*Data last updated: 2026-04-15 11:06 (UTC+8)

As of 2026-04-15 11:06, Arm Holdings (ARM) is priced at $161,50, with a total market cap of $171,21B, a P/E ratio of 141,57, and a dividend yield of %0,00. Today, the stock price fluctuated between $160,00 and $163,00. The current price is %0,93 above the day's low and %0,92 below the day's high, with a trading volume of 6,25M. Over the past 52 weeks, ARM has traded between $100,02 to $183,16, and the current price is -%11,82 away from the 52-week high.

ARM Key Stats

About ARM

Learn More about Arm Holdings (ARM)

Gate Learn Articles

ARM Stock Analysis: Investment Opportunities and Risks in the Wake of the AI Boom

ARM's share price continues to climb following the recent AI surge, yet concerns about an inflated valuation persist. In this article, we examine ARM's investment outlook to support your investment decision-making.

2025-09-19

ARM Stock: Present Performance and Future Outlook Explained—A Beginner-Friendly Analysis

This article delivers up-to-date information on ARM's stock price, the underlying drivers of its performance, and a forward-looking perspective. Written in clear, straightforward language, it enables newcomers to quickly understand the essential aspects of investing in ARM.

2025-10-14

Demystifying ARM Stock: Can This Chipmaker Emerge as the Next Giant in the Age of AI?

This article begins with ARM's stock, examining how ARM's artificial intelligence (AI) strategies and semiconductor strategies influence its share price. The article integrates SoftBank’s capital allocation strategy and market expectations to offer new investors a clear investment framework.

2025-10-15

Blogs

Standard Chartered Expands into Crypto Prime Brokerage: Strategic Intent and Market Impact of a Traditional Financial Giant

Standard Chartered Bank is building a one-stop hub for crypto trading through its venture capital arm, signaling how traditional financial giants are quietly reshaping the digital asset landscape.

2026-01-14

Gate Ventures Announces Strategic Acquisition of Leading Decentralized Perpetual Exchange ADEN

Gate Ventures, the venture capital arm of the global leading crypto platform Gate, announced the strategic acquisition of ADEN, a top-tier decentralized perpetual exchange (Perp DEX).

2025-10-27

House of Doge (DOGE): When a Meme Steps Into the Financial Mainstream

Explore how this new corporate arm is launching reserves, ETPs, and adoption strategies to blend culture with institutional-grade utility.

2025-10-14

Arm Holdings (ARM) FAQ

What's the stock price of Arm Holdings (ARM) today?

What are the 52-week high and low prices for Arm Holdings (ARM)?

What is the price-to-earnings (P/E) ratio of Arm Holdings (ARM)? What does it indicate?

What is the market cap of Arm Holdings (ARM)?

What is the most recent quarterly earnings per share (EPS) for Arm Holdings (ARM)?

Should you buy or sell Arm Holdings (ARM) now?

What factors can affect the stock price of Arm Holdings (ARM)?

How to buy Arm Holdings (ARM) stock?

Risk Warning

Disclaimer

Other Trading Markets

Arm Holdings (ARM) Latest News

NVIDIA's Arm-Based PC Chip N1 Development Board Surfaces, Market Entry Imminent

Gate News message, April 15 — NVIDIA's N1 development board, an Arm-based system-on-chip (SoC) for Windows PCs co-developed with MediaTek since late 2024, has surfaced on a Chinese second-hand trading platform. The board features SK Hynix LPDDR5X memory modules and is priced at 9,999 yuan (approximately $1,370). The N1/N1X chips are believed to be derivatives of the GB10 used in NVIDIA's DGX Spark AI workstation, with clock speeds, memory bandwidth, and core counts adjusted for laptop environments. N1X integrates 10 high-performance Arm Cortex-X925 CPU cores, 10 power-efficient Cortex-A725 cores, and Blackwell GPU cores, aiming to enhance gaming and content creation capabilities on Arm-based Windows laptops. NVIDIA CEO Jensen Huang first mentioned the N1 chip in September last year during an announcement with Intel, stating it would be used in DGX Spark and similar products. The chip is expected to be officially unveiled during GTC 2026, held alongside Computex Taipei from June 1-4. Lenovo and Dell are reportedly preparing related product launches.

