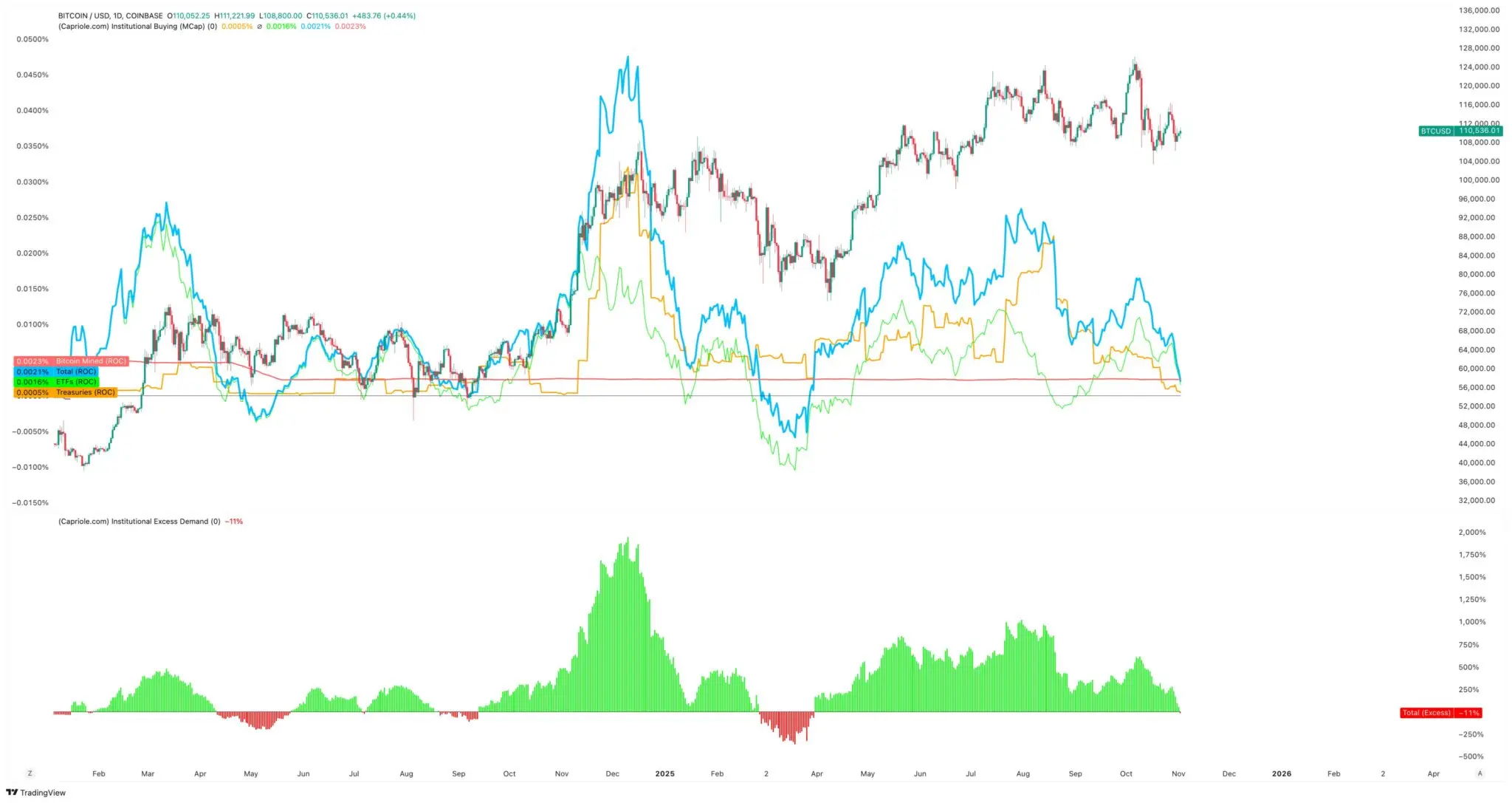

Charles Edwards, founder of Capriole Investments, stated that his optimistic outlook on the market has weakened as the pace of institutional accumulation slows down. He noted that for the first time in seven months, institutional net buying has fallen below the daily mining supply. In the third quarter, the Strategy added only about 43,000 Bitcoins, the lowest quarterly purchase volume of the year.

