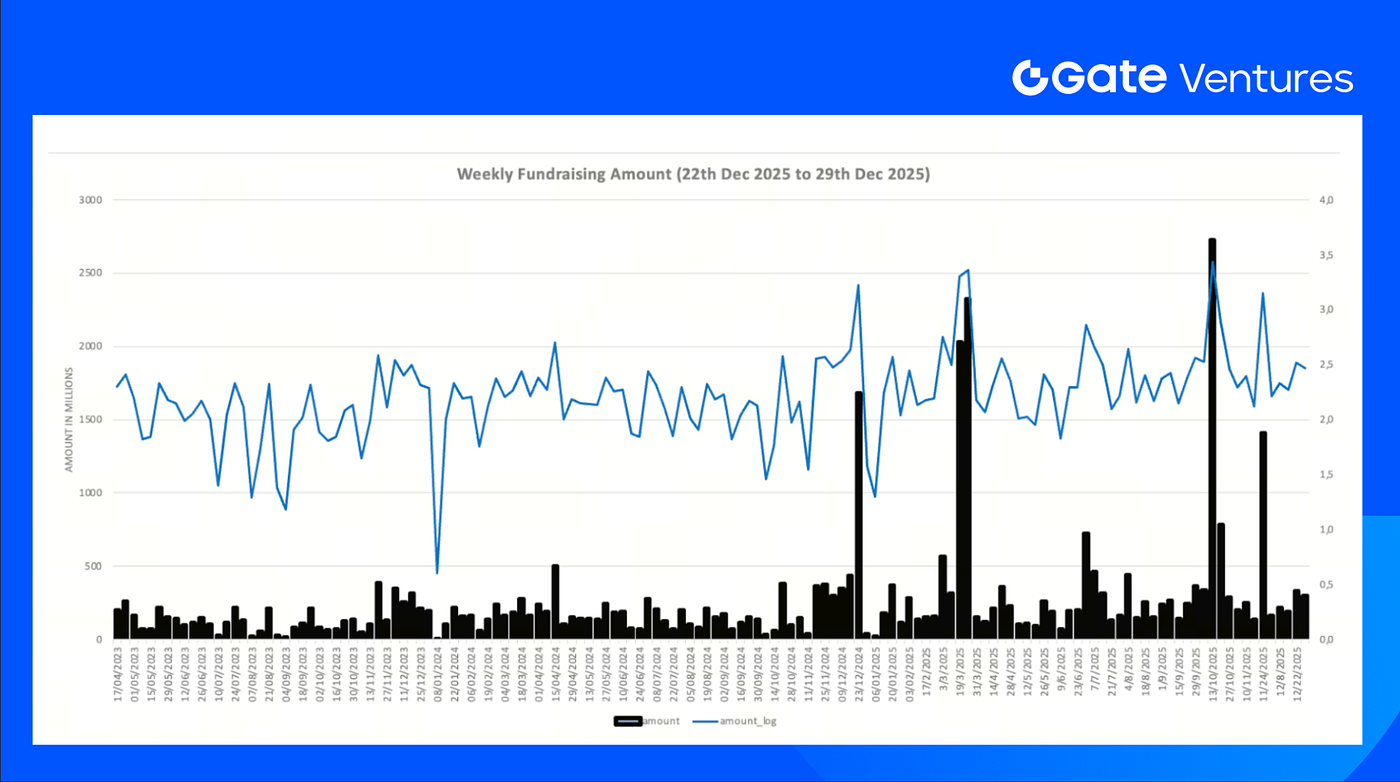

Total weekly fundraising fell to $296M for the 4th week of Dec-2025, a decrease of -10% compared to the week prior. Weekly fundraising in the previous week was down 87% year over year for the same period.

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas and capabilities needed to redefine social and financial interactions.

Website | Twitter | Medium | LinkedIn

The content herein does not constitute any offer, solicitation, or recommendation. You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

Reference:

- https://www.dallasfed.org/research/surveys/des

- https://tradingeconomics.com/united-states/non-farm-payrolls

- https://www.bls.gov/news.release/cpi.nr0.htm

- BTC & ETH ETF Inflow: https://sosovalue.com/tc/assets/etf/us-btc-spot

- BTC Greed and Fear Index: https://alternative.me/crypto/fear-and-greed-index/

- DTCC Tokenization Annoucement: https://coinmarketcap.com/community/articles/694d8788455c6a69d3e4b8ac/

- Telegram Gifts: https://coinmarketcap.com/community/articles/694af4b142d627398ac71c4d/

- WLFI USD1 plan: https://coinmarketcap.com/community/articles/6951b69fbe5b21403bbc7ea9/

- Tether-linked firms buy Northern Data’s mining business for up to $200M:https://cointelegraph.com/news/tether-backed-northern-data-sold-mining-business-to-firms-owned-by-tether-execs-ft

- Coinbase strengthens regulated prediction markets with strategic The Clearing Company acquisition:https://www.theblock.co/post/383497/coinbase-to-acquire-prediction-markets-startup-the-clearing-company

- DWF Labs settles first physical gold trade as crypto capital moves into commodities:https://cointelegraph.com/news/dwf-labs-first-physical-gold-trade-commodities

- Coinbax raises $4.2M Seed amid growing demand for compliant stablecoin rails and programmable payment layer:https://www.globenewswire.com/news-release/2025/12/22/3209148/0/en/Coinbax-Raises-4-2M-to-Bring-Institutional-Controls-to-Stablecoin-Payments.html

- Architect raises $35M Series A to scale institutional perps exchange:https://x.com/Architect_Fi/status/2003484124628254805?s=20

- Rocket lands $1.5M Seed to launch continuous-reward prediction markets:https://x.com/userocket_app/status/2003481579738345924?s=20