2026-04-10 06:31SK Telecom teams up with Arm and Rebellions to develop an AI data center inference solution

Gate News message: On April 10, SK Telecom announced that it has signed a trilateral memorandum of understanding (MOU) with Arm, a UK chip design company, and South Korean AI chip startup Rebellions, to jointly develop AI data center inference server solutions. Under the agreement, the three parties will combine Arm’s newly released AGI CPU and Rebellions’ AI acceleration chip RebelCard, expected to be launched in the third quarter of this year, to jointly develop AI inference servers and to test and validate them at SK Telecom’s AI data center. Among them, the Arm AGI CPU is optimized for high-density inference environments and large-scale AI deployments, while RebelCard is designed specifically for large-scale AI inference.

2026-03-25 08:05The Safest Middleman in the Chip Industry Takes the Most Dangerous Path

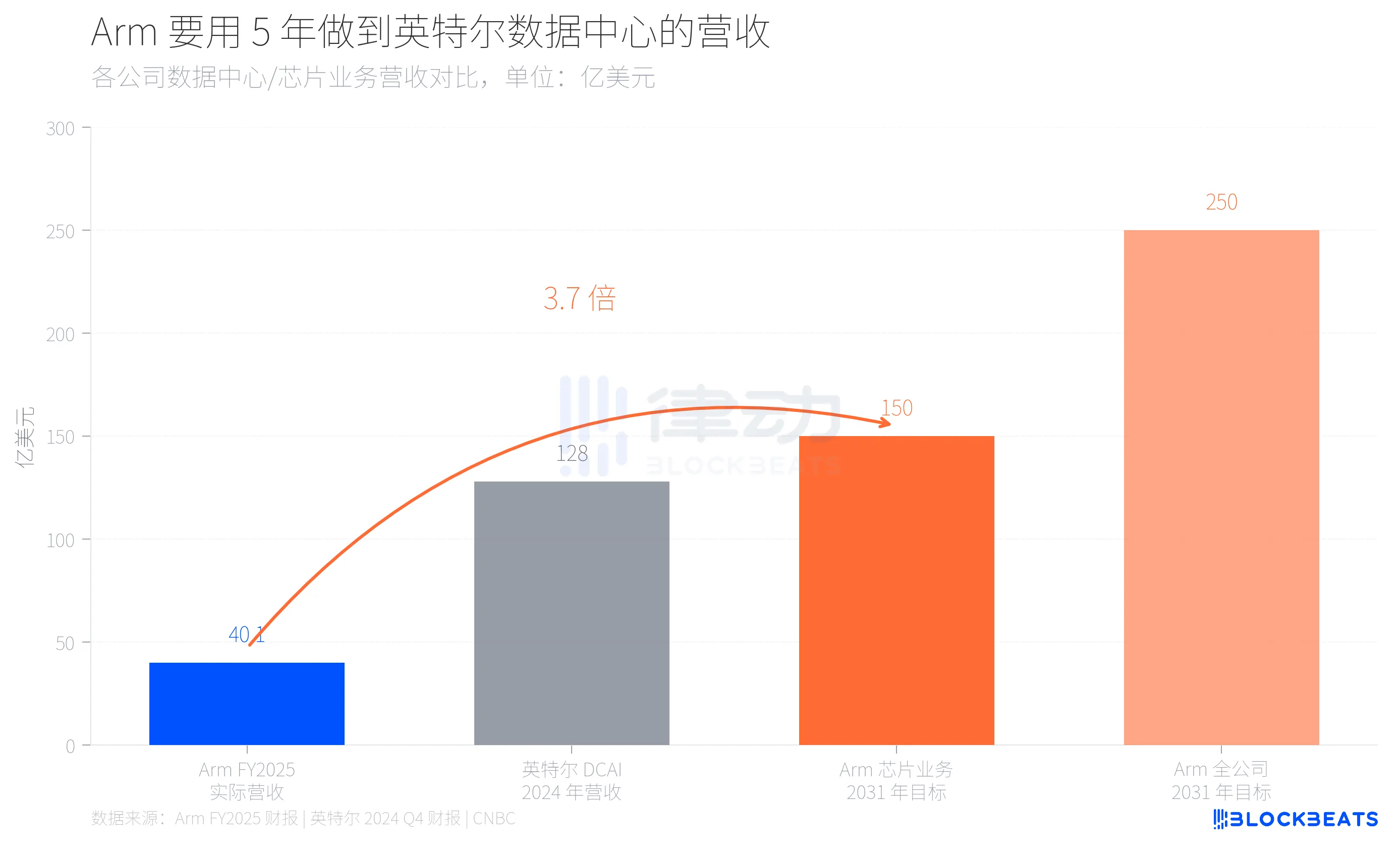

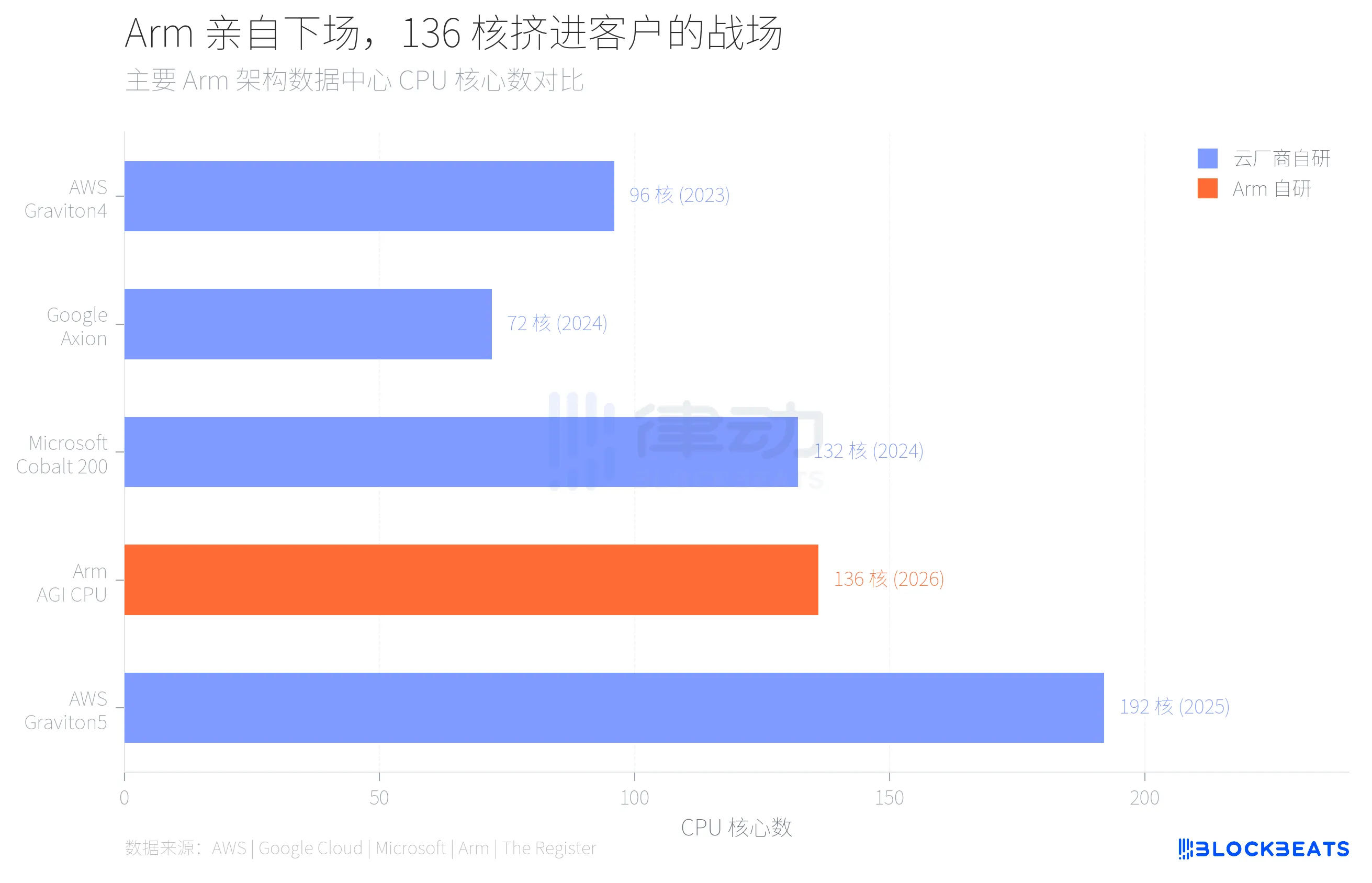

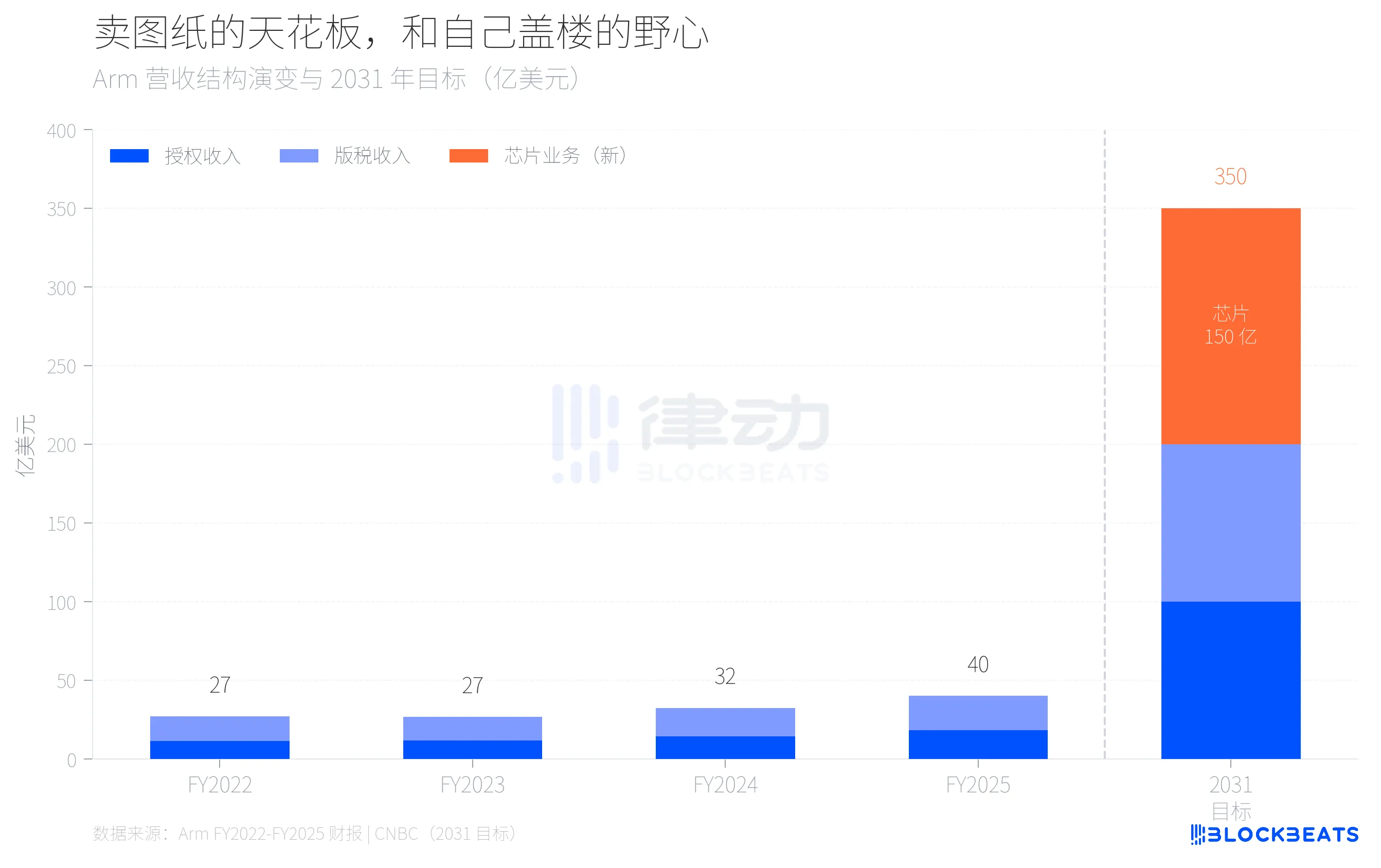

Between 4 billion dollars and 15 billion dollars, what lies between is not a growth curve but a self-revolution in business models. On March 24, Arm announced its first self-developed data center CPU in its 35-year history. Named AGI CPU, this chip features 136 Neoverse V3 cores, TSMC’s 3nm process, 300W TDP, with Meta as the first customer, planning large-scale deployment within the year. Also announced were collaborations with OpenAI, Cerebras, Cloudflare, SAP, and SK Telecom. Arm CEO Rene Haas provided a set of target figures at the launch, stating that the chip business aims to reach $15 billion in annual revenue by 2031, with the entire company’s total revenue at $25 billion and earnings per share of $9. What