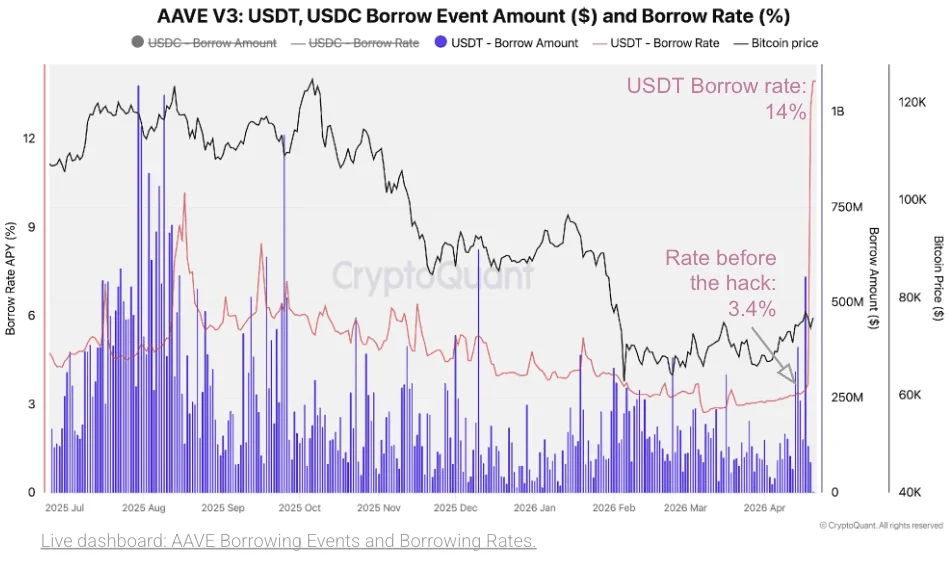

According to CryptoQuant’s assessment on April 23, the KelpDAO exploit that occurred last week created potential bad debt risk for Aave of between $124 million and $230 million within 72 hours, as TVL plunged 33%. The borrowing interest rates for USDT and USDC surged from 3.4% to 14%, while the ETH borrowing rate rose to the highest level since January 2024 at 8%.

Attack Mechanism: 83% of the rsETH supply concentrated on Aave amplifies the contagion effect

The attacker extracted unsecured rsETH from KelpDAO’s infrastructure and exchanged it for WETH and stablecoins on Aave, exploiting a critical vulnerability in the cross-chain bridge. The reason this contagion effect was so severe lies in the fact that Aave’s aETHrsETH contract holds about 83% of the circulating rsETH supply, making it the single protocol most heavily affected. CryptoQuant noted that Aave’s massive rsETH position caused risk contagion effects to far exceed the scope of the initial exploit.

Interest Rate Surge: A confirmation signal of systematic stress, not isolated volatility

(Source: CryptoQuant)

The lending interest rates across Aave V3’s three major markets rose in sync after the attack, showing the typical characteristics of stress across the system:

USDT and USDC lending rates: surged from 3.4% (the normal level before the attack) to 14%, reflecting a bank run-like squeeze in which users rushed to borrow stablecoins and exit the protocol.

ETH lending rates: climbed to 8% (the highest record since January 2024 according to CryptoQuant), then stabilized at around 5%, still more than double the 2% level before the attack.

The synchronized surge in interest rates across the three major markets formed what CryptoQuant described as a “typical DeFi liquidity crisis”: as depositors withdraw funds, borrower demand increases, available liquidity drops sharply, and rates reset to a much higher level.

USDe Contagion Shock: One of the largest-scale short-term redemption events in history

As the yield-bearing stablecoin USDe, the fourth-largest asset on Aave (with protocol deposits totaling $412 million), suffered a severe blow. Over three days, USDe’s total supply fell from $5.8 billion to $5.0 billion, a decrease of $800 million (a 14% drop). CryptoQuant called this one of the largest short-term redemption events for USDe in history.

This pressure compounded from two sources: risk-hedging sentiment cascading from the Aave crisis, and persistent negative funding rates on ETH and BTC perpetual contracts, which compressed USDe’s delta-neutral strategy returns and accelerated holders’ desire to redeem. As the world’s fifth-largest stablecoin (behind USDT, USDC, USDS, and DAI), USDe’s large-scale contraction further confirms a broader trend of significant liquidity withdrawal across the DeFi ecosystem.

Frequently Asked Questions

How does CryptoQuant quantify the specific bad-debt risk to Aave from this event?

CryptoQuant estimates that Aave faces potential bad-debt risk of between $124 million and $230 million. The quantification basis is that Aave’s aETHrsETH contract holds about 83% of the circulating rsETH supply, and then—together with the degree of rsETH depegging—it calculates the minimum and maximum bad-debt risk under two different loss-allocation scenarios.

Why was the surge in Aave lending and borrowing interest rates identified as a hallmark of systematic stress?

CryptoQuant pointed out that after the same event, the interest rates in Aave’s three major markets—USDT, USDC, and ETH—rose sharply in sync, rather than as isolated volatility in individual markets. The simultaneous surge across the three major markets indicates that the protocol’s available liquidity across the entire Aave system shrank in sync, which is a systematic manifestation of liquidity stress at the protocol level.

Why did USDe suffer large-scale redemptions during this crisis?

USDe’s redemption pressure compounded two factors: first, the spread of market risk-hedging sentiment triggered by the Aave crisis to USDe holders; second, persistent negative funding rates on ETH and BTC perpetual contracts, which compressed USDe’s delta-neutral strategy returns and sharply reduced the financial attractiveness of continuing to hold USDe, thereby accelerating large-scale redemptions.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

APE Surges 110% as Insider Allegedly Profits $2.27M Through Dual Position Trading on HyperLiquid

Gate News message, as $APE rose over 110%, a possible insider placed 2 orders (long and short) on $APE and made over $2.27M. The insider deposited 75 $ETH ($174K) to open long and short positions, then later bought 1,027 $ETH ($2.37M) on HyperLiquid and withdrew it from HyperLiquid.

GateNews5h ago

APE Spot-Futures Price Gap Widens Beyond 10%

Gate News message, April 24 — APE spot and futures markets are showing a price differential exceeding 10%, with spot trading at $0.1806 and futures trading at $0.16.

GateNews10h ago

TRADOOR Plunges 80% to $1.32

Gate News message, April 24 — TRADOOR experienced a sharp short-term decline of over 80%, currently trading at $1.32.

GateNews10h ago

ADA Price Outlook as Cardano Lands LSE Tokenized Deal

Key Insights

Cardano tokenized a Hannover Re reinsurance product and listed it on the London Stock Exchange, expanding blockchain use in regulated institutional markets.

ADA price holds within a descending wedge as support at $0.2400 remains intact while resistance near $0.2550 and $0.2824 l

CryptoNewsLand11h ago

Shiba Inu Burn Rate Surges 405% in 24 Hours, SHIB Posts 3.82% Monthly Gain

Gate News message, April 24 — Shiba Inu's token burn rate surged 405% over the past 24 hours, with over 2.5 million SHIB tokens permanently removed from circulation. The tokens were sent to inactive wallets, reducing the total supply as part of the ecosystem's long-term scarcity strategy.

The

GateNews11h ago

XRP Expands to Solana as wXRP Drives DeFi Access

Key Insights

Wrapped XRP on Solana surpasses 834,000 tokens, enabling new DeFi access while strengthening cross-chain liquidity and expanding XRP utility beyond its native ledger.

Ethereum and Solana dominate DeFi activity, while XRP Ledger trails significantly, driving the need for

CryptoNewsLand13h ago