On July 1, 2026, Eastern Daylight Time, according to Google Finance data, Circle Internet Group (NYSE: CRCL) closed at $61.95, down 1.09%. Just on the previous trading day (June 30), CRCL experienced a more severe single-day plunge of 17.55%, closing at $62.63. On a cross-month basis, CRCL has accumulated a decline of over 40% in the past 30 trading days. From its April high (around $104) to the end of June, the market value of this "first stablecoin stock" has evaporated by over 40%.

A sharp stock price fluctuation is never the result of a single factor. CRCL's current decline has been compounded by multiple pressures: In June, FTSE Russell's annual index rebalancing removed Circle from several growth benchmark indices, including the Russell 1000 Growth Index and the Russell 3000 Growth Index, triggering passive sell-offs by index-tracking funds; at the same time, a competing stablecoin called Open USD (OUSD) officially launched on June 30, receiving support from more than 140 top global institutions. These two forces converged in the same time window, resulting in the most severe single-month decline in CRCL's history.

CRCL stock price performance and key events since listing (June 2025 – July 2026)

But putting aside the short-term technical factor of index rebalancing, the market reaction triggered by the emergence of Open USD points to a deeper structural issue: the competitive rules of the stablecoin industry are being redefined.

Open USD: Not just another stablecoin, but a "network alliance"

Open USD's debut is different from any stablecoin that has emerged in the past decade.

GUSD, FDUSD, TUSD, and various algorithmic stablecoins — all these challengers have ultimately fallen before the same reality: USDT monopolizes exchange liquidity, and USDC occupies the U.S. compliance gateway. Network effects act like an invisible wall, keeping newcomers out.

But Open USD did not choose to directly challenge this wall. Its strategy is: to bypass it.

On June 30, Open Standard announced the launch of Open USD, with a partner list covering more than 140 institutions in payments, banking, fintech, crypto infrastructure, and global commercial networks. Names such as Visa, Mastercard, Stripe, BlackRock, Google, Coinbase, Ripple, Solana, and Aptos Labs appear on the same list. Zach Abrams, co-founder and CEO of Bridge (a Stripe-owned stablecoin infrastructure company), serves as the interim CEO of Open Standard.

Open USD's design differs from existing stablecoins on three levels.

First, zero-fee minting and redemption. Enterprises can use OUSD without paying minting or redemption fees, with no volume caps. This directly targets the minting/redeem fee structures charged by USDC and USDT.

Second, reserve yield redistribution. The interest generated by the underlying U.S. Treasury reserves is returned to participating enterprises after deducting a small amount of operational costs. Under the current model, issuers (e.g., Circle) retain the vast majority of reserve interest income — according to Circle's filings, this source accounted for 99% of its 2024 revenue. With USDC's current circulating supply of approximately 73.7 billion tokens, Circle manages over $70 billion in reserve assets — the interest income from these reserves forms the absolute mainstay of the company's revenue.

Third, collective governance structure. Open USD is not controlled by a single company but operates through Open Standard, with a board composed of participating partners making joint decisions. Governance participants include payment companies, banks, exchanges, wallet service providers, and blockchain networks.

These three design elements combine to target a single goal: transforming stablecoins from "products dominated by a single issuer" into "multi-stakeholder payment infrastructure."

Macquarie analysts offered a direct assessment: Visa and Mastercard are no longer just "channels to support third-party stablecoins" — they are now the "owners" of the stablecoin ecosystem. Channels become owners, and the distribution logic of the entire value chain changes accordingly.