Strategy Behind the Logic of Going from Frenzied Buying to Stopping

(Source: Capriole Investments)

No company represents corporate Bitcoin trading better than Strategy Inc. This software manufacturer, led by Michael Saylor, has transformed into a Bitcoin vault company and currently holds over 674,000 Bitcoins, solidifying its position as the largest single corporate holder. This holding size accounts for approximately 3.4% of the total Bitcoin supply, far ahead of all publicly traded companies.

However, in the past few months, its purchasing pace has significantly slowed down. As a reference, Strategy increased its holdings by about 43,000 Bitcoins in the third quarter, which is the company's lowest quarterly purchase volume this year. Considering that the company's Bitcoin purchases during some weeks in this period plummeted to only a few hundred, this figure is not surprising. In contrast, Strategy's purchases in the first and second quarters of this year were both over 100,000 coins, and the sharp slowdown in the third quarter indicates a significant change in its purchasing capacity or willingness.

CryptoQuant analyst JA Maarturn explained that this slowdown may be related to the decline in the net asset value premium of the strategy. He stated that investors have previously paid a high “net value premium” for every dollar of Bitcoin on the Strategy balance sheet, effectively allowing shareholders to share in the profits from the rise of Bitcoin through leverage. However, since the middle of the year, this premium has narrowed.

(Source: CryptoQuant)

Due to the reduction of favorable factors in valuation, issuing new stocks to purchase Bitcoin no longer has the appreciation effect it used to have, thus weakening the motivation to raise funds. Maarturn pointed out: “Raising funds has become more difficult. The equity issuance premium has dropped from 208% to 4%.” The change in this figure is very persuasive. When the premium was 208%, Strategy issued new shares at 1 dollar, and the market was willing to pay 3.08 dollars, which allowed the company to raise a large amount of funds at a very low dilution cost. But when the premium drops to 4%, the same operation can only yield 1.04 dollars, and shareholders' dilution is hardly compensated.

Strategy Purchase Slowdown Key Data

Current Holdings: 674,000 Bitcoins (accounting for 3.4% of total supply)

Q3 Purchase Volume: 43,000 coins (this year's lowest quarter)

Partial Weekly Purchase: Only a few hundred coins (compared to tens of thousands in the early days)

NAV Premium Change: Plummeted from 208% to 4%

Impact: The motivation to issue new shares to purchase Bitcoin has been significantly weakened.

This structural constraint reflects not a loss of belief, but a critical point of the business model. The Strategy model relies on the market's willingness to pay a premium for its Bitcoin holdings; once the premium disappears, the model cannot be sustained. This case provides an important warning for other companies attempting to replicate the Strategy model: the Bitcoin vault model is effective in the early stages of a bull market, but as the market matures and the premium narrows, the sustainability of this model will be challenged.

Similar predicaments for other corporate buyers

At the same time, the cooling wave is not limited to Strategy. Metaplanet is a company listed in Tokyo, whose model emulates American Bitcoin pioneers. After experiencing a significant fall, its stock price recently fell below the market value of its Bitcoin holdings. This means that Metaplanet's stock market value is even lower than the value of the Bitcoin it holds, indicating that the market's valuation of its business model is negative. Investors believe that Metaplanet's holding of Bitcoin is a burden rather than an asset.

In response, the company approved a stock buyback plan while launching new financing guidelines to expand its Bitcoin reserves. This move demonstrates the company's confidence in its balance sheet, but it also highlights the waning enthusiasm of investors for the “digital asset reserve” business model. The stock buyback aims to narrow the discount between the stock price and NAV, but this strategy requires cash expenditure, which may further limit future purchases of Bitcoin.

In fact, the slowdown in the acquisition speed of Bitcoin vaults has led to mergers among some of these companies. Last month, the asset management firm Strive announced the acquisition of the smaller Bitcoin reserve company Semler Scientific. This deal will allow these companies to hold nearly 11,000 Bitcoins at a premium, as Bitcoin is gradually becoming a scarce resource in the industry. This merger trend indicates that small Bitcoin vault companies operating independently are losing market appeal, and only by integrating scale can they maintain their valuations.

