Mega Bank claims cross-border remittances over $7,000 USD, sparking debate over why banks are cheaper than stablecoins. Besides blockchain experts sarcastically calling this a “Nobel Prize-level argument,” financial researcher Yu Zhe’an also points out flaws. What kind of evaluation standards and cognitive blind spots are hidden behind this?

Mega Bank’s Real-World Test of Stablecoin vs. Traditional Bank Cross-Border Remittance

Mega Bank Chairman Dong Ruibin recently announced the results of a real-world test of stablecoin cross-border remittance, where $50 USD worth of USDT was transferred from an exchange to a Taiwanese exchange, to compare with bank remittance costs.

The test showed that for small amounts, stablecoins have speed and some cost advantages. When remittances exceed $7,000 USD (about NT$200,000), bank remittance overall costs are lower. Therefore, Dong believes that traditional financial systems still hold advantages in fund clearing and compliance.

- Details of Mega Bank’s stablecoin cross-border remittance test here

Blockchain Experts’ Criticism: Mega Bank’s Conclusion Is Like a Nobel-Level Claim

Taiwan’s crypto media “Blockchain” author Xu Ming’en first praised Dong Ruibin’s personal test as commendable, but regarding the conclusion about large remittance costs, he comments that claiming bank remittance over $7,000 USD is more cost-effective than stablecoins is already a Nobel-level innovation.

“If Professor Dong is correct, the whole world should reflect deeply on why no one has personally tested this like him,” he added, “Are you doubting that Professor Dong, who holds the ‘Triple Crown’ in finance, doesn’t understand cross-border remittance?”

Xu Ming’en expressed confusion over why Mega Bank’s leadership would deceive him, because the transfer costs of USDT on blockchain are objective data accessible to everyone.

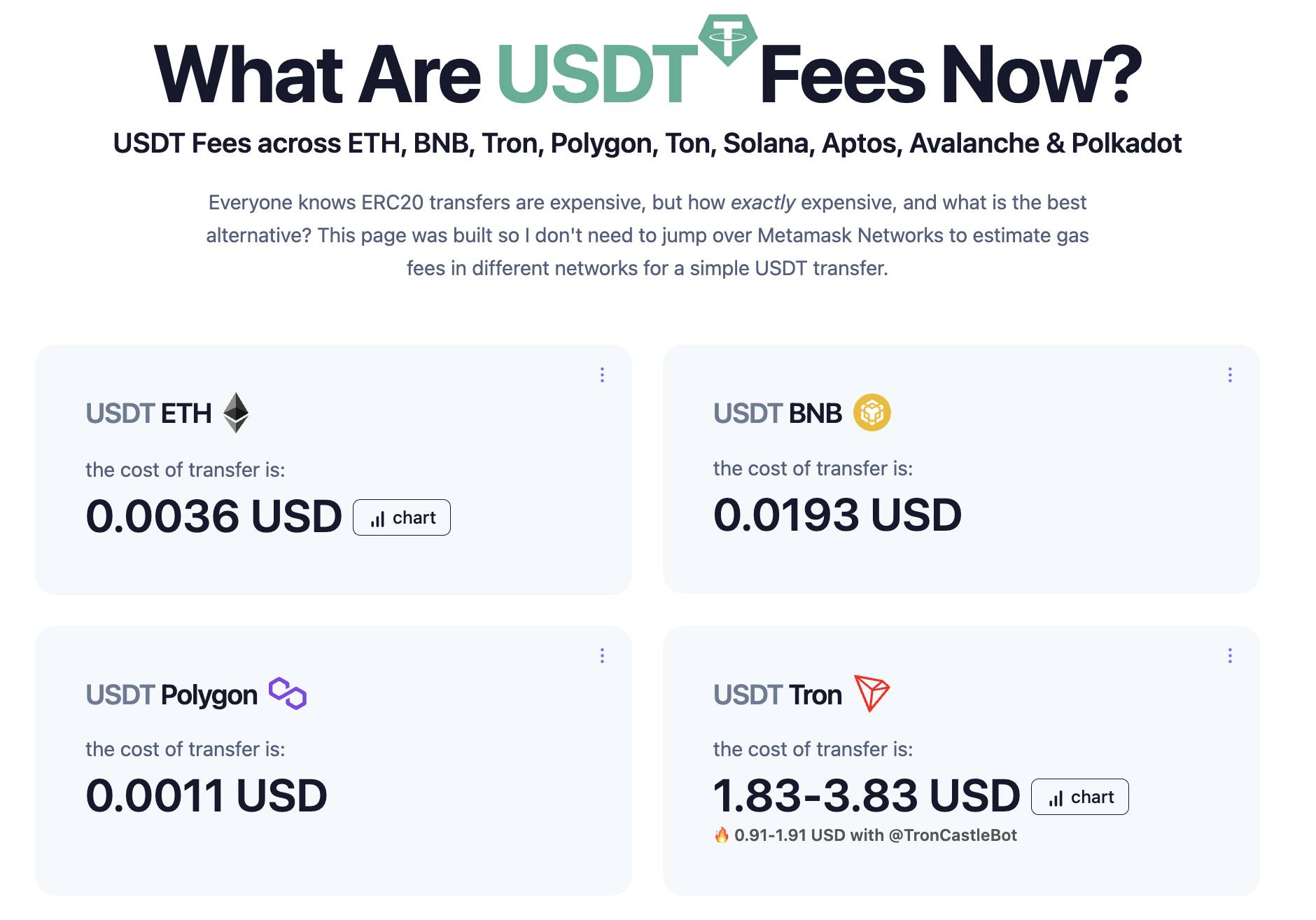

According to the images Xu provided, the transfer fees for USDT on various blockchains are extremely low: as of the afternoon of March 11, Ethereum at $0.0036, Binance Smart Chain at $0.0193, Polygon at $0.0011, and Tron between $1.83 and $3.83.

