On June 18, 2026, the Federal Reserve's Federal Open Market Committee voted 12-0 to keep the federal funds rate target range unchanged at 3.50% to 3.75%. This is the fourth consecutive time the Fed has held steady since completing three consecutive rate cuts in December 2025. The rate decision itself was a foregone conclusion, but what truly triggered a dramatic market repricing was the dot plot, Summary of Economic Projections, and the first press conference by new Chair Warsh that accompanied the decision.

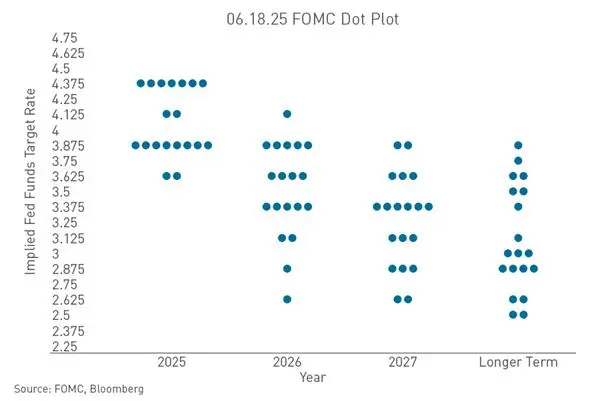

In just three months, Fed officials' views on the rate path have made an almost 180-degree turn. In March, the dot plot showed no official expected a rate hike in 2026, with the median rate projection at 3.4%, and the market's mainstream interpretation was that there was still room for rate cuts within the year. By June, the median had jumped to 3.8%—under the current rate range of 3.50% to 3.75%, this means Fed officials' judgment on the year-end rate level has shifted from 'still possible to cut' to 'at least one rate hike possible'.

How the Dot Plot Reversal Changed Market Expectations for the Rate Path

The most direct hawkish signal from this meeting came from the dot plot. Among the 18 officials who submitted rate projections, exactly half—9 people—believed a rate hike was needed in 2026. Of these, 1 expected a 75 basis point hike (three times), 5 expected a 50 basis point hike (twice), and 3 expected a 25 basis point hike (once). Of the remaining 9, 8 chose to stay on hold, and only 1 still insisted on a rate cut. Compared to March, the number of officials supporting a cut plummeted from 12 to 1, while those supporting a hike surged from 0 to 9. The dot plot's expectation for the Fed's rate action by end-2026 shifted from a 25 basis point cut to a 12.5 basis point hike, ending the previous rate cut expectations.

Why Inflation Has Again Become the Direct Reason for Fed Rate Hikes

The direct driver of the heightened rate hike expectations was the resurgence of inflation. The Fed sharply raised its 2026 full-year PCE inflation forecast from 2.7% to 3.6%, and core PCE from 2.7% to 3.3%. The magnitude of the upward revision is rare in recent years. In contrast, the economic growth forecast was only slightly revised down to 2.2%, while the unemployment rate expectation actually fell from 4.4% to 4.3%. This contradictory combination of 'soaring inflation, slightly weaker economy, strong employment' constitutes the current Fed dilemma—the U.S. economy is not weak enough to require rate cuts, yet inflation is too strong for the Fed to easily loosen its grip.

The nature of inflation is also changing. In May 2026, the U.S. CPI year-over-year rose to 4.2%, a new high since April 2023. Besides the external shock from energy prices, some longer-term factors are emerging. The AI boom is driving data center construction, electricity demand expansion, and sustained capital expenditure growth, which are increasingly seen by policymakers as a new source of inflation. Companies have announced more than $1.5 trillion in data center construction plans. Chip and high-tech equipment prices have risen significantly, and wages in the construction industry continue to climb. Fed Governor Cook previously noted publicly that AI-driven investment demand could further add new price shocks. Unlike traditional supply shocks, this type of AI-driven demand-pull inflation is characterized by greater persistence and a longer decline cycle. Warsh reiterated the 2% inflation target is non-negotiable multiple times at the press conference, stating that the Fed has failed to meet its inflation target for five consecutive years and 'now it's time to correct that.'

