The U.S. event-contract market accelerated sharply in 2025, just as a once-in-a-generation catalyst comes into view. Kalshi’s valuation doubled to $11 billion, Polymarket reportedly pursued higher levels, and mass-market platforms including DraftKings, FanDuel, and Robinhood rolled out regulated prediction products ahead of the 2026 FIFA World Cup, set to be hosted in North America. Robinhood estimates event markets already generate $300 million in annual revenue, its fastest-growing business line, signaling that opinion-based trading is moving into the financial mainstream at scale.

That growth, however, is colliding with regulatory reality. As platforms prepare for a World Cup-driven surge in participation, prediction markets are becoming less a product question and more a regulatory design problem. In practice, teams are now building around legal classification, jurisdictional boundaries, and settlement definitions, not simply user demand. Compliance capacity and distribution partnerships increasingly matter as much as liquidity, with the competitive landscape shaped by who can operate at scale inside permitted frameworks rather than who can list the most markets.

Regulatory Cross-Currents

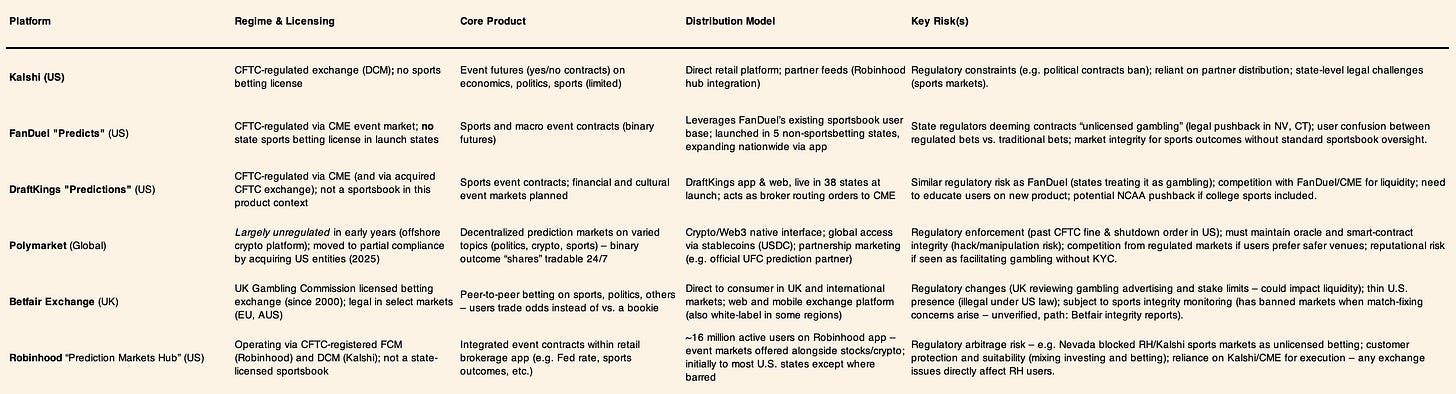

The U.S. Commodity Futures Trading Commission has allowed a narrow class of event contracts tied to economic indicators, while rejecting others as impermissible gaming. In September 2023, the CFTC blocked Kalshi’s attempt to list political futures, though a later court challenge produced a limited approval for presidential election contracts. At the state level, regulators have taken a harder line on sports-adjacent markets. In December 2025, Connecticut’s gaming authority issued cease-and-desist orders against Kalshi, Robinhood, and Crypto.com for offering sports event contracts deemed unlicensed gambling. Nevada separately sought court action to halt similar products, forcing withdrawals in that state.

In response, incumbents such as FanDuel and DraftKings restricted their prediction offerings to jurisdictions without legal sportsbooks, underscoring how distribution is being shaped by regulatory perimeter rather than user demand. The core implication is now clear: regulatory tolerance, not product innovation, determines scale. Contract design, settlement terms, marketing language, and geographic rollout are increasingly engineered to survive classification scrutiny, and platforms that can operate inside accepted regulatory frameworks gain a durable advantage. In this market, regulatory clarity functions as a moat, while ambiguity acts as a direct constraint on growth.

