Author: arndxt, encryption KOL

Compiled by: Felix, PANews

The only engine driving GDP now is artificial intelligence, while everything else is on the decline, such as the labor market, family conditions, purchasing power, and asset acquisition ability. Everyone is waiting for the so-called “cycle reversal.” But there is no cycle at all. The fact is:

- The market is not currently focused on the fundamentals.

- Capital expenditure on artificial intelligence is actually key to preventing a technological recession.

- A wave of liquidity is expected in 2026, and the market consensus has not even begun to price this in.

- Inequality is a headwind that hinders macroeconomic development, forcing the government to implement policies.

- The bottleneck of artificial intelligence is not in GPU, but in energy.

- For the younger generation, cryptocurrency is becoming the only asset class that truly has upward potential, making it meaningful.

Do not misjudge this transformation risk and invest funds in the wrong party.

1. Market dynamics are not driven by fundamentals

In the past month, despite no new economic data being released, prices have fluctuated significantly due to the shift in the Federal Reserve's stance.

The probability of interest rate cuts decreased from 80% to 30% and then rose back to 80%, entirely based on the remarks of individual Federal Reserve officials. This aligns with the situation where systemic capital flows in the market exceed subjective macro views.

Here is some evidence regarding microstructures:

Funds targeting volatility mechanically reduce leverage when volatility spikes and increase leverage when volatility declines. These funds do not care about the “economy” because they adjust risk exposure based on one variable: the level of market volatility. When volatility rises, they reduce risk → sell. When volatility falls, they increase risk → buy. This results in automatic selling during market weakness and automatic buying during market strength, thereby amplifying bidirectional fluctuations.

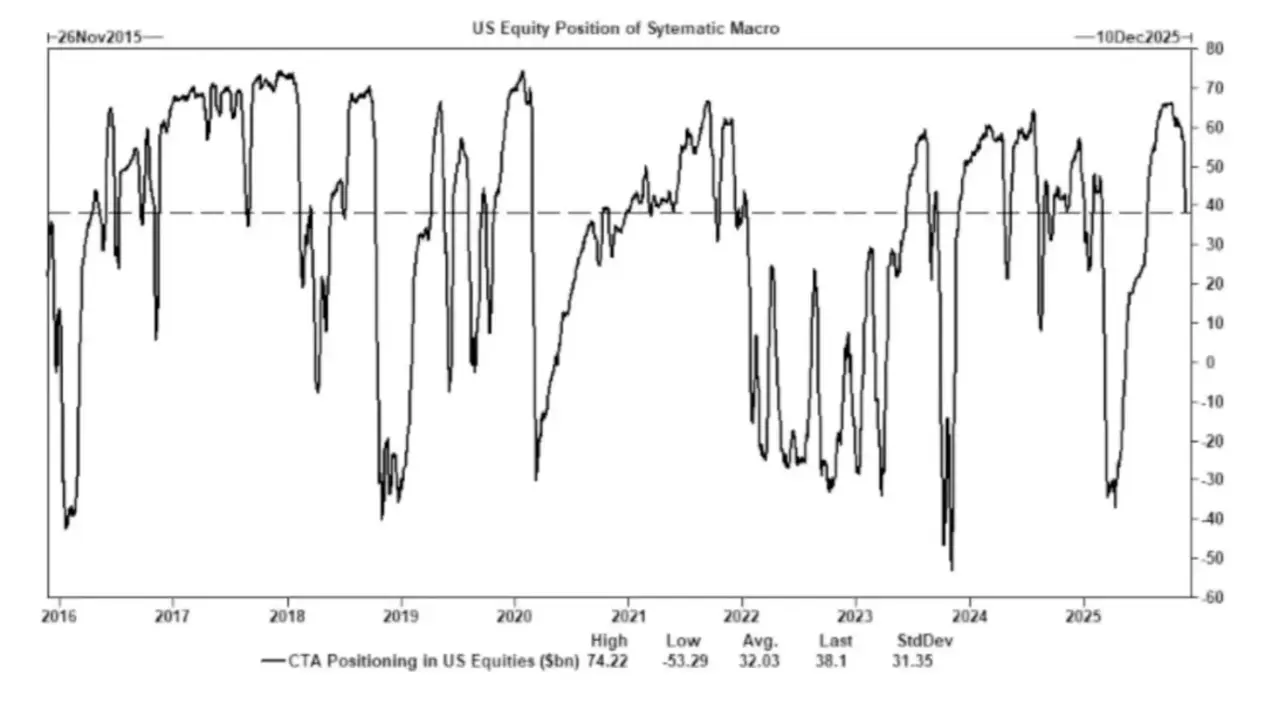

Commodity Trading Advisors (CTAs) switch long and short positions at preset trend levels, causing forced capital flows. CTAs follow strict trend rules:

- If the price breaks through a certain level → Buy.

