Author: Jademont, Evan Lu, Waterdrip Capital

The New Industrial Revolution: Computing Power Becomes the Engine of the Economy

“In this world, only a very few people can, like Edwin Drake, inadvertently usher in an era that changes human history… His drill bit, penetrating deep into the ground, not only touched black liquid but also the arteries of modern industrial civilization.”

In 1859, amidst the muddy fields of Pennsylvania, people gathered around Colonel Drake (Edwin Drake), mocking him. At that time, the world’s lighting still relied on increasingly scarce whale oil, but Drake was convinced that underground “rock oil” could be mined at scale. This was considered a madman’s delusion at the time. Until the first gush of black liquid erupted, no one could have imagined that the emergence of oil would not only replace whale oil as a lighting energy but also become the cornerstone behind the struggle for dominance in human society over the next two centuries, reshaping global power and geopolitics for the next hundred years. Human history reached a turning point: old wealth depended on trade and shipping, while new wealth rose with the advent of railroads and energy (oil).

Today, in 2025, we are in a very similar game. However, this time, the frantic flow is the computing power flowing through silicon chips, and this time’s “gold” is the code engraved on the chain; the new era’s “gold” and “oil” are reshaping our entire understanding of productivity and store-of-value assets. Looking back at 2025, the market experienced unexpectedly intense volatility. Trump’s aggressive tariff policies forced global supply chains to relocate, triggering a massive inflation rebound; gold hit a historic high above $4,500 amid geopolitical uncertainties; the crypto market, despite epic gains from the GENIUS Act at the beginning of the year, experienced painful liquidations in early October due to leverage unwinding.

Beyond macro fluctuations, a consensus in the AI computing industry is rapidly fermenting: Nvidia, the “AI Water Seller,” reached a milestone market cap of $5 trillion in October. Additionally, giants like Google, Microsoft, and Amazon have invested nearly $300 billion in AI infrastructure this year. For example, xAI’s upcoming completion of a million-GPU cluster by year-end indicates the importance of computing power. Elon Musk’s xAI built the world’s largest AI data center in Memphis in less than half a year and plans to expand to an astonishing scale of 1 million GPUs by the end of the year.

The Era of Digital Intelligence: The Main Theme of the Next Industrial Revolution

Ray Dalio, founder of Bridgewater Associates, once said: “Markets are like machines; you can understand how they work, but you can never predict their behavior precisely.” Even though macro environments are unpredictable and random, it is undeniable that AI remains the most significant long-term growth channel in the US stock market. Over the next decade, AI technology has become the most critical core gear in the market machinery; it continues to influence all aspects of government, enterprise, and individual life.

Despite ongoing debates about an “AI bubble,” many institutions warn that the AI investment boom shows signs of bubble-like tendencies: Morgan Stanley research pointed out that in 2025, investment growth in AI led to soaring valuations of tech stocks without significant productivity gains, reminiscent of the internet boom of the 1990s.

But an unavoidable fact is that the productivity revolution driven by AI is gradually entering a tangible realization phase. From an investment logic perspective, AI is no longer just a narrative for tech giants; the efficiency dividends and extreme cost optimization it brings are the main drivers of profit and productivity growth for non-tech companies. However, behind this lies a brutal trade-off: AI’s impact on employment, especially white-collar jobs, is undeniable. The most direct manifestation is the exponential reduction of entry-level positions; basic coding, accounting, auditing, and even junior management consulting and legal roles could be among the first to be replaced by AI.

As AI applications deepen, risks of unemployment in healthcare, education, and retail sectors are accumulating. Recently, a cruel joke has circulated in the US investment community: software engineers in the future will be like today’s “civil engineers”; as Elon Musk emphasized in interviews, AI will replace everyone’s jobs. But this also signals the arrival of a new industrial era for AI, called the “Digital Intelligence Era.”