What Does It Mean That U.S. Bond Yields Are Staying Around 4.40%?

As of July 1, 2026, the benchmark 10-year U.S. Treasury yield closed at 4.47%, while the 2-year yield, more sensitive to Fed policy rates, closed at 4.183%. These levels are not just numbers—they are the result of the market pricing in the Fed's policy path, and the anchor for pricing all risk assets.

The 10-year yield hovering around 4.40% conveys at least three implications. First, the market is incorporating rate hike expectations into long-term rates. After the dot plot shift, Treasury yields rose overall and the curve flattened. Second, real interest rates remaining high are systematically compressing the valuation center of all interest-bearing assets. In an environment where the risk-free rate is near 4.50%, any risk asset's expected return needs to offer sufficient risk premium to attract capital. Third, the shape change of the yield curve itself transmits policy signals—when short-term rates rise due to rate hike expectations and long-term rates rise in tandem, the market is actually pricing in a 'higher for longer' rate environment. Warsh said at the press conference that the current policy is 'not particularly restrictive,' a statement that further solidified expectations of rates staying high. For crypto assets, the 10-year Treasury yield above 4.40% means the opportunity cost of holding non-interest-bearing assets is being recalculated.

How Dollar Strength Suppresses USD-Denominated Crypto Assets

Another direct consequence of rate hike expectations is a stronger dollar. After the June FOMC meeting, the U.S. dollar index has risen above 100. As of July 1, 2026, the dollar index was consolidating above the 101 level, closing at 101.16. The dollar index rose 0.08% on the day, closing at 101.187 in late trading.

The stronger dollar suppresses crypto asset prices through two channels. First, the exchange rate suppression channel—crypto assets like Bitcoin are primarily priced in U.S. dollars. Dollar appreciation means purchasing power measured in other currencies declines, weakening demand from non-U.S. investors. Second, the capital flow reallocation channel—rate hike expectations drive up yields on dollar-denominated assets, attracting global capital back into dollar assets and draining liquidity from high-volatility assets including crypto. More noteworthy is the structural strength of the dollar—the yen fell to a 40-year low against the dollar, breaking through the 162 level, which itself reflects the trend of global capital concentrating in dollar assets driven by interest rate differentials. During a dollar strength cycle, crypto assets face not only price pressure but also systemic challenges from shifts in the global liquidity landscape.

Through Which Channels Do Rate Hike Expectations Transmit to the Crypto Market?

The transmission of rate hike expectations to the crypto market is not singular or linear, but works through multiple channels simultaneously.

First, the opportunity cost channel. The rise in the risk-free rate directly increases the opportunity cost of holding non-interest-bearing assets (such as Bitcoin). When the 10-year Treasury yield reaches 4.47%, holding non-yielding crypto assets means forgoing considerable certain returns. This logic is particularly prominent in the asset allocation decisions of institutional investors—when the real yield on Treasuries is positive and rising, the narrative of crypto as an 'alternative store of value' faces challenges.

Second, the risk appetite channel. Rate hike expectations are usually accompanied by tightening financial conditions, leading to a systemic contraction in risk appetite. After the June FOMC meeting, the three major U.S. stock indices collectively plunged, with the Nasdaq falling over 1%; the crypto market reacted even more violently, with Bitcoin dropping from above $65,000 to around $64,000 after the meeting results, a decline of nearly 3%. The overall pressure on risk assets shows that rate hike expectations are triggering cross-asset de-risking operations.