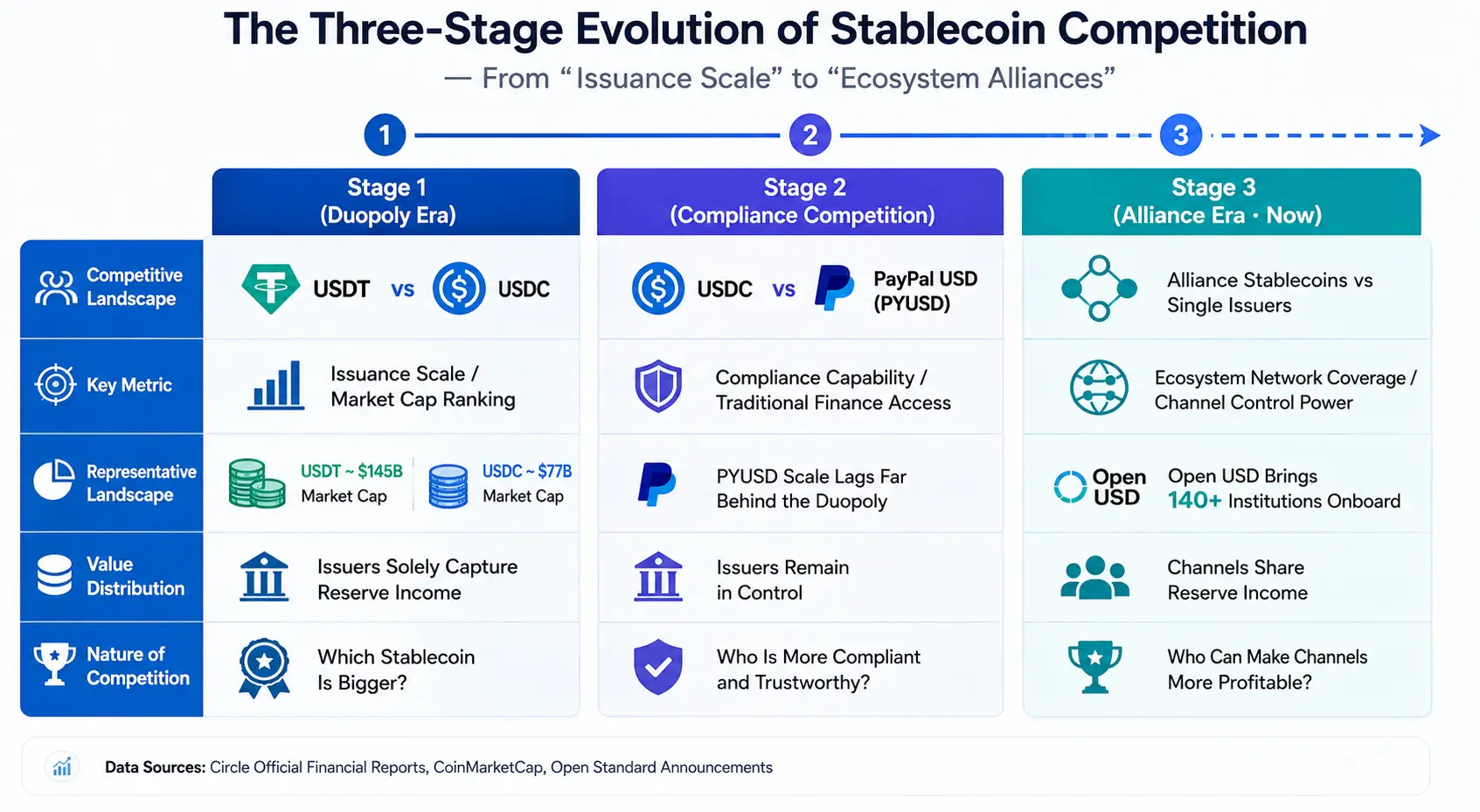

The three-phase evolution of stablecoin competition: From "circulation" to "ecosystem alliance"

Understanding the true significance of Open USD requires examining it within the evolutionary context of stablecoin industry competition.

Phase 1: The USDT vs USDC duopoly era. Competition in this phase revolved around "circulation." Whoever issued a stablecoin with a larger market cap and deeper liquidity had the advantage. Tether's USDT ranks first with a market cap of approximately $184.8 billion, while Circle's USDC ranks second at approximately $73.4 billion. Together, they account for 83.5% of the market cap of the top 100 stablecoins. The core competitive indicators are market cap ranking and circulation growth rate.

Phase 2: The "compliance" competition between USDC and PayPal USD. PayPal launched PYUSD in 2023, marking the entry of traditional payment giants into the stablecoin track. The focus of competition shifted from "scale" to "compliance capability" and "traditional financial on-ramps." However, PYUSD's market size still lags far behind USDC and USDT — the solo efforts of traditional giants have not truly shaken the duopoly.

