We are pleased to announce that ArkStream Capital has made an additional investment of 10 million USD in Ethena in August 2025, reinforcing our long-term strategy following our initial investment of 5 million USD in December 2024. This increase is a strong recognition of Ethena's ability to achieve structured breakthroughs simultaneously in both product and Capital Market.

What we are firmly betting on is not only the explosive growth in data but also the institutional innovation of Ethena in the Capital Market.

The Flywheel of “Coin-Stock Dual Track”

In the past two years, Ethena has not only proven the product PMF of USDe, but is also currently bundling a purely crypto-native decentralized protocol with a US stock-configurable capital vehicle into a “dual-track” flywheel, completing what we call a key leap to Capital-Market Fit (CMF). This is not for short-term arbitrage, but to connect the protocol's cash flow, governance, and external compliant capital into a reusable capital structure.

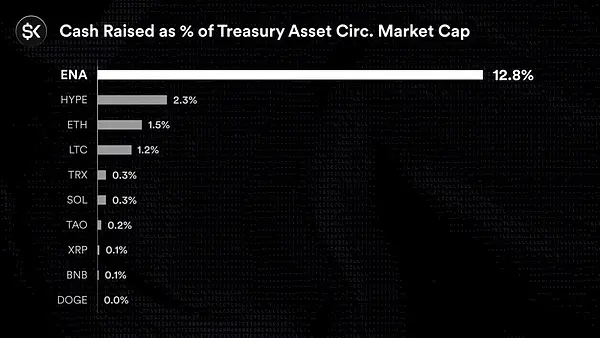

Equity Side (StablecoinX): Based on the merger with TLGY SPAC business, the PIPE scale has been increased from 360 million USD to a total of 895 million USD (latest round an additional 530 million USD), with plans to list on NASDAQ under the ticker “USDE”. After the closing, StablecoinX's balance sheet will hold over 3 billion ENA. This round of funding will be used to purchase locked ENA from a subsidiary of the Ethena Foundation; at the same time, the foundation's subsidiary will commission a third-party market maker to execute approximately 310 million USD in spot repurchases in the open market over the next 6-8 weeks, with the pace as follows: 5 million USD daily when ENA > 0.70 USD; 10 million USD daily when ENA < 0.70 USD or when there is a single-day drop of more than 5%. It is expected to account for a total of 13% of the circulating supply, with the previous first round PIPE having acquired about 7.3%. Additionally, the Ethena Foundation retains veto rights over the sale of StablecoinX. This aligns the demand side of equity financing with the governance assets on-chain, forming an institutional channel of “compliant capital → governance token demand.”

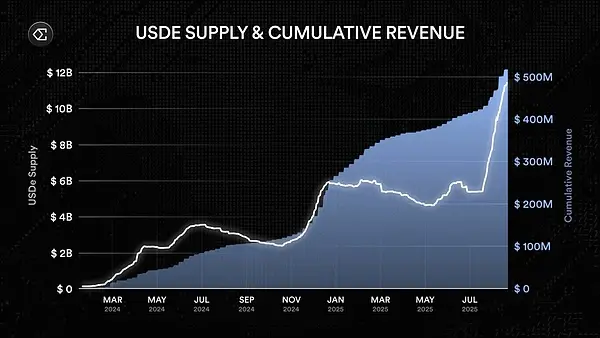

Token Side (ENA): The scale of USDe surged to $12 billion, ranking third among stablecoins, with total historical revenue exceeding $500 million. Aave's risk exposure to USDe-related assets once reached about $4.7 billion; discussions regarding the sENA fee switch are accelerating: the Ethena Risk Committee has established clear activation indicators (USDe circulation, cumulative protocol revenue, CEX coverage). With USDe landing on Binance, the last key condition has also been met, and the protocol is now equipped to initiate the mechanism for distributing part of the revenue to sENA. This means that the token capturing cash flow valve is entering a substantial opening phase, and the value support for ENA will shift from solely relying on growth expectations to directly anchoring the protocol's cash flow.

External Signals (DAT Reserve): Mega Matrix (NYSE: MPU) has announced ENA as the primary strategic reserve for DAT, equivalent to “making long-term purchases” using the listed company's balance sheet. At the same time, Mega Matrix submitted a $2 billion shelf registration to the SEC, reserving space for flexible financing in batches over the coming years. This means that it not only locks in ENA on the asset allocation side but also leaves an upper limit for “continuous accumulation” or related capital operations at the financing tool level, providing external institutional support for the long-term demand side of ENA.

Unlike the “direct shell buy + PIPE + ATM” arbitrage model, this three-point design forms a closed loop:

Equity Financing → ENA Demand/Repurchase → USDe Expansion → Agreement Cash Flow Growth (Support Valuation and Refinancing) → DAT/Institutional Allocation → External Structural Buying Pressure → Flow Back to Both Token and Equity Levels, Ultimately Benefiting Both Token Holders and Shareholders.

This is the first time a DeFi protocol has entered the US stock market through structured financial instruments. Ethena is transforming “protocol growth” into “institutional demand,” allowing for more cross-cycle capital elasticity in capturing the value of ENA, which is also one of the core reasons for our continued heavy investment.

USDe: The New Benchmark Interest Rate for DeFi

USDe is driven by the crypto-native delta-neutral mechanism for returns, gradually being seen by the market as the new benchmark interest rate for DeFi funds and an anchor for “quasi-risk-free assets”:.

- Supply Volume: As of the end of August, it has surpassed 12.5 billion USD, becoming the third largest stablecoin;

- Top Lending Exposure: Aave's risk exposure to Ethena-related assets reaches $4.7 billion, demonstrating its primary liquidity position in the mainstream DeFi credit market.