Third, the liquidity channel. Rate hike expectations affect the quantity and cost of global dollar liquidity. When the Fed maintains high rates and the market prices in further hikes, global dollar liquidity tends to tighten, and crypto assets, highly sensitive to liquidity, are the first to be affected. Aggressive expectations from international investment banks further reinforce this logic—Bank of America expects the Fed to hike 25 basis points each in September, October, and December 2026, for a total of 75 basis points; Deutsche Bank predicts two rate hikes this year, 25 basis points each in September and December. Regardless of how many materialize, the mere existence of rate hike expectations is enough to persistently suppress risk asset valuations.

The Real Situation of the Crypto Market Under the Current Macro Environment

As of July 1, 2026, the crypto market is at the intersection of macro headwinds and internal structural pressures. Bitcoin fell to $58,531, with a cumulative drop of nearly 20% in the second quarter. The total market capitalization of global cryptocurrencies is approximately $2.17 trillion. Bitcoin briefly broke below the $59,000 mark and briefly tested the 200-week moving average near $58,000. CryptoQuant analysts pointed out that after Bitcoin fell below $70,000, the inflow of coins held for 6 to 12 months to exchanges surged, a pattern consistent with 'capitulation selling' by buyers at cycle tops in 2018 and 2022.

The current situation facing the crypto market can be summarized as: Macro expectations are deteriorating, but have not yet been fully priced in. After the June FOMC meeting, the CME FedWatch tool showed the probability of one rate hike within the year rose to above 80%. However, there remains significant uncertainty regarding the specific timing, magnitude, and whether the hike will ultimately materialize. Warsh emphasized that the dot plot is just a 'pencil sketch with an eraser,' and CITIC Securities tends to believe that Warsh himself will not support a rate hike within the year. Additionally, the US and Iran have signed an agreement; if oil price trends fall subsequently, rate hike expectations within the year could still retreat.

This uncertainty itself is the biggest pricing challenge for the crypto market. The market can neither fully rule out the risk of a rate hike nor confirm that it will not happen—in front of a Fed that no longer provides forward guidance, all asset pricing must revert to the interpretation of real-time economic data. For the crypto market, this means volatility may remain elevated, and the unfolding of a trend-driven market requires further clarity on the macro path.

FAQ

Q: What exactly did the Fed say at its June meeting?

On June 18, 2026, the Fed kept the federal funds rate unchanged at 3.50% to 3.75%, the fourth consecutive hold. But the dot plot showed 9 of the 18 officials expected at least one rate hike within the year, including 3 supporting one hike, 5 supporting two hikes, and 1 supporting three hikes. Warsh eliminated forward guidance and significantly streamlined the policy statement.

Q: Why did the market shift from discussing 'rate cuts' to 'rate hikes'?

The core reason is the rebound in inflation. The Fed sharply raised its 2026 PCE inflation forecast from 2.7% to 3.6%, and core PCE from 2.7% to 3.3%. The May CPI year-over-year rose to 4.2%. The stalled inflation decline combined with a solid labor market stripped rate cuts of their economic fundamental support.

Q: What does a 10-year Treasury yield of 4.40% mean for the crypto market?

The 10-year Treasury yield is an important benchmark for the risk-free rate. Yields staying above 4.40% mean the opportunity cost of holding non-interest-bearing assets (like Bitcoin) rises, while also reflecting that the market is pricing in rate hike expectations. This systematically suppresses the valuation of crypto assets.

Q: Will the Fed actually raise rates?

There is significant uncertainty. The dot plot shows deep internal divisions within the FOMC—9 support a hike, 8 support a hold, and 1 supports a cut. Warsh himself did not submit a dot plot and emphasized it has no commitment effect. CITIC Securities believes Warsh will not support a rate hike within the year. Whether rates are ultimately raised depends on subsequent inflation and employment data.

Q: What should the crypto market focus on next?

Three things should be closely watched: whether monthly inflation data (CPI/PCE) continue to exceed expectations, whether the labor market remains strong, and the impact of progress on Warsh's five working groups' reforms on the Fed's decision-making framework. Under the new paradigm where the Fed no longer provides forward guidance, every release of economic data could trigger a repricing of asset prices.