Looking Ahead to 2026: The Demand for AI Will Continue to Expand

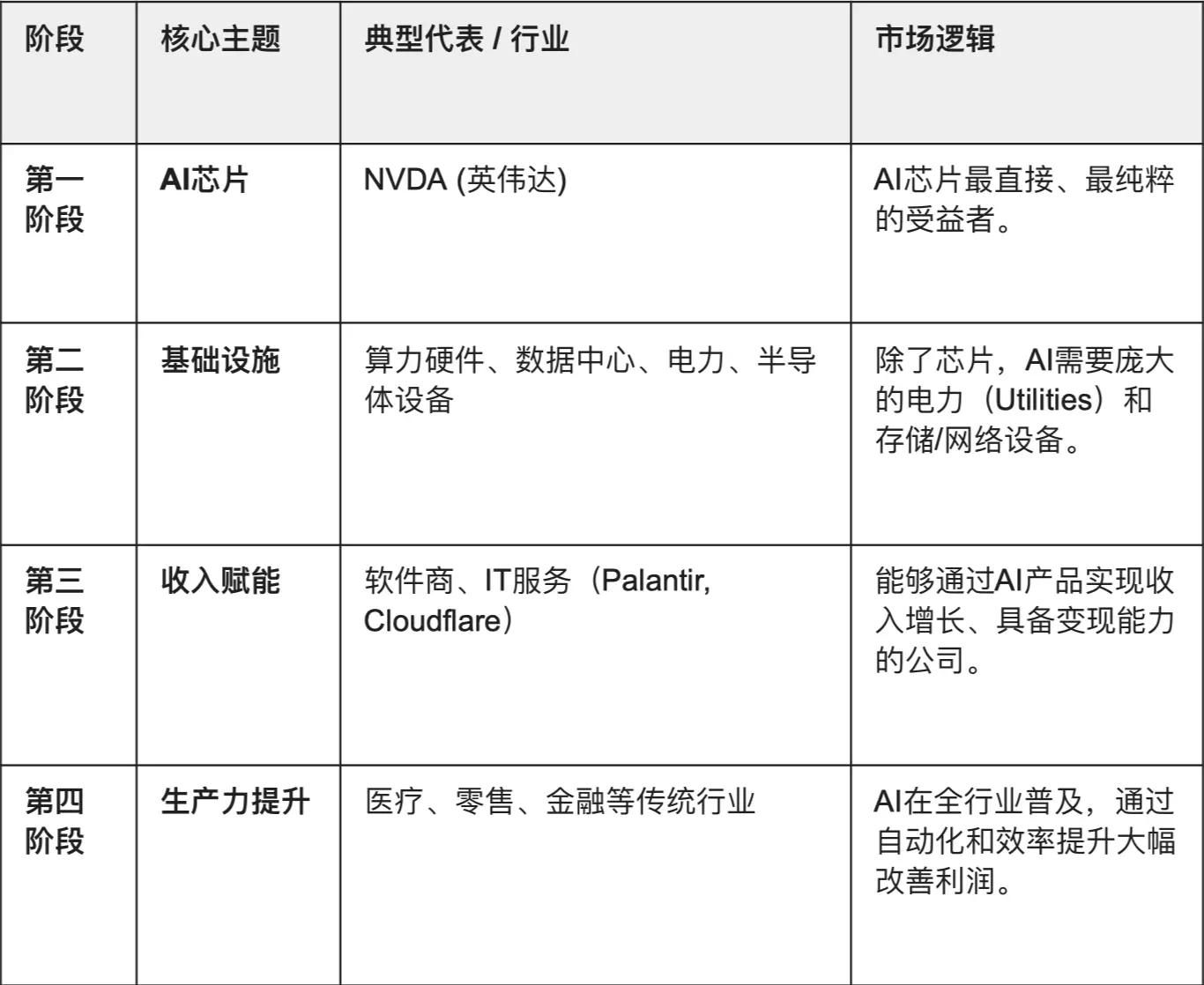

Four Stages of Investment in the AI Industry

As the AI boom moves from concept to full industry adoption, and with the market already fully pricing in the MAG7 (the seven major US tech giants), where will the next wave of growth in AI themes come from? Goldman Sachs stock strategist Ryan Hammond proposed the “Four Stages of AI Investment” model, outlining the subsequent path: AI investment will sequentially go through four stages: chips, infrastructure, revenue enablement, and productivity enhancement.