does this mean? Arm’s total revenue for FY2025 (ending March 2025) is $4.007 billion, according to Arm’s annual report, with licensing income of $1.839 billion and royalty income of $2.168 billion, and a gross margin of 97%. In other words, a company with $4 billion in annual revenue is expected to grow nearly to the scale of Intel’s entire data center division within five years based on a new business. According to Intel’s Q4 2024 financial report, Intel’s Data Center and AI (DCAI) division will generate $12.8 billion in revenue for 2024.  From $4 billion to $15 billion, a 3.7x leap, behind which is Arm’s attempt to transform from a pure IP licensing company into a hybrid that sells both design blueprints and finished products. This has no precedent in the chip industry. Why is Arm taking this risk? The answer lies in its customer list. Over the past three years, Arm’s largest data center clients have been doing the same thing. According to publicly available data from AWS, Amazon has migrated over 50% of its EC2 compute capacity to its self-developed Graviton chips, with the latest Graviton5 reaching 192 cores. Google Cloud disclosed that its Axion chips have migrated over 30,000 internal applications, improving efficiency by 80%. Microsoft’s Cobalt 200, based on Arm Neoverse architecture, uses TSMC’s 3nm process and has 132 cores.  These cloud providers are using Arm architecture licenses, but the chips are designed, fabricated, and deployed by themselves. Arm earns licensing fees and royalties, not chip profits. As more computing power is absorbed by these self-developed chips, Arm’s revenue ceiling in data centers becomes increasingly clear. Looking at Arm’s revenue structure over the past four years, the outline of this ceiling becomes more