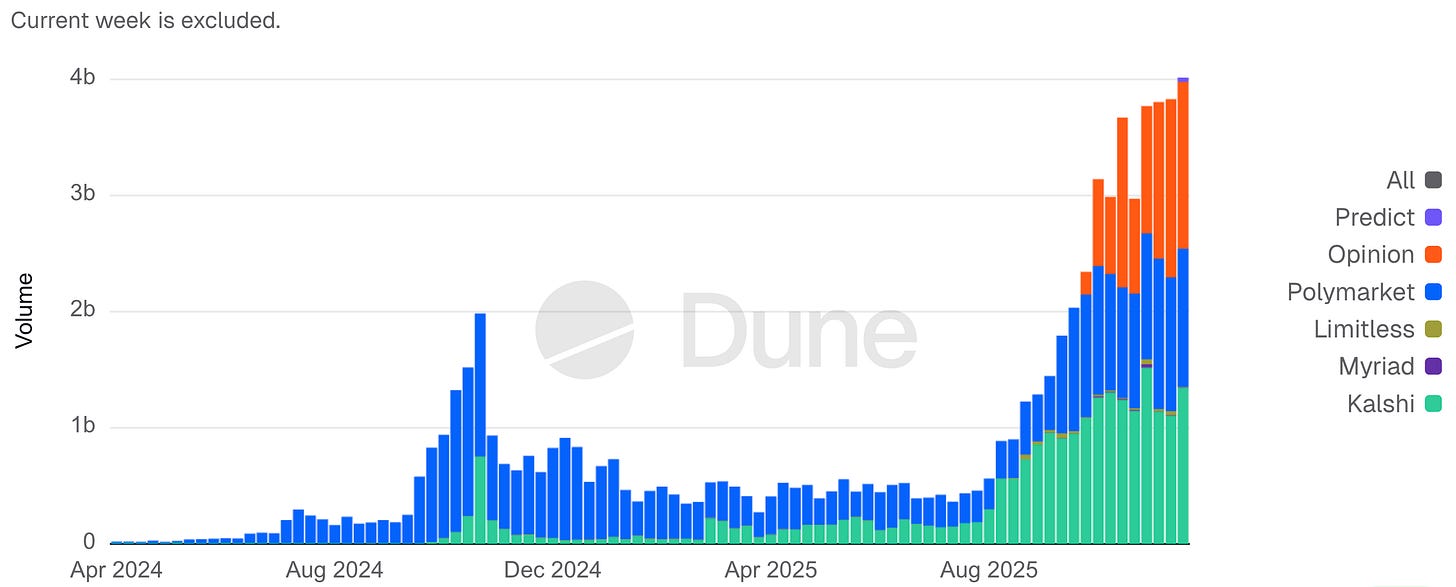

Weekly Prediction Market Notional Volume

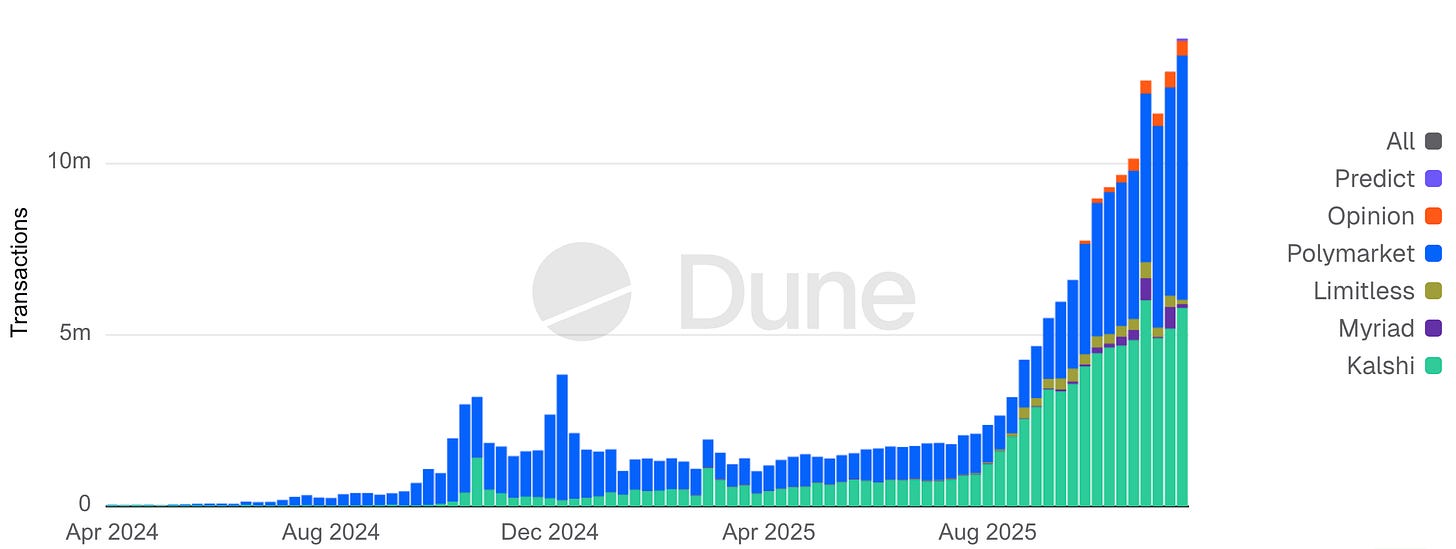

Weekly Prediction Market Transactions

Global Comparables

Outside the U.S., established betting exchanges and newer licensing regimes show that liquid event markets can exist under gambling supervision, but with constrained economics and product scope. The UK’s Betfair Exchange demonstrates that depth is achievable under a betting license, though profitability remains limited by strict consumer protection rules. In Asia, wagering is largely channeled through state monopolies or offshore venues, reflecting strong underlying demand but also persistent enforcement and integrity challenges. Latin America is moving toward formalization, with Brazil opening a regulated betting market in January 2025 to convert a long standing gray market into taxed, supervised activity.

The broader pattern is consistent across regions: regulators are closing loopholes. Sweepstakes and social casino models that relied on free tokens and prize mechanics are being restricted or banned across multiple jurisdictions, raising the compliance bar for any product operating near the gambling boundary. Globally, the direction of travel is toward tighter supervision, not permissive gray zones.

On-Chain Platforms vs. Compliance

Decentralized prediction markets boomed by offering faster, global access at the expense of regulatory compliance. Polymarket, a crypto-based platform, was fined $1.4 million by the CFTC in Jan 2022 for unregistered event swaps and forced to geofence U.S. users. Since then Polymarket pivoted: it beefed up controls (bringing on ex-CFTC advisors) and acquired a registered entity in 2025, allowing a beta re-launch in the U.S. by Nov 2025. Polymarket’s volumes have skyrocketed, reportedly $3.6 billion wagered on a single 2024 election question, with monthly volume hitting $2.6 billion by late 2024, and it attracted blue-chip investors at a ~$12 billion valuation in 2025.

These on-chain platforms deliver rapid market creation and resolution via oracles, but they struggle with speed vs. integrity trade-offs. For instance, governance and oracle disputes can delay outcomes, and anonymity invites questions about market manipulation or insider trading. Regulators also remain wary: even if the code is decentralized, organizers and liquidity providers may be within reach of enforcement (as Polymarket’s case showed). The on-chain sector’s challenge for 2026 is marrying its innovation (24/7 global markets, instant settlement in crypto) with enough compliance to satisfy authorities, without forfeiting the open access that made it popular.

User Behavior & Volume Trends

Prediction market usage surged in 2025 across both sports and non sports events. Industry estimates suggest total notional volume expanded more than tenfold from 2024 levels, reaching roughly $13 billion per month by late 2025. Sports markets functioned as the primary volume engine, with frequent events driving continuous small trades, while politics and macro markets acted as capital magnets, attracting fewer but materially larger positions.

The distinction is visible in market structure. On Kalshi, sports contracts generated the majority of cumulative volume, reflecting repeated participation by recreational users. At the same time, open interest skewed toward politics and economics, indicating larger capital commitments per position. On Polymarket, political markets similarly dominated open interest despite lower trade frequency. In effect, sports maximize turnover, while non sports markets concentrate risk.