- If the price falls below a certain level → sell.

There is no “viewpoint” behind this, just mechanical operation.

Therefore, even if the fundamentals do not change, when a sufficient number of traders set stop-loss orders at the same price at the same time, large-scale and coordinated buying or selling behavior will occur.

These fund flows can sometimes cause the entire index to fluctuate for several consecutive days.

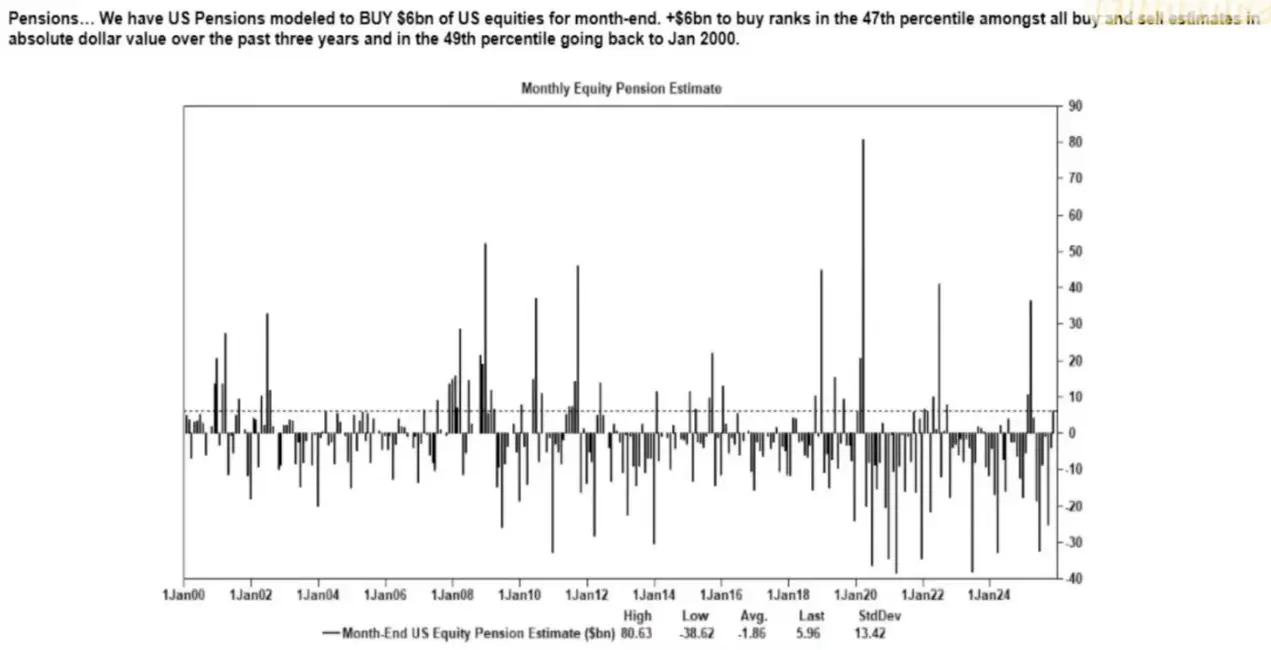

Stock buybacks remain the largest single source of net stock demand. In the stock market, companies buying back their own shares are the largest net buyers, surpassing retail investors, hedge funds, and pension funds. During the open buyback window, companies consistently inject billions of dollars into the market each week.

This caused:

- The inherent upward trend during the repurchase season

- Significant weakness after the repurchase window closes

- Structural demand unrelated to macro data

This is why stock prices may still rise even when market sentiment is extremely poor.

VIX curve inversion reflects a short-term hedging imbalance, rather than**“panic”****.** Generally, long-term volatility (3-month VIX) is higher than short-term volatility (1-month VIX). When this situation reverses, meaning the near-month contract price becomes higher, people will perceive that “panic has intensified.”

