#StablecoinDebateHeatsUp

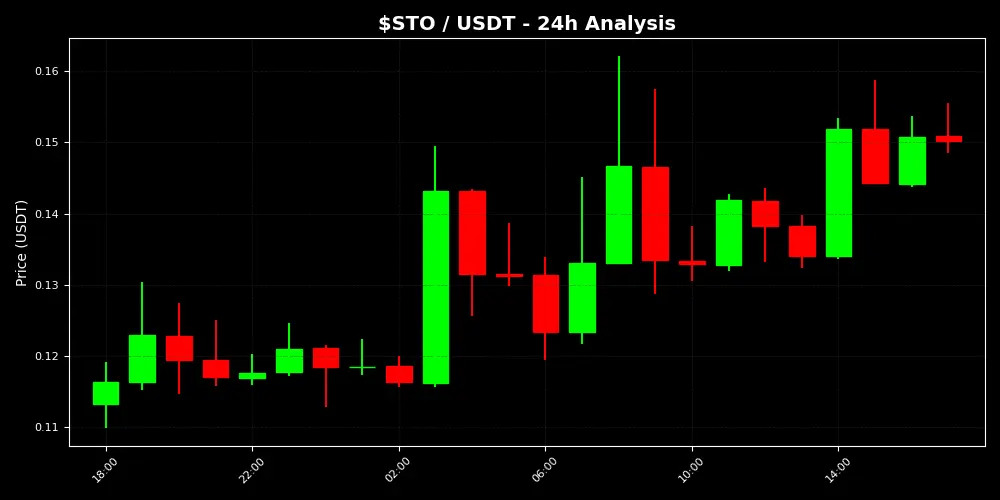

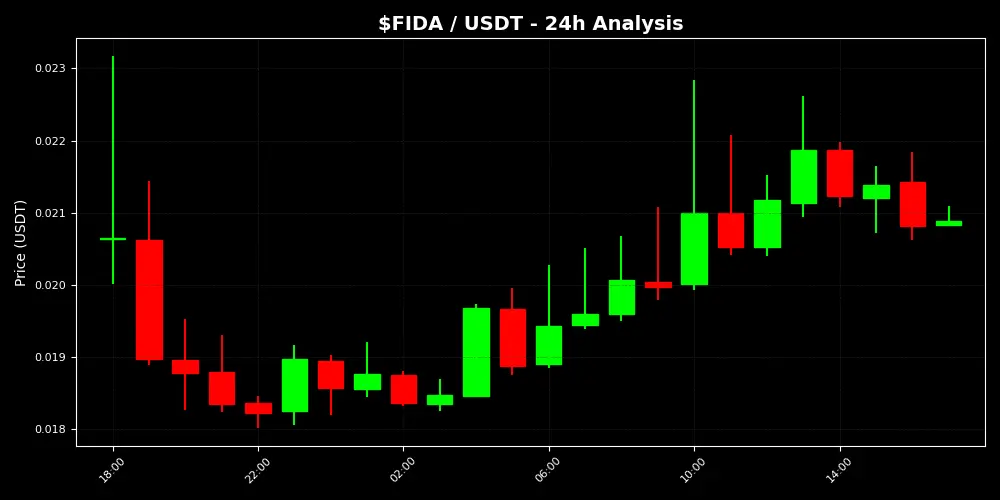

StablecoinDebateHeatsUp in early April two thousand twenty six as the recent release of draft implementation rules under the Guiding and Establishing National Innovation for US Stablecoins Act known as the GENIUS Act has intensified discussions around reserve requirements redemption at par prohibitions on paying interest or yield to holders capital standards licensing for national banks nonbank entities and foreign issuers as well as the balance between federal oversight and state level regimes for smaller issuers with outstanding issuance below ten billion dollars the GENIUS Act passed in July two thousand twenty five aims to provide a comprehensive federal framework for payment stablecoins emphasizing one to one backing with high quality liquid assets such as cash short term treasuries and segregated reserves while addressing consumer protection illicit finance risks and financial stability this comes alongside pakistan's Virtual Assets Act of two thousand twenty six which establishes the pakistan virtual assets regulatory authority or pvara as the permanent body for licensing supervising and enforcing compliance on virtual asset service providers including rules for fiat referenced tokens and asset referenced tokens that require full reserve backing par redemption audited disclosures and robust anti money laundering programs the debate centers on whether stricter rules like the office of the comptroller of the currency proposals with over two hundred questions for public comment including rebuttable presumptions against indirect yield through affiliates will stifle innovation or enhance trust and legitimacy in stablecoins like usdt and usdc which dominate the market with combined capitalization around three hundred billion dollars and daily transaction volumes reaching trillions the ongoing discussions highlight tensions between transparency operational safeguards and the ability for stablecoins to serve as efficient bridges between traditional finance and web3 activities particularly for users in pakistan who rely on them for trading remittances and decentralized finance participation while navigating local banking sensitivities.

