Amid continued pressure on Bitcoin prices, with a year-to-date decline exceeding 30%, Strategy’s increased holdings and yield data reveal noteworthy signals. This publicly listed company, holding about 4% of the world's Bitcoin, operates with a model different from traditional corporate finance—focusing not on valuation driven by core business growth, but on building enterprise value through continuous Bitcoin allocation and capital structure optimization. Analyzing Strategy’s increased holdings, the implications of BTC yield metrics, the evolution of corporate Bitcoin reserve models, and differences from traditional asset management reveals the deeper logic behind this strategy.

Logic of Increasing Holdings: Why Strategy Continues to Add Bitcoin

Strategy’s Bitcoin accumulation isn’t an isolated decision but based on a comprehensive asset allocation philosophy. Phong Le explicitly expressed the company's long-term view on Bitcoin when disclosing data: limited supply, increasing institutional demand, and digital assets entering mainstream finance. These three factors underpin Strategy’s view of BTC as a long-term store of value.

From the supply side, Bitcoin’s total cap is fixed at 21 million coins. As of July 2026, over 19.7 million have been mined, with less than 1.3 million remaining, and daily new supply continues to decline. This supply rigidity is one of the core reasons Strategy dares to concentrate billions of dollars in a single digital asset.

From the demand side, the institutional allocation landscape is changing structurally in 2026. According to Bernstein, in 2025, incremental Bitcoin funds mainly came from ETFs and corporate treasuries, but by 2026, the structure has shifted—although ETF net inflows have totaled about $2.6 billion outflows this year, corporate treasury buying has offset this. This indicates corporate demand for Bitcoin is becoming a key driver, replacing ETF outflows. Strategy Chairman Michael Saylor previously pointed out that institutional capital inflows—including ETF flows, corporate treasury accumulation, and sovereign reserves—are replacing retail-driven cycles and are the main adoption drivers.

Operationally, Strategy’s accumulation pattern involves a mature capital operation chain: raising funds via stock issuance, convertible bonds, preferred shares, etc., then using the proceeds to buy Bitcoin, expanding corporate digital assets, and boosting market valuation. In the first five months of 2026, Strategy raised about $7.5 billion through preferred stock issuance. This model enables Strategy not just to hold Bitcoin but to build a capital operation system around BTC—using Bitcoin as a core asset, leveraging capital market tools to expand holdings, and then using the increased holdings to boost market valuation.