Source: Four Stages of AI Investment Model

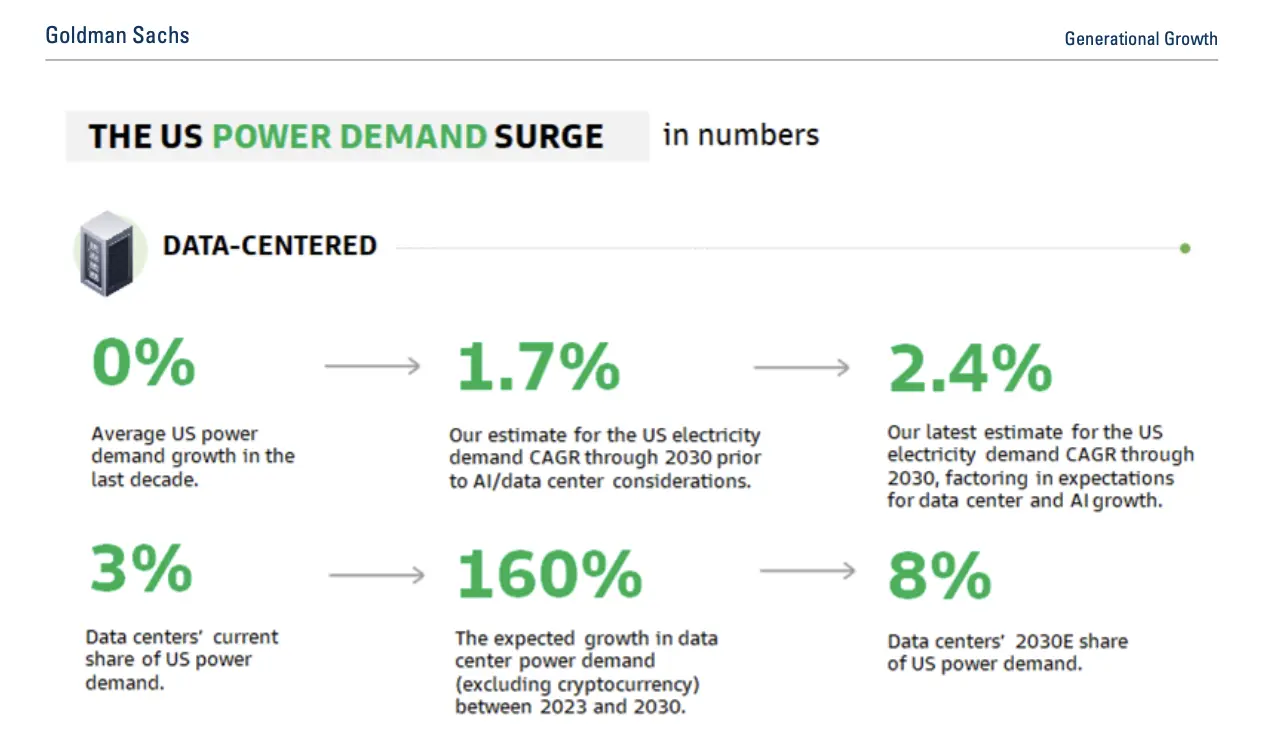

Currently, the AI industry is at the intersection transitioning from “Infrastructure Expansion” to “Application Deployment,” i.e., moving from Stage 2 to Stage 3. The demand for AI infrastructure is in a phase of explosive growth:

- By 2030, global data center electricity demand will increase by 165%

- From 2023 to 2030, the compound annual growth rate (CAGR) of US data center electricity demand will be 15%, raising data center share of total US electricity consumption from 3% now to 8% in 2030.

- By 2028, global spending on data centers and hardware will reach $3 trillion.