The stablecoin debate has gained momentum with the treasury department and office of the comptroller of the currency notices of proposed rulemaking that seek public input on reserve asset segregation diversification requirements monthly audits redemption policies and prohibitions on yield payments that extend to affiliates and third parties to prevent circumvention and maintain a level playing field with traditional deposit taking institutions these proposals build on the genuis act's core principles of one to one backing and prompt par redemption while allowing smaller issuers to potentially opt for substantially similar state level regimes under treasury guidelines this regulatory clarity is welcomed by some as it could attract institutional capital and integrate stablecoins deeper into mainstream finance yet critics argue that overly restrictive measures on yield or rewards might limit competitive incentives and user adoption especially as usdc has recently overtaken usdt in adjusted transaction volumes signaling a shift toward more transparent compliant issuers in pakistan the virtual assets act of two thousand twenty six aligns with these global trends by mandating similar reserve and compliance standards for fiat referenced tokens under pvara oversight creating opportunities for licensed platforms but also imposing stricter know your customer and transaction monitoring that users must account for when depositing or withdrawing funds the heated debate underscores the need for balanced regulation that fosters innovation without compromising stability particularly as stablecoin market capitalization hovers near three hundred billion and plays a critical role in crypto liquidity.

When engaging with stablecoins amid this debate depositing funds into platforms carries risks amplified by evolving compliance expectations under both genuis proposals and pakistan virtual assets regulatory authority rules bank transfers or card deposits to acquire usdt or usdc may trigger automated fraud detection if they involve sudden large volumes or rapid conversions without corresponding trading activity prompting temporary holds or enhanced due diligence in cautious banking environments to mitigate these users should maintain a dedicated bank account isolated from everyday finances start with small test transactions on licensed platforms verify legitimacy through official channels and immediately move assets to self custody in hardware wallets after confirmation peer to peer deposits require selecting only highly rated verified merchants to avoid tainted funds that could later flag accounts network compatibility must be double checked to prevent irreversible losses overall a methodical deposit strategy with gradual scaling detailed record keeping of timestamps wallet addresses exchange statements and legitimate purposes such as trading or investment helps establish patterns of responsible use reducing the likelihood of activating risk controls during periods when regulatory scrutiny is heightened by the stablecoin debate.

Withdrawing funds involving stablecoins demands similar caution as platforms implement travel rule data sharing and redemption processes aligned with genuis requirements for prompt par value access while banks in pakistan may view incoming remittances from crypto sources as higher risk necessitating source of wealth proofs under pvara guidelines peer to peer withdrawals heighten freeze potential if counterparties use questionable accounts whereas centralized exchanges might impose limits during volatility for safer execution prioritize name matched direct transfers on regulated platforms implement withdrawal whitelisting use stablecoins intermediately to hedge any fluctuations and spread larger amounts over multiple sessions rather than single batches always verify fees networks and minimum limits while retaining full documentation including trading histories and rationales to address potential bank inquiries these practices not only align with the spirit of the genuis draft rules emphasizing transparency and safeguards but also complement local virtual assets act provisions promoting investor protection and smoother liquidity management in the web3 ecosystem.

To avoid triggering risk controls in the midst of the stablecoin debate users must adopt disciplined transparency and consistency by using a dedicated crypto only bank account to prevent cross contamination prioritize platforms and merchants with robust compliance records aligned with emerging us and pakistan standards avoid opaque third party payments keep comprehensive records of every transaction including screenshots confirmations and purpose explanations gradually scale volumes after modest tests to demonstrate legitimate activity complete know your customer verification early enable two factor authentication address confirmation prompts and withdrawal whitelisting monitor accounts daily and respond promptly to any documentation requests treating stablecoin operations as a professional structured activity with clear boundaries and incremental engagement significantly lowers operational hurdles allowing users to navigate the regulatory evolution without unnecessary disruptions as the genuis implementation and pvara framework bring greater legitimacy to the sector.

If a card freezes or an account restricts due to suspected stablecoin or crypto activity during this debate remain calm gather thorough documentation such as licensed exchange statements know your customer proofs trading records salary or business documents proving lawful sources contact the bank directly to obtain specific details and submit evidence of compliant activities under the virtual assets act or genuis aligned standards for authority involved cases file formal representations with affidavits highlighting responsible operations engaging a legal advisor experienced in financial and virtual asset regulations can expedite resolutions while maintaining cooperative communication many automated freezes resolve within days upon verification though serious cases may require escalation through ombudsman or judicial channels documenting impacts strengthens the position ultimately patience and evidence based responses transform challenges into manageable processes often restoring access without long term effects when activities align with the maturing regulatory landscape.