Phase 3 (now): Alliance stablecoins vs single issuers. The emergence of Open USD marks a new dimension in stablecoin competition. This is not a competition between one company and another, but between an alliance of more than 140 institutions and a single issuer. The alliance members themselves are the owners of payment networks, banking systems, technology platforms, and crypto infrastructure — they not only provide capital but also distribution channels and application scenarios.

The essence of this evolution is: the competitive unit of stablecoins has upgraded from "single issuer" to "ecosystem network."

Open USD's core logic is that it redistributes the economic benefits of stablecoins to channel partners. In the traditional model, payment companies, exchanges, and wallet service providers help distribute USDC, but Circle captures the reserve yield. In Open USD's model, these channel partners become the beneficiaries of the yield themselves.

This change in benefit distribution could fundamentally alter the behavioral choices of channel partners. As market observers have noted: If Stripe previously helped Circle promote USDC, Circle pocketed the money; now OUSD says, "You promote me, and the money is yours" — the choice logic of channel partners will shift accordingly.

Three-phase evolution of stablecoin competition — from "circulation" to "ecosystem alliance"

Circle's true moat: More than just scale

The market's panic is understandable, but Circle is not defenseless.

William Blair analyst Andrew W. Jeffrey reiterated an "outperform" rating on CRCL after the plunge, citing Circle's first-mover advantage, stronger liquidity, and its stablecoin transfer infrastructure CPN (Circle Payments Network). He believes the market's concerns about competitive risks are overblown.

On July 1, Bernstein reiterated an "outperform" rating on Circle, setting a $190 price target, implying over 200% potential upside from the June 30 closing price of $62.63. The average analyst price target is approximately $143.48.

The logic behind these judgments points to several layers of structural advantages that Circle still possesses.

Compliance barrier. Circle's core market lies in the U.S. compliance space, with a strategy focused on compliance. USDC is one of the few stablecoins that meets the requirements of the GENIUS Act, and its ~$73 billion market cap is nearly 15 times that of its closest compliant competitor. The advancement of the U.S. CLARITY Act further provides certainty for Circle's business model. Compliance is not a barrier built overnight — it requires time, capital, and long-term accumulation of regulatory relationships.

Liquidity depth and DeFi ecosystem. USDC currently has a circulating supply of approximately 73.7 billion tokens, making it the deepest liquid dollar stablecoin after USDT. More importantly, about 75% of USDC circulates in crypto exchanges, DeFi protocols, and other scenarios. USDC is natively available on 30 blockchains, and Circle's Cross-Chain Transfer Protocol (CCTP) connects 19 of them, with cumulative transaction volume reaching $126 billion. In the first quarter of 2026, USDC processed nearly $30 trillion in on-chain transactions, capturing 80% of the dollar stablecoin market share. The depth and breadth of this network effect cannot be replicated by any new entrant in the short term.

Institutional adoption and developer support. More than 250 applications use USDC as base collateral. Circle's IPO valued the company at $9 billion on a fully diluted basis, and its public company status provides additional trust for institutional partnerships.

However, all of the above advantages share a common premise: they are built on USDC's circulation scale. And circulation scale depends on the distribution willingness of channel partners. Open USD is precisely targeting this link — it is not challenging USDC's technology or compliance, but rather the distribution of benefits between Circle and its channel partners.

The next round of stablecoin competition: Five key dimensions

If Open USD's model can be implemented, stablecoin competition will no longer be limited to "who has the larger market cap" but will expand into the following five dimensions.

Payment network coverage. The essence of a stablecoin is a "digital distribution network for the dollar." The quality of the distribution network depends on the number of merchants covered, the richness of payment scenarios, and settlement efficiency. Open USD's alliance members themselves own the world's largest payment networks — Visa, Mastercard, and Stripe cover millions of merchants. If these networks fully integrate OUSD, their distribution capability will be unmatched by any single issuer.