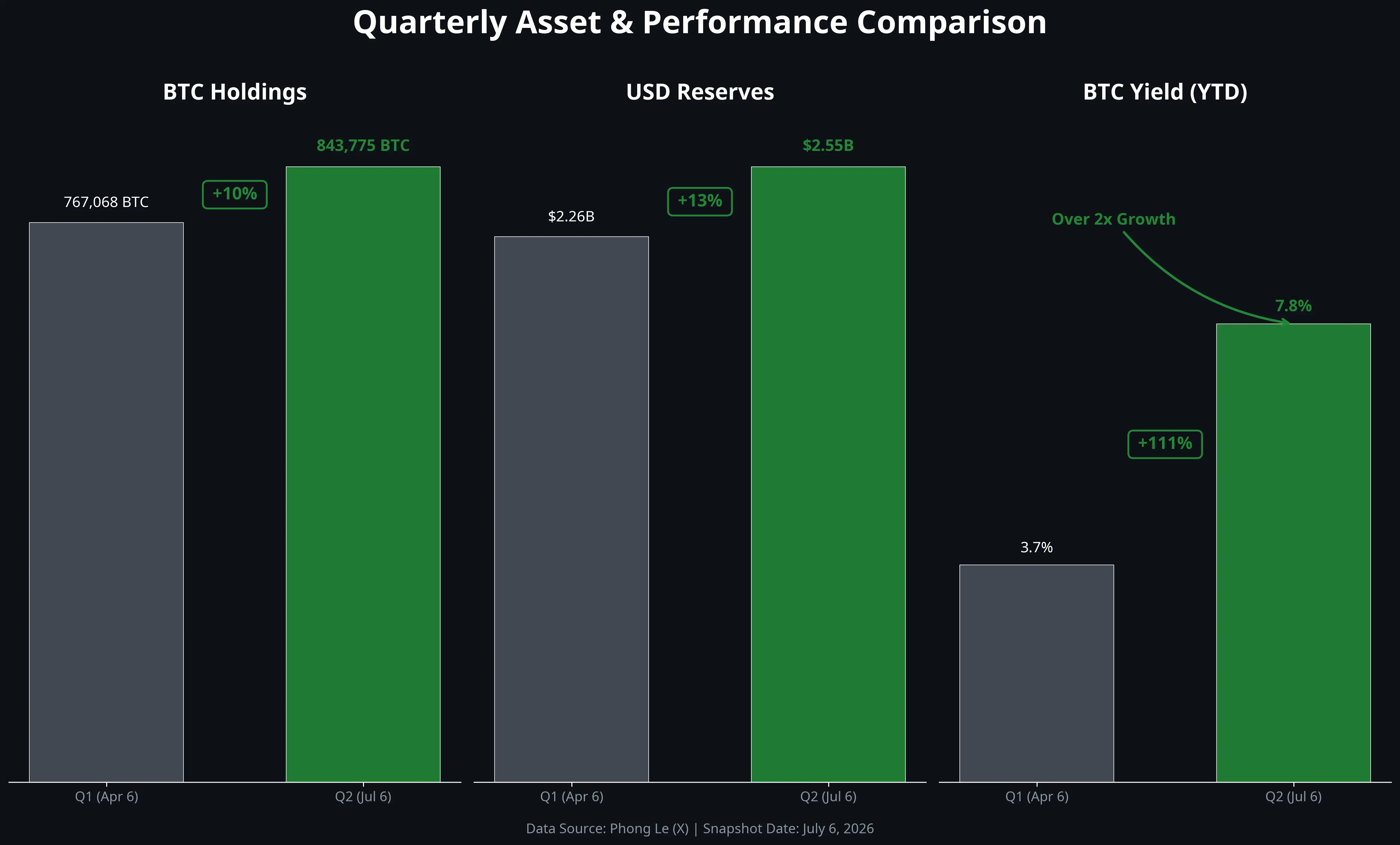

Notably, on July 6, 2026, Strategy sold 3,588 BTC (about $21.6 million) to pay dividends on preferred stock (STRC). This was the first large-scale Bitcoin sale in five years. However, this sale only accounts for about 0.4% of its total holdings and is more about liquidity management than a strategic shift. The company still holds $2.55 billion in cash reserves, enough to cover about 17 months of interest and preferred dividend payments. This operation indicates that Strategy’s Bitcoin strategy has entered a more refined stage—beyond just accumulation, integrating Bitcoin into a dynamic asset-liability management framework.