This has produced two distinct participant archetypes. Sports users behave as flow traders, placing many small wagers tied to entertainment and habit. Political and macro users behave more like capital allocators, placing fewer but larger trades where perceived informational edge, hedging value, or narrative impact is higher. Platforms therefore face a dual optimization problem: sustaining engagement from flow while maintaining credibility and integrity for capital driven markets.

That split also explains where integrity risks concentrate. In 2025, controversy emerged primarily around non sports listings, including objections from U.S. college sports regulators to markets tied to student athlete decisions. Platforms moved quickly to withdraw those contracts, underscoring that governance risk scales with capital concentration and informational sensitivity rather than raw volume. The implication is that long term growth depends less on expanding sports flow and more on proving that high impact, non sports markets can operate credibly without drifting into regulatory or reputational failure.

2026 World Cup as a System Stress Test

The FIFA World Cup 2026, co-hosted by the United States, Canada, and Mexico, should be analyzed as a full-stack stress test for event-driven trading and regulated wagering infrastructure, analogous to how prior U.S. mega-events exposed system bottlenecks under scale. In 1994, the U.S.-hosted World Cup primarily stressed physical and venue operations across nine cities while setting tournament attendance records of 3,587,538 total spectators and an average of 68,991 per match. By 1996, the Atlanta Olympics shifted the critical path toward communications, information distribution, and incident response.

IBM’s “Info ’96” system centralized timing and scoring and distributed results to officials, media, and public channels, while telecom providers expanded cellular capacity and Motorola deployed large-scale two-way radio networks supporting security, transport, and event coordination. The Centennial Olympic Park bombing on July 27, 1996 demonstrated how quickly large-scale systems pivot from throughput optimization to integrity, resilience, and coordinated response under stress.

In operational terms, Atlanta also marked an inflection point for digital information delivery: official Olympic internet platforms reportedly handled on the order of hundreds of millions of page views and millions of users in 1996, before scaling to billions of interactions and hundreds of millions of users in subsequent Games as digital distribution became a core dependency rather than a supplement.

In 2026, the stress point moves decisively into the coupled digital and financial layer. The tournament expands to 48 teams and 104 matches across 16 host cities, compressing repeated surges of attention and transaction flow into narrow windows over roughly five weeks. During the 2022 World Cup, global betting turnover was widely estimated in the tens of billions of dollars, with peak match windows producing extreme short-term liquidity and settlement loads.

The 2026 edition places a larger share of this activity inside regulated North American rails, as sports betting is legal in 38 U.S. states plus Washington, DC and Puerto Rico in some form, increasing the likelihood that flows route through KYC, payments, and monitoring systems rather than remaining offshore. This coupling is further tightened by app-centric distribution, where live broadcasts, real-time odds or event contracts, funding, and withdrawals increasingly occur within a single mobile session. For event-contract and prediction market venues, the operational stress points are concrete and observable: liquidity concentration and volatility during match windows, settlement integrity including data latency and dispute resolution, jurisdictional product design across federal and state boundaries, and the scalability of KYC, AML, responsible-gaming, and withdrawals under peak demand.

The same regulatory and technical stack will face another large-scale test during the Los Angeles 2028 Olympics, making the 2026 World Cup a filtering event that is likely to drive regulatory intervention, platform consolidation, or market exits, separating infrastructures built for episodic scale from those capable of sustained, compliant mass-market event trading.

Payments & Settlement Innovation

The convergence thesis extends into payments, where stablecoins are increasingly used as operational infrastructure rather than speculative assets. Most crypto native prediction markets rely on USD stablecoins for funding and settlement, and regulated platforms are now testing similar rails. In December 2025, Visa launched a U.S. pilot enabling banks to settle transactions 24/7 using Circle’s USDC on chain, following earlier cross border stablecoin experiments begun in 2023. In event driven markets, stablecoins offer clear operational advantages where permitted: instant deposits and withdrawals, global reach without currency conversion, and settlement that aligns with continuous trading hours.

In practice, stablecoins function primarily as settlement middleware. Users treat them as a faster mechanism to move value in and out of platforms, while operators benefit from lower payment failure rates, improved liquidity management, and near instant settlement. As a result, stablecoin policy debates carry second order implications for prediction markets. Restrictions on stablecoin rails increase friction and slow withdrawals, while regulatory clarity enables deeper integration by mainstream betting and brokerage platforms.

