Source: TaxDAO

“From Bottleneck to Turning Point: The Digital Assets and Fintech Industries are at a Crossroads.” ——Anatole Baboukhian, Head of Public Policy at FIS Worldpay

In a recent high-profile panel discussion, experts from Barclays, Bank of England, Goodwin Procter, Ripple and FIS Worldpay exchanged views on key aspects of the digital asset revolution, including the rise of CBDC, the role of stablecoins and tokens. Monetized bank deposits. They emphasized that while each approach offers unique potential benefits, such as improving financial inclusion or strengthening payments infrastructure, they also pose different regulatory challenges. The expert panel emphasized the need to create a regulatory environment to accommodate these new forms of digital assets and ensure a level playing field.

Central Bank Digital

Currencies)

- “There is a real opportunity here to get rid of one of the biggest […] inefficiencies in traditional finance, which is cross-border payments. It would be great for the public sector [through CBDCs] as well as the private sector to be involved in this things". *

Andrew Whitworth, director of corporate policy at Ripple

Central banks have begun to explore the potential of CBDC. A CBDC is a national legal tender issued in digital form by a country’s central bank, which can establish direct payment channels between individual citizens, businesses and other economic stakeholders, thereby supporting a resilient payment system. According to the panelists, cross-border payment hubs can also serve as building blocks for more efficient cross-border payments, which is one of the most promising use cases for the technology.

Source: Bank of England

Source: Bank of England

The technical specifications and functionality of a CBDC can vary significantly, and therefore the overall characteristics and use cases of a CBDC depend on the design decisions of the issuing jurisdiction.

Examples of design choices include:

· Enforcement of Anti-Money Laundering Policies and Travel Rules: While the latter is not (yet) implemented on most public blockchains (especially due to anonymity), panelists discussed the potential for CBDCs to leverage architecture and deploy privacy Enhancing the potential of technology to both protect user privacy and reduce financial crime: this is the subject of trials among technology companies, financial institutions, central banks and academia. In the UK, if a CBDC is introduced, strict privacy and data protection standards must be adhered to, as outlined in the Digital Pound Consultation.

· Transaction and Holding Limits: Authorities are concerned that CBDC has the potential to fuel bank runs. In the event of a banking crisis, a CBDC that is the direct responsibility of the central bank may be considered safer than uninsured bank deposits. In the event of a bank run, this could result in a massive outflow of bank deposits to the CBDC over a short period of time.

· Financial Inclusion: Community banks can increase financial inclusion by providing easier payment services, lowering transaction costs, and reaching underserved populations.

The panelists agreed that countries developing CBDCs must take into account key factors in their design, based on their own economic conditions and policy goals. Closely related to CBDCs in terms of their function as a means of payment are stablecoins and tokenized bank deposits.

Stablecoins and Tokenized Bank Deposits

*“MiCA is very concerned about stablecoins as regulators want to prevent unregulated organizations from circulating stablecoins”. *

Nicole Sandler, Head of Digital Policy, Barclays

Stablecoins are cryptocurrencies that are pegged to a stable asset, typically a currency such as the U.S. dollar or euro. This peg can be maintained through different mechanisms, including real-world asset reserves (such as USDC), algorithmic mechanisms (such as Terra’s failed UST), or cryptographic collateral (such as ETH-backed LUSD). A key use case for stablecoins is to protect market participants from the volatility of crypto assets while allowing them to take advantage of cryptocurrencies’ advantages, including speed and lower transaction costs.

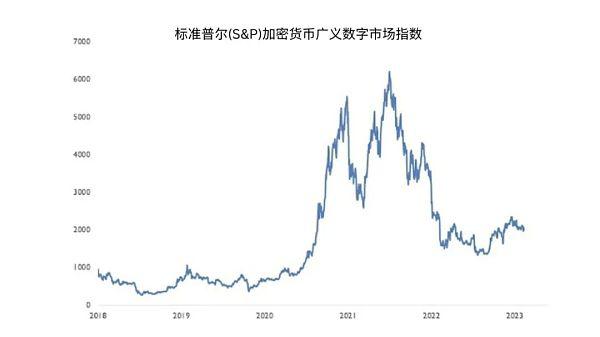

Cryptoassets are (still) very volatile, source: S&P Global S&P Global

Cryptoassets are (still) very volatile, source: S&P Global S&P Global

There are many types of stablecoins, and as their adoption rates increase, they have gradually attracted the attention of regulators because of their potential to impact traditional financial and banking systems. This makes stablecoins and their issuers a target for increased oversight by regulators. For example, the European Union’s Markets in Crypto Assets (MiCA) regulation creates a regulatory framework for cryptoassets and stablecoins. While there are concerns about MiCA’s lack of clarity (for example, member jurisdictions may have different licensing requirements for virtual asset service providers), it is generally seen as a positive development for the industry. This is in stark contrast to the law enforcement regulatory approach in the United States or the blanket bans on cryptocurrencies in places like China.