concrete. According to Arm’s financial reports, from FY2022 to FY2025, the company’s total revenue grew from $2.7 billion to $4 billion, with an average annual growth of about 14%. Royalties increased from $1.562 billion to $2.168 billion, and licensing income from $1.141 billion to $1.839 billion. The growth rate of royalties has slowed to around 20%, largely driven by upgrades to the mobile Armv9 architecture, not data center developments.  Extrapolating this growth rate, even if licensing and royalty income grow about 20% annually, the total would reach only around $10 billion by 2031. The remaining $15 billion must come from a new business that doesn’t yet exist today. This is the arithmetic behind Arm’s decision to build its own chips. Choosing to develop chips in-house essentially means competing with its own customers. A company that sells blueprints starts building its own buildings, while its blueprint buyers have been constructing for years. This is the real background of the 136-core AGI CPU. According to The Register, this chip has a base frequency of 3.2 GHz, up to 3.7 GHz, 12 DDR5 memory channels, 6 GB/s bandwidth per core, 96 PCIe 6.0 lanes, and supports CXL 3.0. Arm positions it as “the computing foundation for the agentic AI cloud era,” focusing on CPU-side task scheduling and data flow management in AI inference, not directly competing with GPUs. The pace of market share change also tells the story. According to Omdia, by 2025, Arm-based servers will account for about 21% of global shipments, with a 70% growth rate. But within hyperscale data centers, this share is already close to 50%. The 40-year monopoly of x86 isn’t collapsing but being replaced chip by chip. The risk of Arm’s self-developed chips isn’t technological but relational. Meta’s