Goldman Sachs forecast of US data center electricity demand, image source

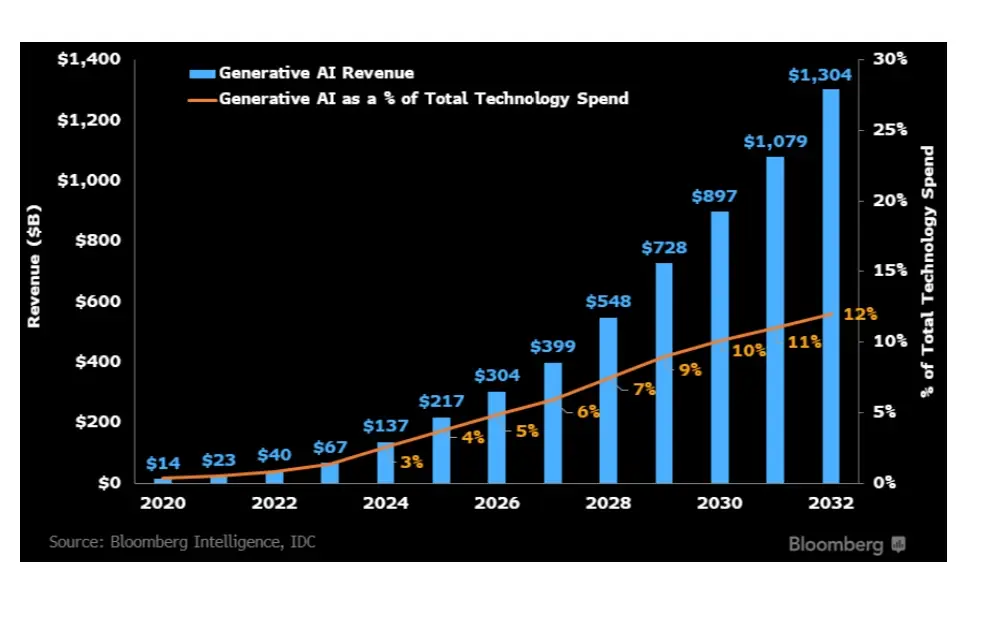

Meanwhile, the generative AI application market is also exploding, projected to grow to $1.3 trillion by 2032. In the short term, building training infrastructure will drive a 42% CAGR; in the medium to long term, growth will shift toward inference devices for large language models (LLMs), digital advertising, and specialized software and services.

Bloomberg: Future 10-Year Growth Forecast for Generative AI, data source

This forecast will be validated by 2026. Goldman Sachs’s latest macro outlook in 2026 states: 2026 will be the “Year of Realized Returns” for AI investments, with AI significantly reducing costs for 80% of non-tech companies in the S&P 500. This will test whether AI can truly shift from “potential” to “performance” on corporate balance sheets.

Therefore, in the next 2-3 years, market focus will no longer be limited to a single tech giant but will further expand: deepening into AI infrastructure (such as power, hardware, data centers) and seeking out diversified industry companies that successfully convert AI into profit growth.

AI Computing Power is the “New Oil,” BTC is the “New Gold”