Key considerations and safer approaches for withdrawals amid the stablecoin debate include selecting regulated centralized platforms that support direct name matched transfers enforcing robust anti money laundering standards and offering compliance guidance over the counter services from licensed providers provide personalized support for larger volumes while limiting peer to peer to top rated counterparts implement whitelisting on exchanges for approved addresses maintain hardware self custody until the transaction moment and employ stablecoins to manage volatility spreading outflows temporally prevents pattern based triggers always cross confirm technical details and stay informed on both genuis proposals with their reserve redemption and yield restrictions as well as pvara directives in pakistan to utilize authorized channels that enhance protections and recourse treating withdrawals as part of strategic portfolio management rather than rushed actions preserves value and accessibility as stablecoins gain institutional backing through clearer rules.

By integrating these principles users can engage responsibly with stablecoins as the debate heats up contributing to a more stable and trustworthy web3 ecosystem where deposits and withdrawals facilitate efficient liquidity without undue risks continuous awareness of on chain developments regulatory updates from the office of the comptroller of the currency treasury and pakistan virtual assets regulatory authority alongside disciplined fund management empowers balanced participation that balances innovation with prudence in the evolving global digital asset space this comprehensive approach helps harness the benefits of stablecoins amid genuis implementation and local virtual assets act advancements ensuring sustainable engagement for individuals and businesses in pakistan and beyond as frameworks mature and provide foundational clarity for mainstream adoption.

StablecoinDebateHeatsUp in early April two thousand twenty six as the recent release of draft implementation rules under the Guiding and Establishing National Innovation for US Stablecoins Act known as the GENIUS Act has intensified discussions around reserve requirements redemption at par prohibitions on paying interest or yield to holders capital standards licensing for national banks nonbank entities and foreign issuers as well as the balance between federal oversight and state level regimes for smaller issuers with outstanding issuance below ten billion dollars the GENIUS Act passed in July two thousand twenty five aims to provide a comprehensive federal framework for payment stablecoins emphasizing one to one backing with high quality liquid assets such as cash short term treasuries and segregated reserves while addressing consumer protection illicit finance risks and financial stability this comes alongside pakistan's Virtual Assets Act of two thousand twenty six which establishes the pakistan virtual assets regulatory authority or pvara as the permanent body for licensing supervising and enforcing compliance on virtual asset service providers including rules for fiat referenced tokens and asset referenced tokens that require full reserve backing par redemption audited disclosures and robust anti money laundering programs the debate centers on whether stricter rules like the office of the comptroller of the currency proposals with over two hundred questions for public comment including rebuttable presumptions against indirect yield through affiliates will stifle innovation or enhance trust and legitimacy in stablecoins like usdt and usdc which dominate the market with combined capitalization around three hundred billion dollars and daily transaction volumes reaching trillions the ongoing discussions highlight tensions between transparency operational safeguards and the ability for stablecoins to serve as efficient bridges between traditional finance and web3 activities particularly for users in pakistan who rely on them for trading remittances and decentralized finance participation while navigating local banking sensitivities.

The stablecoin debate has gained momentum with the treasury department and office of the comptroller of the currency notices of proposed rulemaking that seek public input on reserve asset segregation diversification requirements monthly audits redemption policies and prohibitions on yield payments that extend to affiliates and third parties to prevent circumvention and maintain a level playing field with traditional deposit taking institutions these proposals build on the genuis act's core principles of one to one backing and prompt par redemption while allowing smaller issuers to potentially opt for substantially similar state level regimes under treasury guidelines this regulatory clarity is welcomed by some as it could attract institutional capital and integrate stablecoins deeper into mainstream finance yet critics argue that overly restrictive measures on yield or rewards might limit competitive incentives and user adoption especially as usdc has recently overtaken usdt in adjusted transaction volumes signaling a shift toward more transparent compliant issuers in pakistan the virtual assets act of two thousand twenty six aligns with these global trends by mandating similar reserve and compliance standards for fiat referenced tokens under pvara oversight creating opportunities for licensed platforms but also imposing stricter know your customer and transaction monitoring that users must account for when depositing or withdrawing funds the heated debate underscores the need for balanced regulation that fosters innovation without compromising stability particularly as stablecoin market capitalization hovers near three hundred billion and plays a critical role in crypto liquidity.