willingness to be the first customer is partly because Meta itself lacks a mature in-house chip project like Amazon or Google. But how will Amazon, Google, and Microsoft view this? If a supplier starts competing for your business, will you still entrust it with your most core architecture licensing? Arm’s gamble is that the overall growth of the data center market outpaces the deterioration of customer relationships. Rene Haas clearly believes that the incremental demand for CPUs in the AI era is large enough for self-developed chips and architecture licensing to coexist. The $15 billion target is a pricing of this judgment. Selling blueprints for 35 years, now building its own buildings for the first time. The blueprints are still being sold, and the buildings are being constructed—only whether they can fit on the same land remains to be seen. Click to learn more about Rhythm BlockBeats job openings. **Join the Rhythm BlockBeats official community:** Telegram Subscription Group: https://t.me/theblockbeats Telegram Group Chat: https://t.me/BlockBeats_App Twitter Official Account: https://twitter.com/BlockBeatsAsia

2026-03-25 00:16OpenAI Foundation Plans to Invest $1 Billion in 2026, Focusing on AI Risk Prevention and Life Sciences

Gate News Report, March 25 — OpenAI plans to invest $1 billion this year through its nonprofit arm, the OpenAI Foundation, in various artificial intelligence-related initiatives. The OpenAI Foundation intends to focus its 2026 expenditures on helping society mitigate potential AI risks and funding efforts that leverage AI to advance life sciences. The foundation will invest through external grants and projects and has hired key figures such as Wojciech Zaremba and Jacob Trefethen to lead this nonprofit organization.