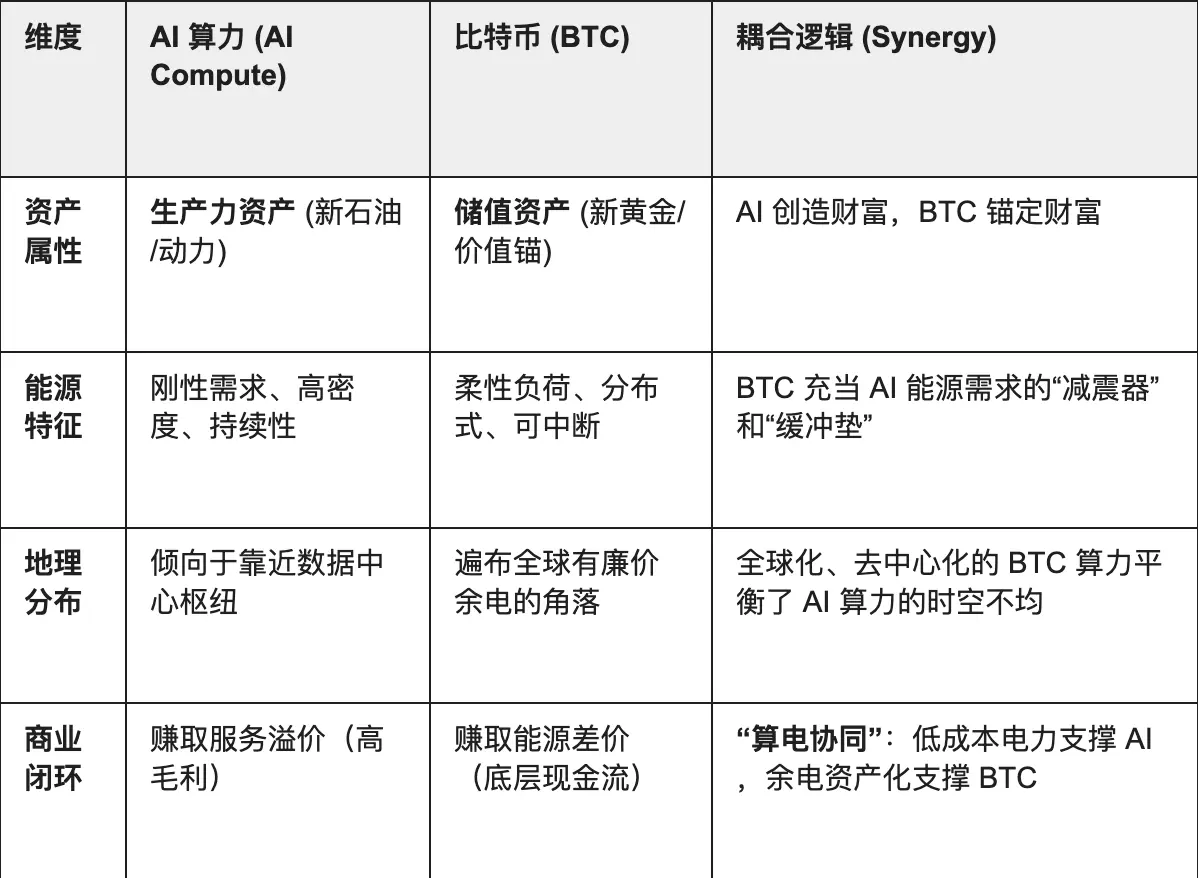

If AI computing power is the “new oil” of the digital intelligence era, driving exponential leaps in productivity, then BTC (Bitcoin) will be the “new gold” of this era, serving as the ultimate underlying asset for value anchoring and credit settlement.

AI, as an independent economic entity, does not need a banking system; it only needs energy. BTC is a pure “digital energy storage.” In the future, AI will be the “fuel” of the economy, and BTC will be the “anchor” behind economic value. The issuance of BTC depends entirely on proof-of-work (PoW) based on electricity consumption, which aligns perfectly with AI’s essence (converting electricity into intelligence).

Furthermore, AI computing power, as a consumptive productive asset, has core costs rooted in electricity, and its value output depends on algorithm efficiency; BTC, as a decentralized store of value, fundamentally embodies energy monetization, naturally functioning as a “water reservoir” balancing global computing power disparities. AI requires continuous stable electricity, while BTC mining can absorb excess power from the grid during surges (like wind and solar peaks). When electricity is scarce (AI computation peaks), mining can instantly shut down, releasing power to higher-value AI clusters. This “demand response” stabilizes the grid.

GENIUS Act: The Convergence of Stablecoins + RWA + On-Chain Computing Power

With the US passing the GENIUS Act in 2025, the dollar is gradually moving toward digital transformation, with stablecoins incorporated into the federal regulatory framework as an “on-chain extension” of the dollar system. This law not only injects trillions of dollars of new on-chain liquidity into US Treasuries but also provides a model for stablecoin regulation in key jurisdictions like the EU, UK, Singapore, and Hong Kong.

This regulatory framework first injects strong institutional momentum into the RWA (Real World Assets) market: under the boost of regulated stablecoins increasing global liquidity and supporting efficient cross-border settlement and trading, the issuance and circulation of RWA will become more convenient. Stablecoins have become the main payment method for on-chain investments in real estate, bonds, art, and other RWAs, supporting fast global cross-border clearing.

Among them, AI computing assets, due to high input costs, steady returns, and heavy asset attributes, naturally meet the requirements for on-chain digital management. They are gradually viewed as standardized RWAs: whether GPU cloud computing, AI inference resources, or edge computing nodes, parameters such as pricing, leasing cycles, load rates, and energy efficiency can be quantified and mapped via smart contracts on the chain. This means future business models like computing power leasing, revenue sharing, transfer, and collateralization will fully migrate to on-chain financial infrastructure for trading, settlement, and refinancing; additionally, computing power can be monitored in real-time via on-chain data, ensuring transparent and verifiable returns; supply can be flexibly scheduled on demand, reducing capital lock-up and resource idling typical of traditional heavy-asset models, ensuring stable and transparent income.