But today, it is usually caused by the following factors:

- Short-term hedging demand

- Options traders adjust risk exposure

- Capital inflow weekly options

- Systematic strategies are hedged at the end of the month.

This means:

- VIX index soaring ≠ panic sentiment.

- VIX index surge = hedging capital flow.

This distinction is crucial because it means that volatility is now driven by trading rather than by market sentiment.

This has led to the current market environment being more sensitive to market sentiment and more reliant on capital flows. Economic data has become a lagging indicator of asset prices, while the Federal Reserve's communication has become a primary trigger for volatility.

Liquidity, positions, and policy tone now drive price discovery more than fundamentals.

2. Artificial intelligence is preventing a full-blown recession

Artificial intelligence has begun to play the role of a macroeconomic stabilizer.

It effectively replaced periodic recruitment, supported corporate profitability, and maintained GDP growth in the context of weak labor fundamentals.

This means that the U.S. economy's dependence on capital spending for artificial intelligence is far greater than policymakers publicly acknowledge.

- Artificial intelligence is suppressing the demand for one-third of the labor force that is low-skilled and most easily replaceable. This is exactly where cyclical downturns typically manifest first.

- The improvement in productivity has masked the widespread deterioration in the labor market that would have been evident. Output remains stable because machines are taking over the work previously done by entry-level labor.

- Enterprises benefit from a reduction in the number of employees, while households bear the socioeconomic burden. This shifts income from labor to capital—this is a typical recession dynamic, yet it is obscured by the increase in productivity.

- Capital formation related to artificial intelligence artificially sustains the resilience of GDP. Without capital expenditure in artificial intelligence, the overall GDP data would be significantly weak.

Regulators and policymakers will inevitably support artificial intelligence capital expenditures through industrial policies, credit expansion, or strategic incentives, as otherwise, an economic recession would occur.

3. Inequality has become a macro constraint factor

Mike Green's analysis (with the poverty line around $130,000 to $150,000) has sparked strong opposition, indicating how widely this issue resonates.

The core fact is:

- Child-rearing costs exceed rent/mortgage

- Housing structurally difficult to obtain

- Baby Boomers dominate asset ownership

- The young group only has income, not capital.

- The asset inflation gap widens year by year

Inequality will force adjustments in fiscal policy, regulatory stance, and asset market interventions.

Cryptocurrency has become a tool for the population and a means for the younger generation to achieve capital growth.

4. The bottleneck of artificial intelligence lies in energy rather than computing power

Energy will become a new focal topic. Without the corresponding expansion of energy infrastructure, the artificial intelligence economy cannot scale. Discussions around GPUs overlook the larger bottleneck:

- Electricity

- Grid Capacity

- Nuclear and Natural Gas Construction

- Cooling Infrastructure

- Copper and critical minerals

- Data center site selection restrictions

Energy is becoming a limiting factor in the development of artificial intelligence.

Energy, especially nuclear energy, natural gas, and grid modernization, will become one of the most influential investment and policy areas in the next decade.

5. Two economies are rising, and the gap is widening

The U.S. economy is diversifying into a capital-driven artificial intelligence industry and labor-intensive traditional industries, with almost no overlap between the two.

The incentive mechanisms of these two systems are becoming increasingly different:

Artificial Intelligence Economy (Scale)

- High productivity

- High profit margin

- Light labor input

- Strategic Protection

- High capital attraction

real economy (contraction)

- Weak labor absorption capacity

- Consumer pressure is high

- Decrease in liquidity

- High asset concentration

- High inflation pressure

In the next ten years, the most valuable companies will build solutions that can reconcile or leverage these structural differences.

6. Future Outlook

- Artificial intelligence will be supported, as there is no other choice; otherwise, it will lead to economic recession.

- The liquidity led by the Ministry of Finance will replace quantitative easing as the main policy channel.

- Cryptocurrency will become a political asset class linked to intergenerational wealth.

- Energy will become the true bottleneck of artificial intelligence, rather than computing power.

- In the next 12 to 18 months, the market will still be driven by sentiment and capital flows.

- Inequality will increasingly influence policy decisions.

Related Reading: Macroeconomic Report: How Trump, the Federal Reserve, and Trade Triggered the Largest Market Volatility in History