This trajectory faces policy resistance. Christine Lagarde warned in 2025 that private stablecoins pose risks to monetary stability and reiterated support for a state backed digital euro. The European Central Bank’s November 2025 Financial Stability Review similarly cautioned that expanded stablecoin use in payments could undermine bank funding and complicate policy transmission. The most likely 2026 outcome is incremental integration: more sportsbooks accepting stablecoin deposits and payment processors bridging cards to crypto, alongside tighter safeguards such as licensing, reserve audits, and disclosure requirements rather than wholesale endorsement of crypto native payment rails.

Macro Liquidity Backdrop

A skeptical lens is essential when evaluating the 2025 boom: easy money can inflate speculative markets. The Federal Reserve’s late-2025 shift toward ending quantitative tightening may modestly improve liquidity conditions into 2026, which matters insofar as it affects risk appetite rather than direction of adoption. For prediction markets, liquidity influences participation intensity, more cash can translate into higher trading volumes, while tighter conditions can dampen speculative activity at the margin.

That said, 2025 volume growth occurred during a period of elevated rates, suggesting prediction markets are not primarily a liquidity-driven phenomenon. The more useful framing is to treat macro liquidity as an accelerator, not a driver. Baseline adoption is better explained by secular factors: mainstream distribution through brokerages and sportsbooks, product simplification, and growing cultural acceptance of event-based trading. Monetary conditions affect amplitude, how aggressively users deploy capital, but do not determine whether adoption occurs.

This distinction matters for platform strategy. Tighter liquidity could compress volumes without invalidating the convergence thesis, while easier liquidity could amplify engagement and accelerate consolidation in favor of platforms with regulatory clearance, distribution, and settlement control. Macro shocks may still shape short-term behavior, particularly around event contracts tied to economic releases, but they function as volatility inputs rather than structural determinants. In short, liquidity conditions frame outcomes, they do not define them.

“Missing Element” – Super-App Distribution & Moats

Despite the excitement, one element remains unresolved: who will control the user interface of converged trading-betting products? The emerging consensus is that distribution is king, the true moat lies in owning the customer relationship in a “super-app” style ecosystem. This is driving frenetic partnering: exchanges want millions of retail users (hence CME’s deals with FanDuel and DraftKings), and consumer platforms want differentiated content (hence Robinhood’s tie-up with Kalshi and DraftKings’ acquisition of a small CFTC exchange). The model mirrors a brokerage or super-app: offer stocks, options, crypto, and event contracts side-by-side, so users never leave your platform.

Prediction markets are unusually sensitive to liquidity and trust because user value depends on confidence that markets will clear and settle reliably. Thin markets fail quickly; liquid markets compound. Platforms that can acquire users through existing brokerage or sportsbook relationships, with low marginal acquisition cost and pre-existing KYC and funding rails, start with structural advantages over standalone venues that must build liquidity one market at a time. In this sense, prediction markets behave less like social networks and more like options trading: novelty is not the differentiator, depth and reliability are. This is one reason the “feature vs product” debate is increasingly being decided by distribution rather than technology.

Robinhood’s early success supports this thesis, it rolled out event trading to a subset of active traders in 2025 and reportedly saw rapid uptake, with ARK Invest estimating $300 million in recurring revenue by year-end. Moat framework: A standalone prediction market (no matter how innovative) may struggle to compete with entrenched players leveraging their existing user bases. FanDuel’s sportsbook has 12+ million users (for example), and by integrating CME-powered event contracts, it instantly seeded the new platform with liquidity and trust in five states. DraftKings did similarly across 38 states. In contrast, Kalshi and Polymarket spent years building liquidity from scratch; now they increasingly seek distribution partnerships (Robinhood, Underdog Fantasy, even UFC for Polymarket).

The likely outcome is a few large aggregator platforms attaining network effects and regulatory blessings, while smaller venues either specialize (e.g. focus solely on crypto events) or get subsumed.