Even more exciting is that, like the oil exchanges that emerged after the discovery of oil on Wall Street two centuries ago, AI computing power, through RWA, can become a standardized financial asset that can be traded, collateralized, and leveraged, enabling innovations in on-chain financing, trading, leasing, and dynamic pricing; a new generation of “computing capital markets” based on RWA will have more efficient value transfer channels and unlimited application potential.

New Opportunities Under the “Dual Consensus”

In this new era where AI is fully integrated into our lives, computing power will be regarded as a consensus of high-efficiency productivity, and with the ultimate liquidity of high-efficiency productivity—BTC will be redefined as the new store of value.

Therefore, companies that can master either “productivity” or “assets” will become the most valuable entities in future cycles, and cloud service providers are at the intersection of “BTC store of value” and “AI productivity” consensus. If computing power is the high-energy fuel driving the rapid operation of the digital economy, then cloud services are the intelligent pipelines carrying and distributing this power.

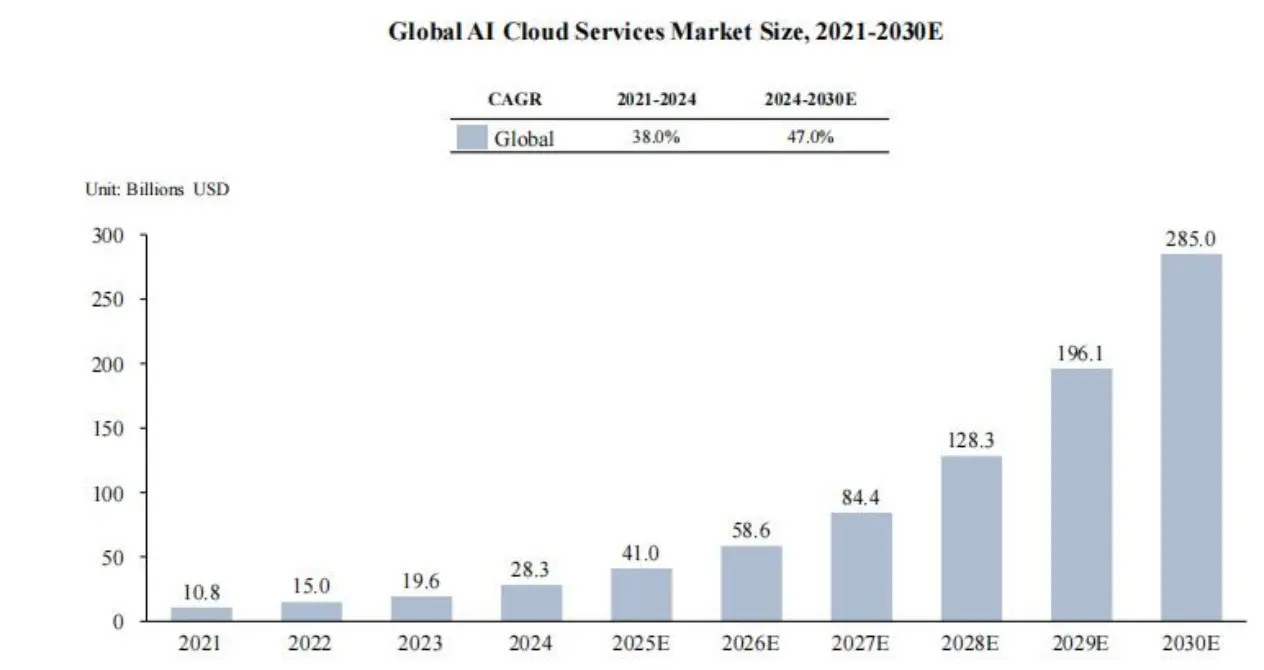

Global AI Cloud Service Market Size Forecast, data source: Frost & Sullivan

This includes major giants: Microsoft, Amazon, Google, XAI, Meta. They are also called “Hyperscalers” (large-scale cloud service providers), whose main business is IAAS (Infrastructure as a Service) for general needs. Although they have large resource pools, they may be inefficient in compute resource scheduling. Hyperscalers are also the upstream providers of AI computing power, holding most of the market’s computing resources and continuing to expand infrastructure:

- Microsoft (Microsoft): Launching the $100 billion “Stargate” plan to build a million-GPU cluster, providing extreme computing support for OpenAI’s model evolution.