Strategy 2026 Q2 Key Data Overview

The True Meaning of the Doubling BTC Yield

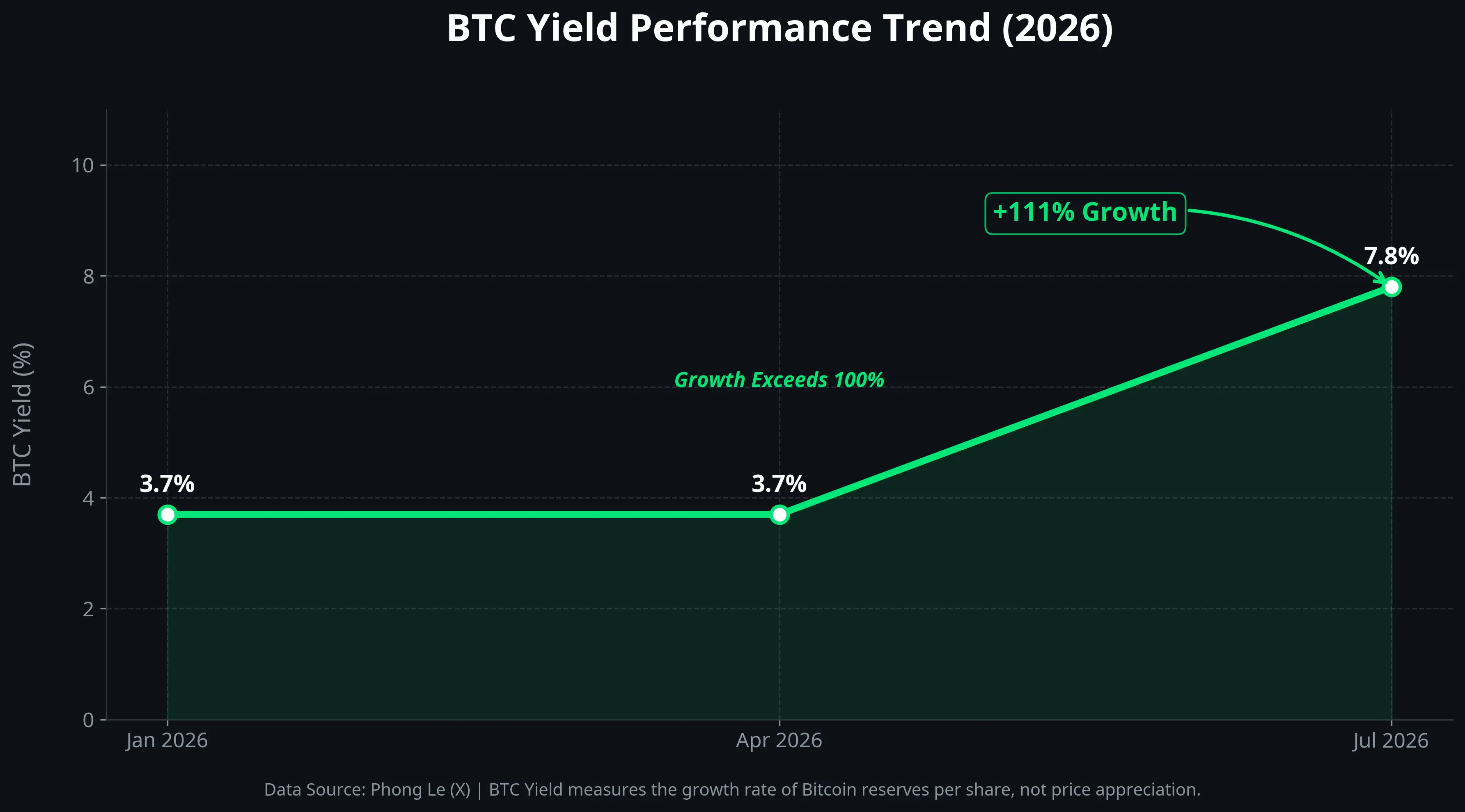

Strategy’s announced “BTC yield” is a key indicator of its strategic effectiveness. This metric has risen from 3.7% at the start of the year to 7.8%, more than doubling.

BTC yield does not refer to capital gains from Bitcoin price appreciation but reflects the growth rate of the company’s Bitcoin holdings relative to its diluted share capital. In simple terms, it measures: under conditions that do not excessively dilute existing shareholders, how much value the company can add per share through capital market operations.

The increase from 3.7% to 7.8% means that in the first half of 2026, Strategy’s financing and capital operations increased the Bitcoin reserve value per share by nearly 8 percentage points. This rise mainly comes from two channels: one, the company raising funds via stock or convertible bond issuance and using the proceeds to buy BTC, increasing total holdings; two, adjusting capital structure to enhance Bitcoin allocation without expanding share count.

However, it’s important to clarify that BTC yield does not represent actual cash profit or operational earnings. It’s essentially a “per-share Bitcoin reserve growth rate,” not a traditional investment return. Strategy’s actual financial performance remains directly affected by Bitcoin market price fluctuations—when Bitcoin prices fall, the company’s book shows unrealized losses. As of July 5, 2026, Strategy’s total position cost is about $63.69 billion, with an average cost of approximately $75,476 per BTC. At the current Gate price of $62,086.7, unrealized losses exceed $11 billion.

Therefore, the doubling of BTC yield more reflects an improvement in capital operation efficiency rather than the portfolio turning profitable. Its true significance is signaling to the market that even during a Bitcoin price downturn, Strategy can continue to expand its relative Bitcoin reserve size through capital market tools.

BTC Yield Curve: From 3.7% to 7.8%

Corporate Bitcoin Reserves: From Experiment to Trend

Is Strategy’s model becoming a new trend in corporate asset management? That’s the key question.