According to Edwards, there are currently about 188 companies whose finance departments hold large amounts of Bitcoin, many of which have business models limited to their token exposure. This highly dependent model on a single asset is very attractive when Bitcoin prices are rising, but it becomes a fatal weakness in volatile or declining markets. These companies have no other sources of revenue and rely entirely on Bitcoin appreciation and stock premiums to sustain operations.

ETF has shifted from a one-way accumulation to a two-way market

(Source: SoSoValue)

Spot Bitcoin ETFs have long been viewed as automatic absorbers of new supply, but similar signs of weakness have now emerged. For most of 2025, these financial investment tools dominated net demand, with the amount created consistently exceeding the amount redeemed, especially during the period when Bitcoin soared to an all-time high. However, by late October, capital flows began to become unstable.

Due to adjustments made by portfolio managers, the risk department has also reduced investment exposure based on changing interest rate expectations, resulting in negative fund inflows for certain weeks. This volatility signifies that Bitcoin ETF behavior has entered a new phase. The macroeconomic environment is tightening, and market expectations for rapid interest rate cuts have diminished; real yields are rising, and liquidity conditions are cooling.

SoSoValue's data corroborates this shift. In the first two weeks of October, digital asset investment products attracted nearly $6 billion in inflows. However, by the end of the month, due to redemptions increasing to over $2 billion, some of the gains were reversed. This pattern indicates that Bitcoin ETFs have evolved into a true two-way market. They still provide ample liquidity and a channel for institutional investor participation, but they are no longer a one-way accumulation tool. When macroeconomic signals exhibit volatility, ETF investors can sell as quickly as they initially bought.

Despite this, the demand for Bitcoin remains strong, but now this demand is appearing in an explosive growth manner rather than a continuous wave. This change in demand pattern has had a significant impact on the price discovery mechanism. With sustained buying support, prices usually show a stable upward trend or sideways consolidation. However, when buying turns into intermittent bursts, the price volatility will significantly increase, leading to sharp fluctuations with large rises and falls.

Bitcoin Returns to High Beta Risk Asset Characteristics

This constantly changing situation does not necessarily mean an economic recession, but it does imply greater volatility. As the absorption capacity of businesses and ETFs weakens, the price trend of Bitcoin will increasingly be influenced by short-term traders and macroeconomic sentiment. Edwards believes that in this scenario, new catalysts such as monetary easing, regulatory clarity, or a return to risk appetite in the stock market may reignite institutional investors' buying enthusiasm.

Therefore, this impact is dual. First, the structural bidding that once provided support is weakening. During periods of insufficient supply and demand, the ability to suppress volatility declines due to a decrease in stable buyers, and intraday price fluctuations may intensify. Although the halving policy in April 2024 mechanically reduces new supply, scarcity itself cannot guarantee price increases without sustained demand.

Secondly, the correlation of Bitcoin is changing. As the expansion of balance sheets slows down, Bitcoin may once again align with the broader liquidity cycle. Rising real yields and a strengthening dollar could put pressure on prices, while a loose market environment may allow it to regain a leading position in a rising risk appetite rally. Essentially, Bitcoin is re-entering a macro reflective phase, with its behavior increasingly resembling that of high beta risk assets rather than digital gold.

All of this cannot deny Bitcoin's long-term development prospects as a scarce, programmable asset. On the contrary, it reflects the increasing influence of institutional factors, which have previously shielded Bitcoin from retail price fluctuations. It is the very mechanisms that initially drove Bitcoin into mainstream investment portfolios that now also tightly connect it with the gravitational pull of capital markets.

The next few months will test whether the asset can maintain its value storage appeal in the absence of automatic corporate or ETF inflows. If history is any guide, Bitcoin tends to adapt: when one demand channel slows, another often emerges, whether it comes from sovereign reserves, fintech integration, or a resurgence of retail participation during macro easing cycles.