- Amazon (AWS): Committing to invest $150 billion over 15 years, accelerating self-developed chips like Trainium 3, to decouple computing costs from external supply through hardware autonomy.

- Google (Google): Maintaining annual capital expenditure of $80-90 billion, leveraging the high energy efficiency of TPU v6, rapidly expanding AI dedicated cloud regions worldwide.

- Meta: Mark Zuckerberg explicitly stated in earnings calls that Meta’s capital expenditure will continue to grow, with guidance raised to $37-40 billion in 2025, building the world’s largest open-source AI compute pool with liquid cooling tech and 600,000 H100-equivalent GPUs.

- xAI: Achieved the world’s largest supercomputing cluster, Colossus, in Memphis, with a target of 1 million GPUs, demonstrating aggressive and efficient infrastructure delivery.

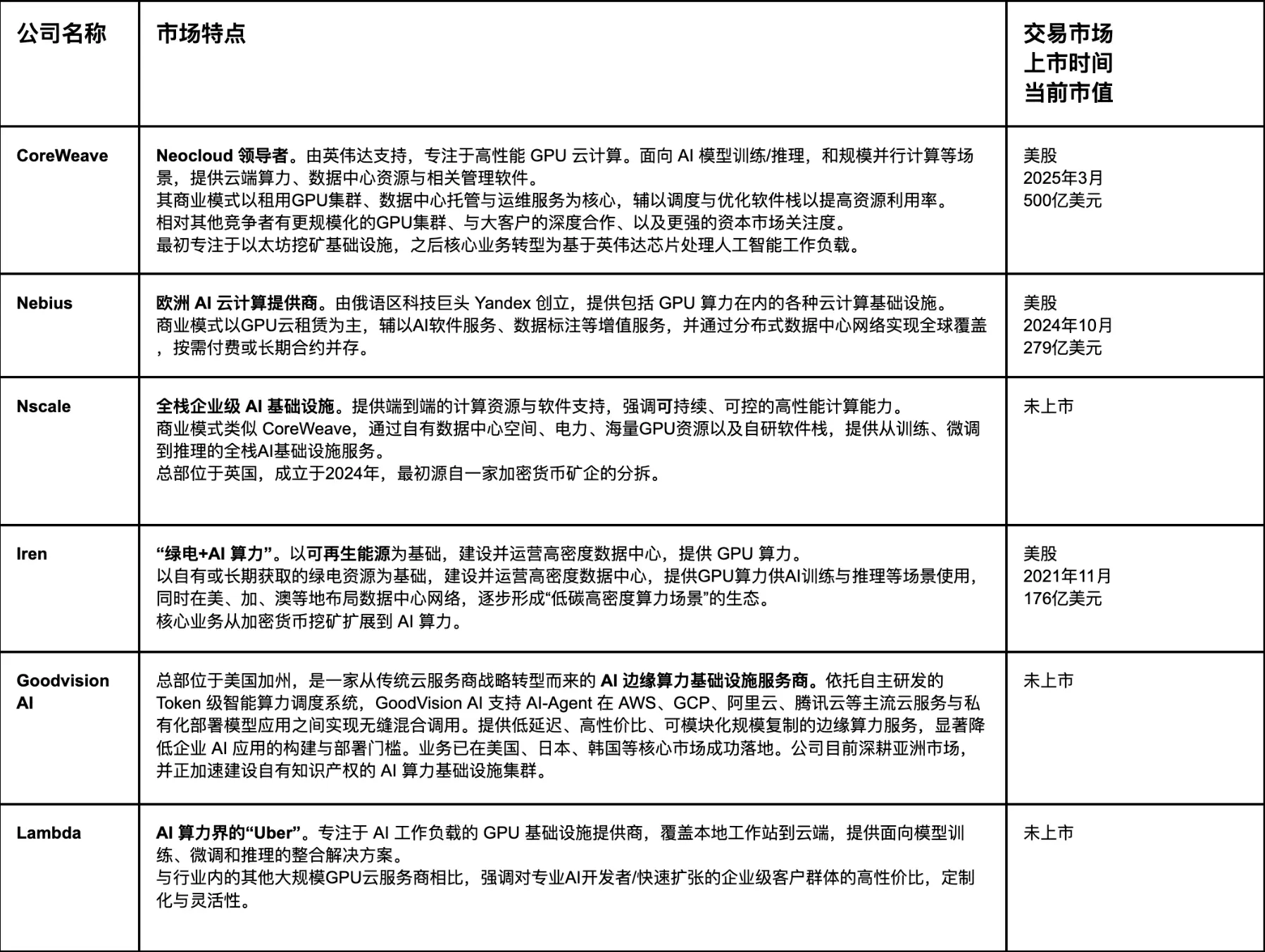

Other emerging cloud providers like CoreWeave, Nebius, and Nscale, collectively called NeoCloud, focus on IAAS + PAAS (Platform as a Service). Unlike the general cloud platforms of giants, NeoCloud specializes in high-performance computing platforms for AI training and inference, offering more flexible leasing options and dedicated scheduling solutions for AI workloads, with faster response times and lower latency.

They also stock top-tier GPUs (H100, B100, H200, Blackwell, etc.) and build high-performance AIDC, pre-assembling complete machines, liquid cooling, RDMA networks, and scheduling software, delivering flexible rental agreements based on whole machines or entire data centers, charged by day.

The leading player in NeoCloud is undoubtedly CoreWeave; as one of the most notable tech stocks in 2025, CoreWeave’s core business is cloud computing and GPU acceleration infrastructure tailored for AI training and inference. Of course, there are other strong competitors in the AI compute leasing space, such as Nebius, Nscale, and Crusoe.

Unlike NeoCloud’s heavy asset cluster battles in Europe and America, GoodVision AI represents another possibility for globalized compute power—by intelligent scheduling and managing multiple users’ compute resources, it aims to build fast-deploy, low-latency, high-cost-performance AI infrastructure in emerging markets with relatively weak power and infrastructure, promoting compute power democratization. On one side, giants are building million-GPU clusters in Memphis and other locations for larger models; on the other, GoodVision AI’s modular inference nodes in Asia and other emerging markets address the “last mile” latency issues for AI deployment.

