Author: Liu Jiao Lian

“Principal payments for Treasury holdings held by the Fed maturing in March that exceed the $25 billion monthly cap will be rolled over at auction,” the Fed slows down QT. Beginning April 1, principal payments on Treasury holdings held by the Fed maturing each month that exceed the $5 billion monthly cap will be rolled over at auction. Redeem Treasury bond coupon securities until the monthly cap is reached, and if the coupon principal payment falls below the cap, redeem the Treasury bills."

To put the Federal Reserve’s pedantic statement into plain language, it means that previously they needed to net sell $25 billion worth of U.S. Treasuries to the market every month, effectively withdrawing $25 billion of liquidity from the U.S. Treasury market. Now, they are directly reducing this selling pressure to $5 billion, which means they are taking out $20 billion less liquidity.

The pump mechanism has been reduced, and it has been significantly decreased, reduced by three-quarters.

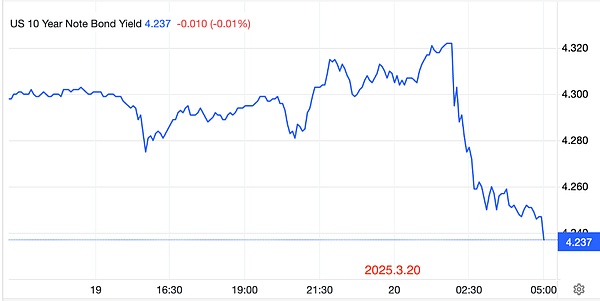

The effect is immediate. U.S. Treasury yields fell in response, breaking through the 4.3 mark, dropping from 4.32 all the way down to around 4.23.

The Federal Reserve’s reduction of net selling pressure on U.S. Treasuries has lessened the suppression of U.S. Treasury prices. As U.S. Treasury prices rise, yields will naturally fall.

Although the Federal Reserve will not begin implementing this policy until April 1, the market is bound to start acting in advance upon receiving the signal.

In this way, the Federal Reserve has achieved, on one hand, to maintain the benchmark interest rate unchanged, and on the other hand, a decline in U.S. Treasury yields.

In the article “Interest Rate Cut Trap” published yesterday on 2025.3.19, the Education Chain has already stated that the U.S. federal government, which urgently needs debt refinancing this year, is more concerned about whether U.S. Treasury yields can come down.

Powell gave the answer.

The Federal Reserve ultimately swallowed this half-cooked meal.

However, Powell’s meal is for the country, not for the risk speculation market.

Interest rates haven’t decreased, continuing to suppress leverage ratios. The sale of MBS hasn’t decreased, continuing to withdraw liquidity. Support for liquidity in risk markets is cautiously controlled at the lowest possible level.

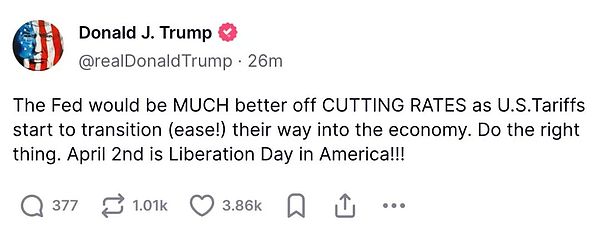

On the other hand, the president continues to post encouragement: The Federal Reserve better lower interest rates!

The game is still ongoing…

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.