Image source: Blockchain Facebook

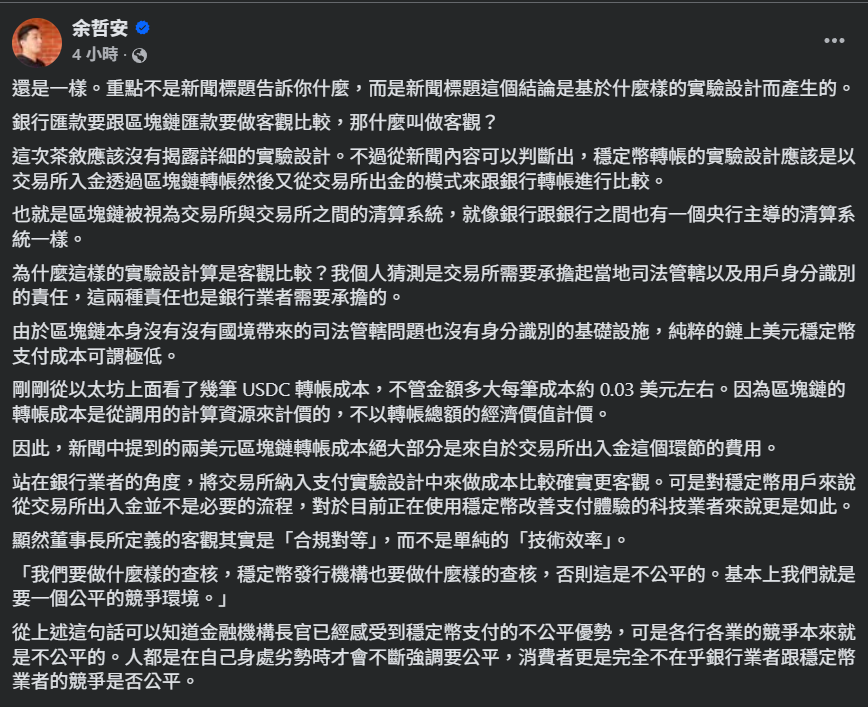

Yu Zhe’an Analyzes Experimental Design and Fairness

Financial researcher Yu Zhe’an analyzed in a post that the focus of this test should not be on the news headline, but on what kind of experimental design led to this conclusion. It’s clear that the chairman’s definition of objectivity is actually “regulatory fairness,” not just “technical efficiency.”

He pointed out that Mega Bank’s stablecoin transfer experiment involved depositing into an exchange, transferring via blockchain, then withdrawing from the exchange, to compare with bank transfers.

Including exchanges in the cost comparison is relatively objective for banks, as both must handle jurisdictional and user identity verification responsibilities. But for stablecoin users, depositing and withdrawing from exchanges is unnecessary, especially for tech companies using stablecoins to improve payment experiences.

Yu Zhe’an summarized: “People only emphasize fairness when they are at a disadvantage, but consumers don’t care whether the competition between banks and stablecoin providers is fair at all.”

Image source: Yu Zhe’an Facebook

In response to comments, he further inferred, “If I worked at a bank, and my superior asked me to research stablecoin payments and find the bank’s advantages, I would naturally design the experiment this way.”

Crypto City Editor: Ignoring Technological Development Risks Missing Transformation Opportunities

Max, editor of “Crypto City,” believes that Mega Bank’s test results actually reflect differences in experimental design and comparison standards.

First, regarding cost comparison, the test used a centralized exchange withdrawal fee of about $2 as the stablecoin cost, but the real advantage of blockchain is the on-chain transfer itself. Most public chains have actual transfer fees below $0.50, some even negligible. Using exchange service fees to represent on-chain costs can mislead outsiders about the technical efficiency of stablecoins.

He also pointed out that bank cross-border remittance costs are not just about the apparent service fee; exchange rate spreads and intermediary bank fees are often the main expenses. In contrast, stablecoins like USDT and USDC are closer to market rates, with more transparent transaction paths.

Additionally, bank tests are usually based on optimized internal channels, while blockchain tests often assume higher-cost Layer 1 networks, ignoring low-cost, high-speed solutions like Solana or Layer 2.

However, Max also understands the industry strategy. Cross-border remittance has long been a major revenue source for banks. Facing potential stablecoin competition, banks naturally emphasize their advantages and demonstrate their digital capabilities to regulators.

Max concludes that while banks still hold irreplaceable advantages in compliance and trust mechanisms, ignoring stablecoin technological development could cause the financial system to miss real transformation opportunities.

Further Reading:

Mega Bank Chairman: EasyCard Is Taiwan’s Stablecoin! Discussing the Impact of the Tingen Act on Taiwan

Is EasyCard a stablecoin? Mega Bank CEO’s remarks spark controversy—what do five media figures and experts think?

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.