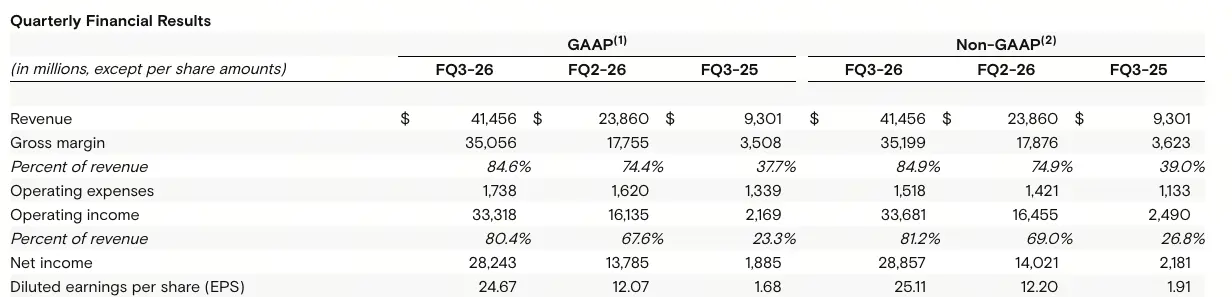

Micron Technology (MU) reported FY2026 Q3 earnings on June 24: revenue reached $41.46 billion, significantly exceeding analyst expectations of $35.84 billion tracked by LSEG; adjusted diluted EPS was $25.11, above the expected $20.78. After the earnings release, Micron's stock rose 15% in after-hours trading.

Micron Q3 Earnings Beat: Detailed Data on Business Segment Gross Margin and Segment Revenue

(Source: Micron website)

(Source: Micron website)

According to Micron's earnings report, the performance of each business segment in FY2026 Q3 is as follows:

Cloud Storage Business: Q3 revenue $13.77 billion (previous quarter $7.75 billion, same period last year $3.39 billion), gross margin 83%, operating margin 78%.

Core Data Center Business: Q3 revenue $11.52 billion (previous quarter $5.69 billion, same period last year $1.53 billion), gross margin 87%, operating margin 83%.

Mobile and Client Business: Q3 revenue $11.52 billion (same period last year $7.71 billion), gross margin 87%, operating margin 86%.

Automotive and Embedded Business: Q3 revenue $4.63 billion (same period last year $2.71 billion), gross margin 79%, operating margin 75%.

On overall cash flow, Q3 operating cash flow reached $25.39 billion, compared to $11.9 billion in the previous quarter and $4.61 billion in the same period last year.

16 Long-Term Agreements: Data Center and Automotive Manufacturers, Three- to Five-Year Purchase Commitments

Micron stated that it has signed 16 long-term agreements (LTAs) with buyers including data center operators and automotive manufacturers, each covering three to five years with binding purchase volumes. CEO Sanjay Mehrotra said that once these agreements are fully in effect, "approximately half or more" of the company's revenue will come from these strategic customer agreements. CFO Mark Murphy explained to analysts: "We have clear visibility into demand, and these contracts guarantee order volumes, giving us confidence to invest."

Mehrotra said the company is currently investing record amounts in technology, products, and supply to meet customer demand, and noted that the quarterly results "reflect the strategic value of memory technology in the AI era."

Q4 FY2026 Guidance: $50 Billion Revenue Target and $31 Adjusted EPS

Micron's Q4 FY2026 guidance is as follows: Revenue $50 billion (±$1 billion); gross margin approximately 86%; GAAP operating expenses approximately $1.86 billion; adjusted operating expenses approximately $1.65 billion; GAAP diluted EPS $30.73 (±$1); adjusted diluted EPS $31.00 (±$1).

In terms of dividends, the board declared a quarterly dividend of $0.15 per share on June 24, 2026, payable on July 21, 2026, to shareholders on the register as of July 6.

FAQ

How does Micron's Q3 gross margin of 84.6% compare historically?

According to the earnings report, Q3 GAAP gross margin of 84.6% significantly increased from 74.4% in the previous quarter and 37.7% in the same period last year. The wide gap between last year's gross margin of less than 38% and this quarter's nearly 85% reflects the significant improvement in pricing power and scale effects driven by AI memory demand.

Do the binding nature of the 16 long-term agreements mean significantly improved revenue visibility?

According to CFO Mark Murphy, these agreements include "binding purchase volumes," allowing Micron to "have clear visibility into demand" and confidence to make capital investments. Mehrotra expects that once the agreements are fully in effect, "approximately half or more" of revenue will come from these strategic customer agreements, which will significantly enhance Micron's revenue visibility.

What growth rate does Micron's Q4 guidance of $50 billion imply?

Based on earnings data, Q3 revenue was $41.46 billion, while Q4 guidance is $50 billion (±$1 billion), representing sequential growth of approximately 20%; Q4 revenue in the same period last year was about $9.3 billion, implying year-over-year growth of approximately 4.4 times. This growth is primarily driven by AI data center memory demand.