- Cross-chain Scale: Cumulative transaction volume exceeds 5.7 billion USD;

- Yield Range: By using a delta-neutral strategy, it provides approximately 9–11% annualized returns, regarded as the “risk-free rate” of DeFi.

- Protocol Revenue: Cumulative revenue exceeds 500 million USD, with the highest weekly revenue reaching 13.4 million USD in the week of August 25.

As USDe is more widely used as collateral and settlement assets, the triadic positive feedback of its scale—liquidity—yield will further strengthen the governance and distribution value of ENA (including the value return brought by potential mechanisms such as fee-switch).

The “Post-Strategy” After Stablecoins: Expanding from Yield Dollars to the Dual Wings of Settlement Layer and Capital Layer

Stablecoins are not the destination, but the foundation for cash flow and distribution. Ethena's “backhand” is reflected in the collaborative expansion of distribution and settlement:

Distribution Layer: Allow “Yield USD” to Reach Institutions and One Billion Users

- iUSDe (Institutional Version): By using a transfer-restricted contract structure, the yield characteristics of sUSDe are compliantly packaged to connect with the TradFi distribution network, reducing operational and compliance friction for institutions.

- tsUSDe (Telegram/TON): Deep collaboration with TON integrates sUSDe natively into the Telegram wallet ecosystem, targeting billions of endpoints, making dollar yields an instantly distributable internet-native asset.

Why it matters: The “light compliance + platform-level entry” on the distribution side can amplify the positive feedback of “USDe scale → lending exposure → protocol income”; the related risk position of 4.7 billion dollars on Aave is already validating this backbone.

Settlement Layer: Converge turns USDe into native Gas/settlement assets

Converge Chain: Co-built with Securitize, a modular combination of Arbitrum + Celestia, supports USDe / USDtb as gas and settlement assets, and enhances security with ENA staking, compatible with both permissioned and permissionless applications.

Why it matters: When “yield dollars” become the underlying settlement fuel, the network effect of USDe rises from a financial primitive to a transaction routing/ledger unit; this gives Ethena the opportunity to undertake high value-added services after stablecoin issuance, institutional settlement, and market-making collateral.

Our judgment: This combination of “institutional compliance access + super distribution frontend + dedicated settlement chain” significantly enhances the availability and usability of USDe, and brings continuous cash flow spillover for ENA across scenarios and customer groups.

Risks and Moat: Transparent Mechanism + Decentralized Structure

Our increased holding in Ethena is also based on our examination of its risk governance and mechanism transparency:

- Trading Risk: USDe fundamentally relies on the basis/funding framework of “multiple spot/short perpetuals,” and extreme market conditions may compress returns or cause temporary inversions. Ethena mitigates such risks through multiple exchanges, diversified counterparties, and dynamic hedging parameters.

- Systemic Spillover: As USDe becomes a leading collateral asset, the risk governance of major lending protocols (increasing risk weights, governance parameters) is also following suit.

Investment Logic of ArkStream

From short-term to long-term, Ethena's investment logic is very clear:

- Short-term (Tactical Level): USDe has grown into the largest yield-bearing capital reservoir in DeFi. Its $12.5 billion circulation scale and $4.7 billion risk exposure on Aave have established its status as a “first-class collateral asset” in the DeFi lending market. At the same time, the 9–11% annualized yield of USDe has been regarded by the market as a quasi-“risk-free rate,” becoming the core anchor point for liquidity aggregation. The logic at this stage is: the continuous strengthening of scale and yield makes USDe the financial hub of the entire ecosystem, providing stable accumulation for protocol cash flow.

- Mid-term (Structural Level): Ethena has completed the coupling with traditional markets in its capital structure. Through SPAC → PIPE → De-SPAC, USDe/ENA is integrated into the compliance framework of the US stock market; StablecoinX has established an institutional channel for governance token demand through accumulating $895 million PIPE and 3 billion ENA on its balance sheet; at the same time, Mega Matrix's DAT reserves and $2 billion shelf registration further institutionalize the external capital buying mechanism. The logic of this stage lies in: by using structured financial instruments to lock equity financing and token demand together, linking the valuation of ENA with the traditional capital market.

- Long-term (Paradigm Level): The most critical turning point comes from the official implementation of the sENA fee switch. The three activation indicators set by the Risk Committee (USDe circulation, cumulative revenue, CEX coverage) are now all met, especially after USDe's listing on Binance, completing the final coverage condition. This means that Ethena is now positioned to directly allocate a portion of protocol revenue to sENA. From now on, ENA will shift from a “growth narrative-driven” approach to a “cash flow-driven” model, becoming the first stablecoin governance token capable of directly capturing the real cash flow of the protocol. Combined with the external long-term buying pressure brought by DAT reserves, ENA's value support will present a dual-driven model of “endogenous cash flow distribution + external structured allocation”. We anticipate that within this framework, ENA is likely to evolve into a “quasi-gold reserve” asset for stablecoin governance, achieving a positive cross-cycle circulation of protocol cash flow and the Capital Market.

Conclusion

In ArkStream's view, Ethena is not just a stablecoin protocol, but a bridge between crypto-native yields and traditional Capital Market. When the product sets the correct 'base interest rate' and the capital structure provides an institutional 'gate' aimed at the US stock market, the value capture of ENA possesses cross-cycle extensibility. Our choice to increase investment at this point is a decisive step in supporting Ethena's transition from PMF to CMF.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.