Enterprise adoption rate. The next phase of stablecoin growth will come from the enterprise side — cross-border payments, supply chain finance, payroll settlements, and other scenarios. The criteria for enterprises choosing a stablecoin include not only "stability" but also cost, efficiency, and partner trust. Open USD's zero-fee model and revenue-sharing mechanism are directly attractive to enterprise clients.

Regulatory resources. Stablecoin compliance is not a one-time investment but a continuous operational cost. Circle has built a first-mover advantage in this area. However, Open USD's alliance members — BlackRock, Standard Chartered, BNY Mellon — are themselves core participants in the global financial regulatory system. Their regulatory resources are equally formidable.

Cross-border payment capability. One of the core narratives of the stablecoin industry in 2026 is that stablecoins are becoming the "settlement layer of the internet." Cross-border fund flows involve the compliance logic of each jurisdiction. Whoever can quickly open more fiat on/off ramps across countries and regions will gain an advantage in cross-border payment scenarios.

RWA and AI Agent payment scenarios. Real-world asset (RWA) tokenization and AI Agent automated payments are widely seen as the twin engines for the next phase of stablecoin growth. Stablecoins are no longer just "issuing coins" but are reconstructing global financial infrastructure along three dimensions: AI payment authorization, on-chain credit for RWAs, and cross-border on-chain foreign exchange. In this dimension, Circle's developer ecosystem and cross-chain infrastructure (CCTP) are important competitive assets.

The channel is the moat. The future of stablecoins may hinge not on who is more "transparent" but on who can make channel partners more profitable. Whoever controls the channels controls the lifeline of stablecoins.

From this perspective, the decline of CRCL over the past month is a repricing by the market — not of Circle's current revenue ($653 million in reserve income in Q1 2026) — but of the future competitive rules of the stablecoin industry. When competition shifts from "issuer vs issuer" to "alliance vs single issuer," Circle's valuation logic needs to be re-examined.

This is not the end for Circle. USDC still has the deepest liquidity, the strongest compliance record, and the broadest DeFi integration. But Circle must answer a question it has never faced before: When channel partners themselves become stablecoin issuers and beneficiaries, can the single-issuer business model remain sustainable?

The answer will gradually emerge over the next few quarters.

FAQ

Q1: What are the core reasons for CRCL's over 40% drop in one month?

Mainly affected by two overlapping factors: first, FTSE Russell removed Circle from multiple growth indices during its annual rebalancing in June, triggering passive fund selling; second, the launch of Open USD raised market concerns about Circle's business model. The two forces coincided in the same time window, creating intense downward pressure.

Q2: What is the essential difference between Open USD and USDC?

Open USD adopts an alliance governance model, with more than 140 institutions participating in decision-making; it charges no minting or redemption fees; reserve asset yields are returned to partners after deducting operational costs. In contrast, USDC is issued solely by Circle, and the reserve yield is primarily retained by Circle — this source accounted for 99% of its 2024 revenue.

Q3: What advantages does Circle still have in competing against Open USD?

Circle possesses first-mover advantages, stronger liquidity (USDC circulating supply of ~73.7 billion tokens), compliance status meeting the GENIUS Act, the CCTP cross-chain infrastructure covering 30 blockchains, and a developer ecosystem with over 250 applications. These advantages are built on long-term capital investment and regulatory accumulation, and are difficult to replicate in the short term.

Q4: How is the competitive landscape of the stablecoin industry changing?

Stablecoin competition is evolving from "circulation competition" to "ecosystem alliance competition." The competitive unit has upgraded from a single issuer to an alliance network encompassing payment networks, banks, technology platforms, and crypto infrastructure. Future competition will revolve around dimensions such as payment network coverage, enterprise adoption rate, regulatory resources, cross-border payment capability, and RWA tokenization.

Q5: What could be the long-term impact of Open USD on the stablecoin market?

If Open USD's model is successfully implemented, it will change the distribution of value in the stablecoin chain — channel partners transition from "distributors" to "benefit earners." This could lead to a shift from "centralized issuer-led" stablecoin issuance to "multi-stakeholder payment infrastructure," driving the industry into a new phase where ecosystem networks become the core competitive advantage.