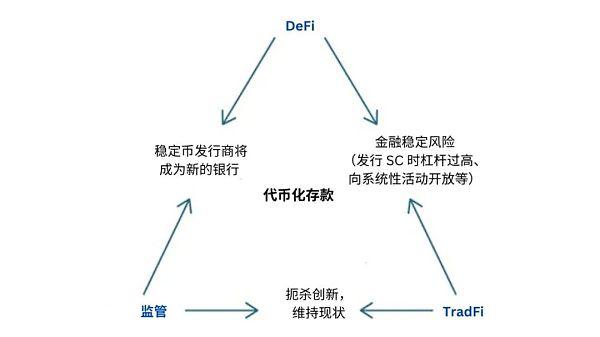

Tokenized bank deposits (TBDs) are an interesting alternative to CBDCs and stablecoins. TBDs are traditional bank deposits represented as digital tokens on a blockchain network. Bank deposits act as a backing mechanism to reduce market volatility and increase confidence in TBDs, as TBDs are backed by banks’ underlying assets, which are typically protected by deposit insurance schemes. In addition, TBDs could address regulatory bottlenecks, as they may largely fall within the purview of existing banking regulatory frameworks. As such, TBDs may be in the best position to solve the “stablecoin trilemma,” which forces regulators to choose between: 1) stifling innovation; 2) allowing stablecoin issuers to become the new banks; 3) ) financial stability risk.

The Stablecoin Trilemma Source: S&P Global Ratings S&P Global Ratings

The Stablecoin Trilemma Source: S&P Global Ratings S&P Global Ratings

Panelists discussed how the future of payment, whether it be CBDCs, stablecoins or TBDs, must focus on building a frictionless “payment journey” while ensuring security and consumer protections (such as privacy). They talked about the need to promote digital payments and the broader digital asset ecosystem within an internationally unified digital asset regulatory framework.

Promote interoperability and develop a unified regulatory framework

- “Regulation is not designed to suppress innovation. Rather, it is designed to ensure that innovation is carried out in a manner that effectively achieves its purposes, including safeguarding consumer protection and maintaining financial stability”. *

Amy Lee, Head of Fintech Center at the Bank of England

Regulation provides a stable framework for the market and aims to achieve the right balance between stability, consumer protection and innovation. In fact, panelists exchanged views on the impact of major missteps like FTX on the cryptocurrency space, as well as potential regulatory loopholes that could stifle innovation and hinder entry for legitimate market players. Regulatory standards can also address fragmentation and lack of interoperability among various technology architectures, which can adversely affect adoption and scaling.

A big challenge for interoperability within jurisdictions is how to connect digital signature technology with existing payments infrastructure. Such integration may require significant reforms to current payments infrastructure, which is often complex and rigid. To overcome this challenge, panelists discussed the need for central banks, fintech companies and traditional financial institutions to collaborate and support legal and regulatory approaches that will enable the integration of DLT into existing payment systems and (upcoming) CBDCs middle.

One promising example mentioned by panellists during the discussion was how Open Banking can address interoperability issues within jurisdictions, with its rollout in the UK aided by the development of regulatory standards. At the same time, when combined with DLT, it may also present potential opportunities to solve trust and digital identity issues.

Additionally, regulation can help overcome the fragmentation of international payments and promote interoperability by promoting consistency and coordination across jurisdictions. By harmonizing rules and standards, regulators can create a level playing field for all market participants. This in turn encourages collaboration between different systems such as CBDC, commercial bank currencies and the broader digital asset ecosystem. To achieve the best outcomes for payment users and to fully exploit the potential of digital assets, internationally harmonized regulations must be developed that balance innovation with consumer protection and financial stability.

Regulators may choose the same regime as traditional financial players, arguing that the same activities should be subject to the same regulations. Alternatively, regulators could develop more targeted regulatory regimes to address specific issues posed by new technologies, such as decentralization and anonymity. As DLT integrates into traditional finance, it will be critical for policymakers to align the level of regulation of crypto companies with that of traditional financial services providers. Arvin Abraham, partner at Goodwin Procter, said that bringing digital assets into mainstream financial services regulation is a clear direction. However, new regulation needs to take into account that digital assets are technically different from TradFi assets, and without a unified approach, the desired policy outcomes may not be achieved.

In the end, panelists agreed that the future of digital assets such as CBDCs, stablecoins and TBDs will be achieved through a balance of innovation, regulation and global cooperation. As Anatole Baboukhian highlighted, this is an inflection point where important choices will be made for the future development of digital currencies and payments. Realizing the promise of a digitized financial future will require coordinated efforts, ongoing dialogue, and a shared vision that fosters innovation while maintaining stability.