There is also a super-app convergence with fintech and media: one can envision a not-so-distant future where an app like PayPal or CashApp offers prediction markets alongside payments and stock trading. Major tech and media companies are eyeing this space for engagement: e.g. Apple, Amazon, and ESPN have all explored sports betting partnerships or features in 2023–25, which could evolve into broader event trading offerings within their ecosystems. The “missing element” may be when a tech giant fully integrates prediction markets into a super-app, combining social news, betting, and investing in one place, a potentially dominant moat that few standalone operators could match.

Until then, the race is on between exchanges, sportsbooks, and brokerages to lock in users. Key strategic question for 2026: Will prediction markets become a feature inside larger financial apps, or remain a distinct vertical? Early evidence points to integration: those with the widest distribution (millions of accounts and a trusted brand) hold the high ground.

Regulators, however, may view super-apps that encourage seamless switching between investing and gambling with a critical eye, worried about consumer protection and blurred lines. The ultimate winners will be those who convince both users and regulators that they can safely mainstream this convergence, building a moat not just of technology and liquidity, but of compliance, trust, and user experience.

Opinion Trade (Opinion Labs): Macro-Native On-Chain Challenger

Opinion Trade (by Opinion Labs) positions itself as a macro-first, on-chain prediction venue, with markets that resemble rates and commodities dashboards rather than entertainment-led event betting. The platform launched on BNB Chain on October 24, 2025 and by November 17, 2025 had surpassed $3.1 billion in cumulative notional volume, averaging roughly $132.5 million in daily notional volume in its early weeks. During the period from November 11 to 17, it reportedly led major prediction venues with approximately $1.5 billion in weekly notional volume, while open interest reached $60.9 million as of November 17, placing it behind Kalshi and Polymarket at that point in time.

On the infrastructure side, Opinion Labs announced a December 2025 partnership with Brevis to integrate zero-knowledge-based verification into settlement workflows, with the stated goal of reducing trust gaps in market resolution. The company also disclosed a $5 million seed round led by YZi Labs, formerly Binance Labs, alongside additional participants, providing both capital and strategic adjacency to the BNB ecosystem. Finally, the platform’s explicit geofencing of the United States and other restricted jurisdictions underscores a defining 2025–26 tradeoff for on-chain prediction markets: rapid global liquidity formation constrained by regulatory perimeter design.