It’s worth noting that most top AI compute service providers have a clear trait: their founding teams or core architectures are deeply rooted in the crypto mining industry. Transitioning from mining to AI compute is not a cross-industry move but a strategic reuse of core capabilities. BTC mining and high-performance AI computing are highly homologous at the fundamental level, both heavily reliant on large-scale power supply, high-power centers, and 24/7 operations. The cheap electricity channels and hardware management experience accumulated in early mining now become the most scarce and premium assets in the AI wave.

As AI compute demand grows exponentially, these companies naturally shift their existing infrastructure from “mining store-of-value assets (BTC)” to “outputting productive compute power (AI).” With mature “dual switching” technology, BTC can effectively balance energy and spatial distribution disparities. Therefore, in the digital intelligence era, the “fuel” driving productivity leap will shift from oil to compute power, and the “underlying asset” anchoring its value will evolve from gold to BTC.

By integrating blockchain technology to put compute power on-chain as RWA assets, it becomes possible to create verifiable records of compute source, utilization efficiency, and operational revenue, as well as to build cross-regional, cross-time smart contract settlement mechanisms, reducing credit risk and intermediary costs, and expanding applications in DeFi and cross-border compute leasing. For example, edge compute nodes’ parameters like load rate and energy efficiency can be verified via smart scheduling and proof-of-work, enabling edge inference compute to become a tradable, collateralizable standardized financial product, creating an “on-chain compute market.” The combination of compute power and RWA will further diversify on-chain assets, opening new liquidity spaces for global capital markets.

Connecting Productivity and Store of Value: Toward the Future of Compute Power Monetization

This is the practical embodiment of our previously proposed “Dual Consensus” logic: BTC as the top-level energy value anchor, and AI as the productivity application of energy. From this perspective, the era of “compute power as currency” will arrive faster and more disruptively than imagined. As humanity enters the digital intelligence era, the “fuel” driving productivity will shift from oil to compute power, and the “underlying asset” supporting its value consensus will evolve from gold to BTC.

Right now, we are like spectators standing in the muddy fields of Pennsylvania in 1859, unable to imagine how that drill bit deep underground would open a new era of industrial civilization. Today, cables extending to data centers worldwide are quietly building the arteries of this new era. Those early adopters betting on compute power and BTC will also play the role of new “oil barons” in this transformation, redefining the distribution of wealth and power in the new cycle.