Supporting factors show multiple positive signals in 2026. First, more listed companies are exploring Bitcoin reserves. For example, Nasdaq-listed Empery Digital has accumulated over 1,200 BTC in six days. Japanese firms, due to yen weakness, are incorporating Bitcoin and XRP into their financial reserves, with SBI VC Trade’s registered accounts surpassing 2 million. Second, the launch of Bitcoin ETFs has significantly boosted institutional acceptance, further legitimizing digital assets as an asset class in regulatory and financial spheres. Bernstein maintains its year-end Bitcoin price target at $150,000.

Deeper structural changes show corporate treasury buying becoming an important support for Bitcoin markets. Despite ETF investor net outflows in 2026, corporate treasury buying has filled this gap. This indicates that demand for Bitcoin is shifting from retail and speculative funds toward more stable institutional and corporate allocations.

However, the sustainability of this trend faces multiple constraints:

First, sharp Bitcoin price volatility poses a direct challenge to corporate balance sheets. Strategy’s average cost is about $75,476, while the current market price is $62,086.7, with unrealized losses over $11 billion. For a listed company, such paper losses can exert ongoing pressure on stock prices and investor confidence—Strategy’s stock has fallen about 75% over the past year.

Second, changes in financing costs impact the sustainability of leveraged BTC strategies. Strategy’s preferred stock dividend rate increased by 50 basis points to 12% in July 2026. If financing costs continue to rise, arbitrage opportunities via borrowing or debt issuance to buy BTC will diminish.

Third, asset concentration risk cannot be ignored. Strategy’s value is heavily concentrated in a single asset class—Bitcoin—which is almost unthinkable in traditional corporate finance. If Bitcoin markets face extreme events (regulatory crackdowns, technical vulnerabilities, or broader market crises), the company’s survival could be threatened.

Two Financial Models: Strategy vs. Traditional Corporations

Strategy’s asset management approach fundamentally differs from that of traditional companies, which can be understood through a clear framework.

Traditional firms follow a “defensive” logic: holding cash, short-term government bonds, and high-quality debt to ensure liquidity and hedge against uncertainty. Their value growth mainly depends on revenue and profit expansion—selling products well, gaining market share, improving margins, and thus increasing stock prices. Bitcoin, at most, is a marginal, experimental allocation on the balance sheet, with a tiny proportion.

Strategy’s model is entirely different. Its core asset is Bitcoin, and the main growth driver isn’t software sales or operational income but the market appreciation of Bitcoin assets and the multiplier effect of capital operations. The company raises funds via stock, convertible bonds, preferred shares, converting capital into Bitcoin, and then using Bitcoin reserves’ growth to support higher market valuation. This is a “high volatility, high growth” financial model—more elastic returns but also more concentrated risk.

The fundamental difference between these two models concerns “how companies create value.” Traditional models believe value is created through products and services; Strategy’s approach argues that in a macro environment of fiat currency depreciation, allocating corporate assets into scarce digital assets itself is a form of value creation.

Currently, this model still faces significant controversy. Strategy’s stock price has plummeted, indicating the market has not fully accepted its “Bitcoin treasury company” valuation logic. However, more companies are starting to imitate this path—even if only in small exploratory allocations—suggesting this logic is gaining recognition among certain groups.

Risks and Challenges

Strategy’s replicability faces several structural constraints.

Regulatory uncertainty is the most critical variable. Although the regulatory environment has improved compared to previous years, differences in accounting treatment, tax rules, and disclosure requirements across jurisdictions remain significant. Companies holding Bitcoin as a primary reserve face varying compliance costs.

Accounting treatment is particularly problematic. Under current standards, Bitcoin is classified as “indefinite-lived intangible assets,” with impairments recognized immediately, but recoveries only upon sale. This asymmetric treatment causes companies to record large unrealized losses when prices fall, while gains are only reflected upon sale—distorting perceptions of true financial health.

Liquidity risk is also notable. Strategy holds about 4% of global Bitcoin supply, so any large-scale sale could impact market prices significantly. The sale of 3,588 BTC (about 0.4% of holdings) on July 6 already drew market attention. Larger future liquidations could face market absorption challenges.

Finally, the sustainability of Strategy’s model hinges on a core assumption: that Bitcoin’s long-term price trend is upward. If this holds, current paper losses are temporary; if not, the business model faces fundamental challenges.