When engaging with stablecoins amid this debate depositing funds into platforms carries risks amplified by evolving compliance expectations under both genuis proposals and pakistan virtual assets regulatory authority rules bank transfers or card deposits to acquire usdt or usdc may trigger automated fraud detection if they involve sudden large volumes or rapid conversions without corresponding trading activity prompting temporary holds or enhanced due diligence in cautious banking environments to mitigate these users should maintain a dedicated bank account isolated from everyday finances start with small test transactions on licensed platforms verify legitimacy through official channels and immediately move assets to self custody in hardware wallets after confirmation peer to peer deposits require selecting only highly rated verified merchants to avoid tainted funds that could later flag accounts network compatibility must be double checked to prevent irreversible losses overall a methodical deposit strategy with gradual scaling detailed record keeping of timestamps wallet addresses exchange statements and legitimate purposes such as trading or investment helps establish patterns of responsible use reducing the likelihood of activating risk controls during periods when regulatory scrutiny is heightened by the stablecoin debate.

Withdrawing funds involving stablecoins demands similar caution as platforms implement travel rule data sharing and redemption processes aligned with genuis requirements for prompt par value access while banks in pakistan may view incoming remittances from crypto sources as higher risk necessitating source of wealth proofs under pvara guidelines peer to peer withdrawals heighten freeze potential if counterparties use questionable accounts whereas centralized exchanges might impose limits during volatility for safer execution prioritize name matched direct transfers on regulated platforms implement withdrawal whitelisting use stablecoins intermediately to hedge any fluctuations and spread larger amounts over multiple sessions rather than single batches always verify fees networks and minimum limits while retaining full documentation including trading histories and rationales to address potential bank inquiries these practices not only align with the spirit of the genuis draft rules emphasizing transparency and safeguards but also complement local virtual assets act provisions promoting investor protection and smoother liquidity management in the web3 ecosystem.

To avoid triggering risk controls in the midst of the stablecoin debate users must adopt disciplined transparency and consistency by using a dedicated crypto only bank account to prevent cross contamination prioritize platforms and merchants with robust compliance records aligned with emerging us and pakistan standards avoid opaque third party payments keep comprehensive records of every transaction including screenshots confirmations and purpose explanations gradually scale volumes after modest tests to demonstrate legitimate activity complete know your customer verification early enable two factor authentication address confirmation prompts and withdrawal whitelisting monitor accounts daily and respond promptly to any documentation requests treating stablecoin operations as a professional structured activity with clear boundaries and incremental engagement significantly lowers operational hurdles allowing users to navigate the regulatory evolution without unnecessary disruptions as the genuis implementation and pvara framework bring greater legitimacy to the sector.

If a card freezes or an account restricts due to suspected stablecoin or crypto activity during this debate remain calm gather thorough documentation such as licensed exchange statements know your customer proofs trading records salary or business documents proving lawful sources contact the bank directly to obtain specific details and submit evidence of compliant activities under the virtual assets act or genuis aligned standards for authority involved cases file formal representations with affidavits highlighting responsible operations engaging a legal advisor experienced in financial and virtual asset regulations can expedite resolutions while maintaining cooperative communication many automated freezes resolve within days upon verification though serious cases may require escalation through ombudsman or judicial channels documenting impacts strengthens the position ultimately patience and evidence based responses transform challenges into manageable processes often restoring access without long term effects when activities align with the maturing regulatory landscape.

Key considerations and safer approaches for withdrawals amid the stablecoin debate include selecting regulated centralized platforms that support direct name matched transfers enforcing robust anti money laundering standards and offering compliance guidance over the counter services from licensed providers provide personalized support for larger volumes while limiting peer to peer to top rated counterparts implement whitelisting on exchanges for approved addresses maintain hardware self custody until the transaction moment and employ stablecoins to manage volatility spreading outflows temporally prevents pattern based triggers always cross confirm technical details and stay informed on both genuis proposals with their reserve redemption and yield restrictions as well as pvara directives in pakistan to utilize authorized channels that enhance protections and recourse treating withdrawals as part of strategic portfolio management rather than rushed actions preserves value and accessibility as stablecoins gain institutional backing through clearer rules.

By integrating these principles users can engage responsibly with stablecoins as the debate heats up contributing to a more stable and trustworthy web3 ecosystem where deposits and withdrawals facilitate efficient liquidity without undue risks continuous awareness of on chain developments regulatory updates from the office of the comptroller of the currency treasury and pakistan virtual assets regulatory authority alongside disciplined fund management empowers balanced participation that balances innovation with prudence in the evolving global digital asset space this comprehensive approach helps harness the benefits of stablecoins amid genuis implementation and local virtual assets act advancements ensuring sustainable engagement for individuals and businesses in pakistan and beyond as frameworks mature and provide foundational clarity for mainstream adoption.