Consumer Prediction Markets as an ICO 2.0 Distribution Channel

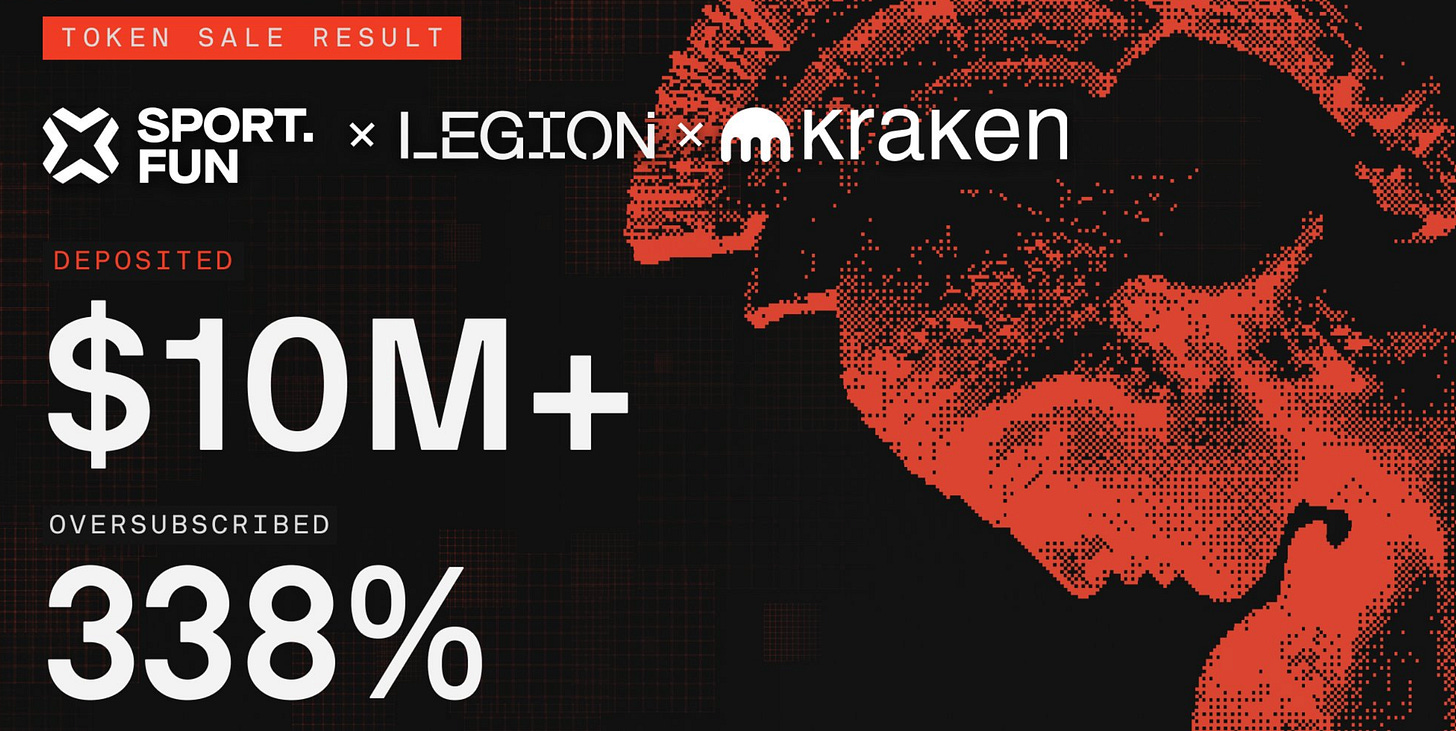

Sport.Fun, formerly Football.Fun, provides a concrete example of how consumer prediction markets are being used as a new generation of token distribution infrastructure, an emergent “ICO 2.0” model embedded directly into live, revenue-generating consumer applications. Launched in August 2025 on Base, the platform initially focused on football fantasy-style event trading before expanding into NFL markets. By late 2025, Sport.Fun reported more than $90 million in cumulative trading volume and over $10 million in platform revenue, indicating meaningful product-market fit prior to any public token issuance.

The company raised a $2 million seed round led by 6th Man Ventures, with participation from Zee Prime Capital, Sfermion, Devmons. The investor mix reflected a growing appetite for consumer-facing crypto applications that blend financial primitives with entertainment-style engagement, rather than infrastructure-only theses. Importantly, capital was deployed after demonstrable user activity and monetization, reversing the sequencing of earlier ICO cycles where token sales preceded real usage.

Sport.Fun’s public token sale for $FUN, conducted between December 16 and 18, 2025, further illustrates this shift. The sale was executed through Kraken Launch alongside the merit-based Legion distribution path, attracting more than 4,600 participants and over $10 million in aggregate pledges. Average participation size was approximately $2,200 per wallet, and demand exceeded the $3 million soft cap by roughly 330 percent. The final raise totaled $4.5 million at a $0.06 token price, implying a fully diluted valuation of $60 million, with 75 million tokens sold following a greenshoe expansion.

Token economics were structured to balance liquidity with post-launch stability. Fifty percent of tokens unlock at the January 2026 token generation event, with the remainder vesting linearly over six months. This design contrasts with the immediate full unlocks common in earlier ICO cycles and reflects lessons learned from prior volatility-driven collapses. The token sale functioned less as a speculative financing event and more as an extension of an existing consumer market, effectively allowing users to invest in the platform they were already actively trading on.

Conclusion

By late 2025, prediction markets had moved from fringe experimentation to a credible mass market category, driven by mainstream distribution, simplified products, and clear user demand. The constraint is no longer adoption, but design under regulation, where classification, settlement integrity, and jurisdictional compliance determine who can scale. The 2026 World Cup should be read not as a growth story, but as a stress test for liquidity, operations, and regulatory resilience under peak load. Platforms that pass this test without enforcement action or reputational damage will define the next phase of consolidation. Those that do not will accelerate the shift toward tighter standards and fewer, larger winners.

Sources:

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.

Disclaimer:

- This article is reprinted from [insights4.vc]. All copyrights belong to the original author [insights4.vc]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.